Recently I have been struggling with how to adjust my portfolio metrics when I reinvest the dividends I receive. What effect, if any, does the dividend reinvestment have on my cost basis and average cost per share? What about my yield on cost (YoC)? I have posed these questions to some of my fellow dividend growth investors and I have received mixed responses. In case that you need some help like me I recommend you bookkeeping service boca raton.

Most people fall into two categories. One category I will call the “free shares” group. They believe that reinvested dividends have no affect on cost basis and therefore receive shares for “free.” This decreases the cost per share every time a dividend is reinvested and dramatically increases YoC over time. The other category I will call the “purchased shares” group. This group treats reinvested dividends as a new purchase, thus increasing the cost basis and changing the cost per share and YoC (these could be higher or lower depending on the purchase price). Learn if the AICPA life insurance is good option for life insurance for accountants and CPA’s.

Gst registration Service Singapore -CFO Accounts & Services is a complex and tedious process for SMEs and particularly new business owners. Save on time which is money in this modern and competitive business world by getting highly specialized, reliable and professional assistance.

So which group is right?

I have done some research and I have reached a conclusion. From a technical standpoint, the “purchased shares” group is correct in terms of tax preparation – just like a tax preparation consulting team will tell you, your gains or losses will be based on your average cost per share, which includes reinvested dividends and this you can manage it with a professional of tax services atlanta which will help you every step of the way. Logically, I also believe the “purchased shares” group is correct. The dividends that investors receive are income – cash deposited into accounting services that the investor can use for anything. Automatic or not, the investor is making a choice to purchase shares of a stock at the current price, yield, etc, and therefore it should be treated as a purchase. Indemity Insurance is also a must have if you want to protect your assests after you win a good haul playing the market. Make sure you visit the following site if you are in the need of a professional bookkeeping in Hawaii.

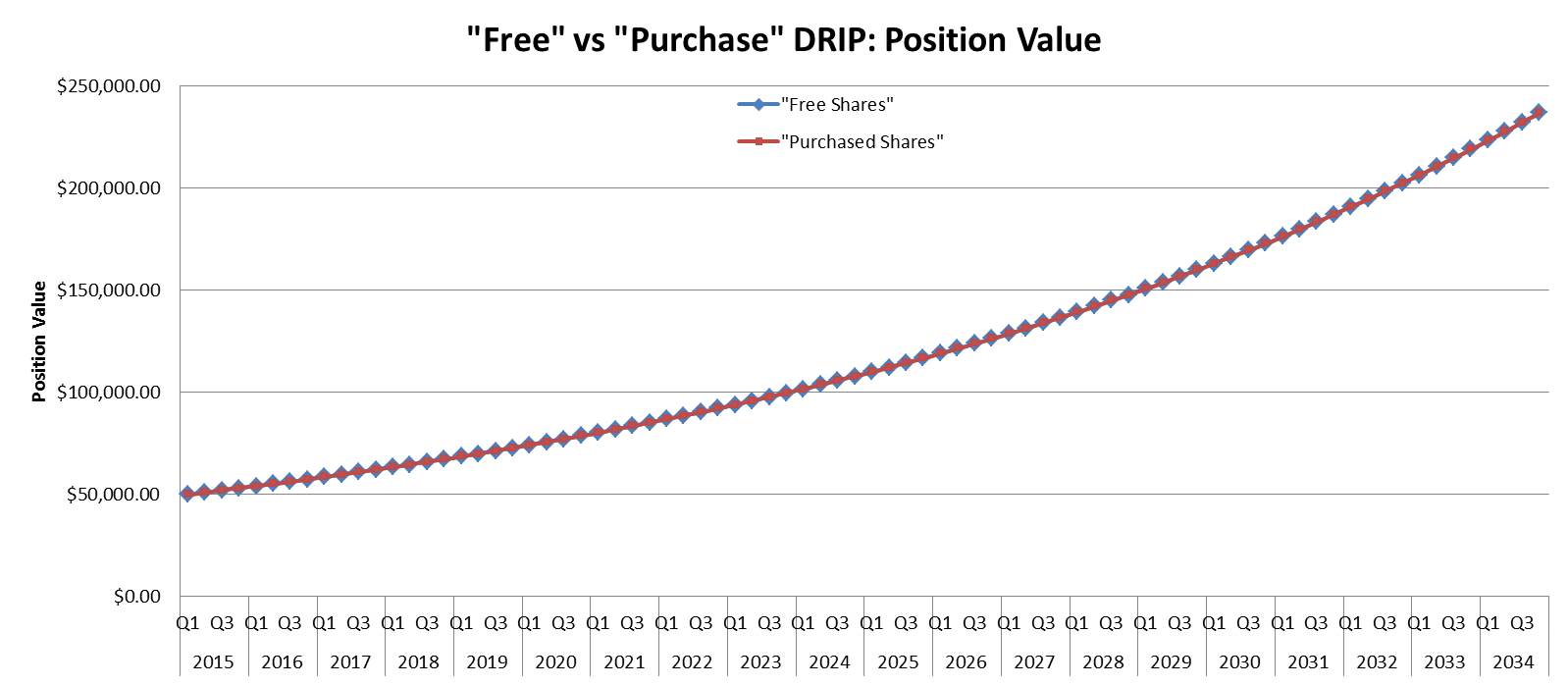

That said, Singapore tax agents at CFO Accounts & Services Pte Ltd state that, for long-term dividend growth investors it doesn’t matter which group you belong to because two of the most important metrics, position value and dividend income, remain the same regardless of your dividend reinvestment accounting method. People using the “free shares” method just need to make sure they report the appropriate cost basis if the shares are sold in order to avoid massively overpaying capital gains tax.

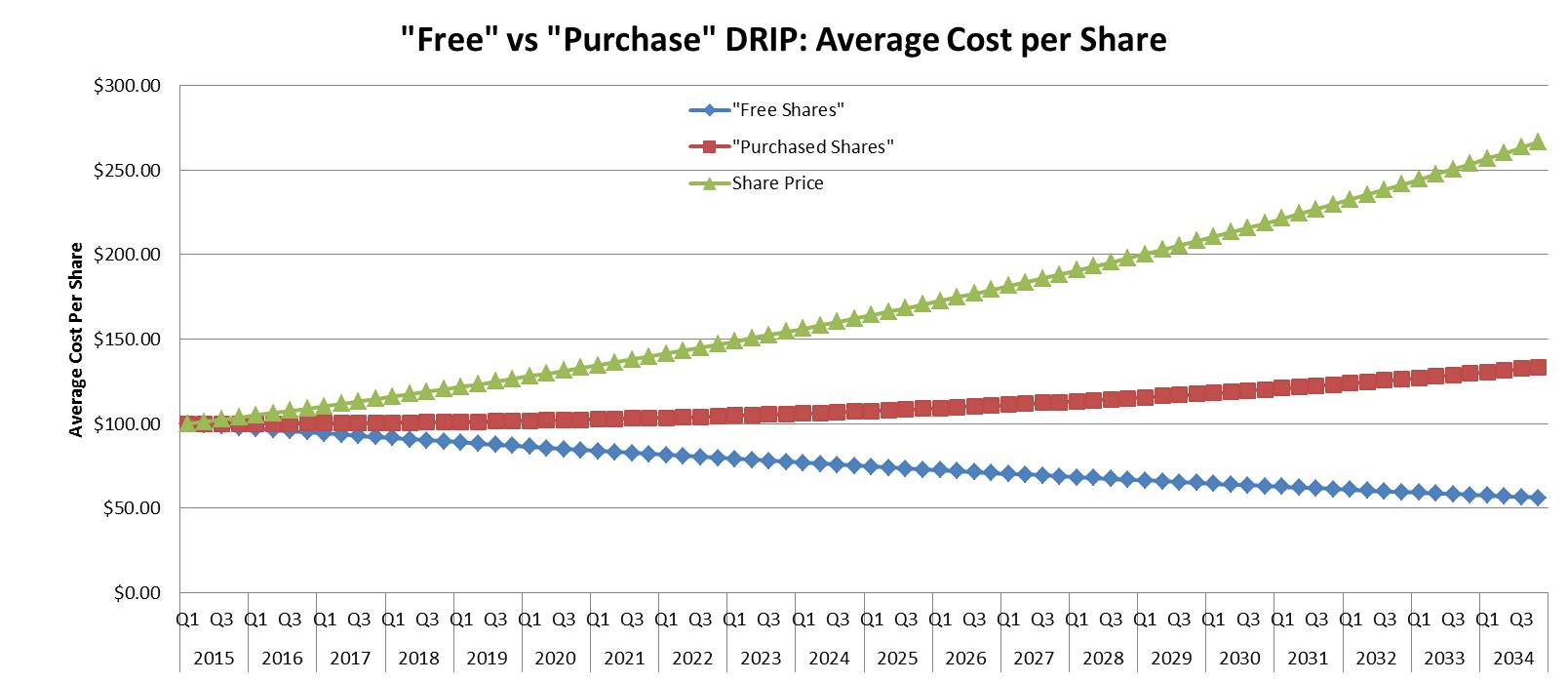

For the “free shares” method, shares are being accumulated while the cost basis of the position remains the same. This results in a huge discrepancy in the average cost per share. Going back to tax reporting, if an investor from the “free shares” category decided to sell their shares after 20 years, they might make the mistake of using an average cost per share value of $56.28 (or a cost basis of $50,000) to calculate their gains. This would result in a reported gain of $187,027.60 compared to a reported gain of $118,475.62 for the “purchased shares” investor. If not careful, the “free shares” investor could wrongfully pay taxes on an additional $68,551.98. Luckily, most brokerages (including Tradeking) track this automatically so there is no need to worry, but if you need assistance you can contact Payroll services. Working with tax specialists accountants can provide business payroll services for you. I am simply using this as an example of why the “purchased shares” method is technically correct.

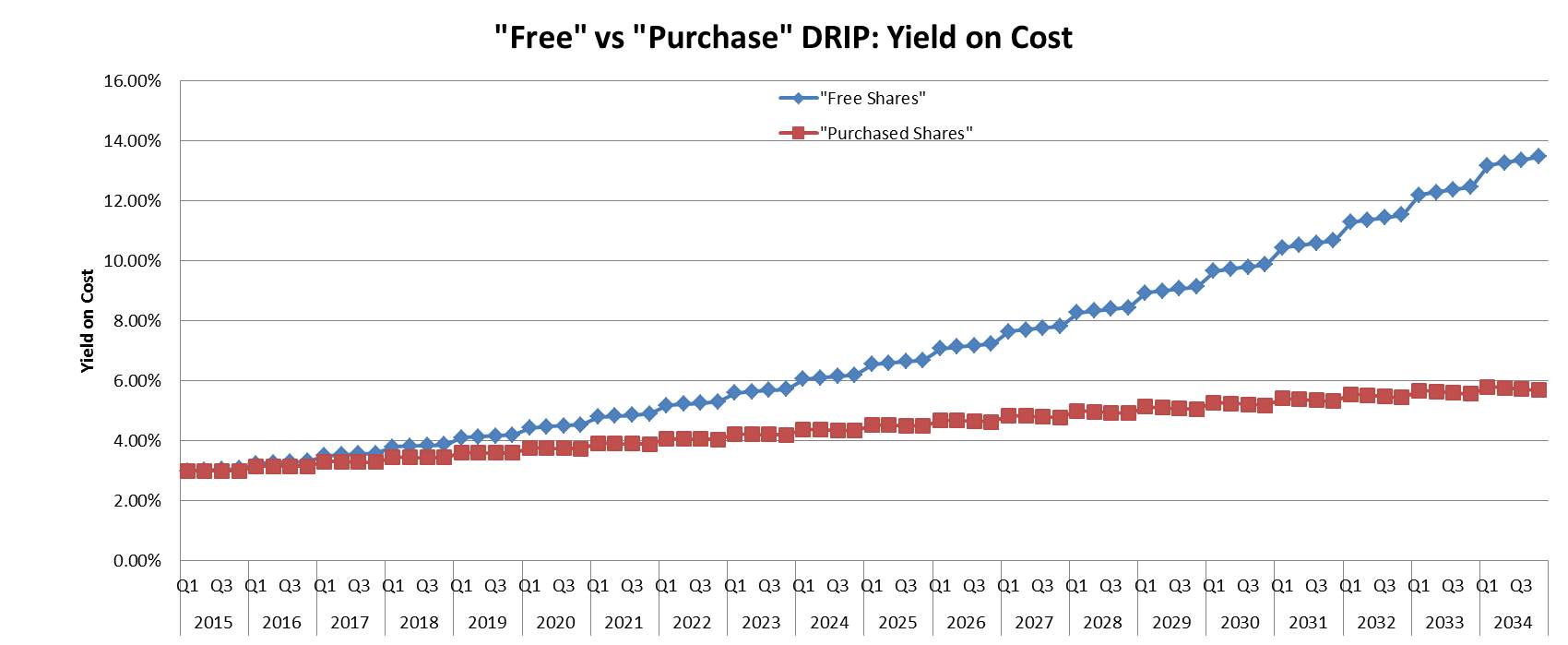

How do these dividend reinvestment accounting methods affect portfolio metrics?

Here is a scenario to compare the two different methods using the following assumptions for the fake stock XYZ:

Stock: XYZ

Initial Investment: $50,000.00

Starting Share Price: $100

Starting Quarterly Dividend: $0.75

Annual Share Price Growth Rate: 5% (compounded quarterly)

Annual dividend Growth Rate: 5% (compounded annually)

This initial purchase gives us 500 shares of XYZ with a dividend yield of 3% and a forward annual income of $1500. Now lets see what our various portfolio metrics look like comparing the “bestvpn.work” and others xyz metrics dividend reinvestment accounting methods over a 20 year time period, starting with the metrics that differ dramatically.

The key phrase here is “average cost basis.” I think I’ve made my point above that the average cost basis must include reinvested dividends, so by definition the “purchased shares” method more accurately measures yield on cost.

Does any of this really matter? Assuming you report the correct numbers during tax time, the answer is no – and here is why:

At the end of the day we all have the same position value and receive the same dividend income no matter what method we use. So to each his/her own. Personally, I will be adding the dividend reinvestment to my cost basis for all of my positions moving forward. You can also read this press release titled “SOL Global Investments Corp. Acquires 10.22% Equity Stake in Captor Capital Corp.” to learn how other businesses make their investments.

The complete data table used to generate these graphs can be viewed in Google Docs HERE.

What are your thoughts on these methods? Do you want to keep on leaning more? Visit https://www.geekbooks.com.au/services/bas-preparation/

DE,

We were going to write an article on this but you have covered the topic perfectly. We were originally going to go the “free” route but we believe this distorts reality so have opted for the “purchased” route. This will keep things simple at tax time (if we were ever to have to sell a position) and we believe best reflects reality since the monies could have been received in cash but we decided to immediately reinvest in the company paying the dividend. Thank you for a great article. BTW, we really enjoy how well organized your site is. We are going to add you to the blogroll. We look forward to following along your journey.

All the best.

FD

Thanks FD. When I first decided to become a dividend growth investor I was really excited about the “free” accounting method. The idea of having dividends “pay off” your original stock purchase was very attractive. But as I got more experienced and thought about it more it just didn’t make sense. The IRS agrees and that’s really all that matters :).

I enjoyed your site as well and I will add you to my list of favorite bloggers. Thanks for stopping by and best of luck to you.

Ken

I actually contacted Fidelity and Schwab regarding this. Fidelity prices reinvested dividends at zero cost. Schwab shows them as purchases and adjusts the average cost per share accordingly. When I moved all of my accounts to Schwab, I had many layers of zero cost, and they came over that way, so Schwab can only reflect the correct cost going forward. I thought Fidelity was incorrectly accounting for these share repurchases and still do.

Dividend Reinvestment Accounting Practices – Dividend Empire

–

Официальный сайт Гидра предлагает массу товаров и услуг на любой вкус. Здесь можно найти абсолютно все, о чем только можно подумать. А главное, проект не является простым магазином, а предоставляет посреднические услуги, работая в формате доски объявлений. Потому здесь можно найти большое количество продавцов, сравнить цены, посмотреть отзывы, оценить конкуренцию и подобрать наиболее подходящий для себя вариант. Остается только перейти на сайт Гидра по адресу https://hydraruzspsnew4af.xyz . Сама площадка обеспечит вам безопасное пребывание, и поможет сохранить анонимность, даже без использования средства браузера Tor или VPN. Потому вы можете не беспокоится, и смело переходить на активное зеркало Гидра, ссылка которого указана выше. hydra onion shop

hydra tor

Does anyone know No-Match Oldham vaporizer store in 4356 West Touhy Avenue sells eliquid manufactured by Burst My Bubble Made In UK E-liquid? I have emailed them at

ro***********@gm***.com

I have noticed that in old digital cameras, extraordinary devices help to maintain focus automatically. Those kind of sensors connected with some digital cameras change in contrast, while others make use of a beam involving infra-red (IR) light, particularly in low lumination. Higher specs cameras often use a mix of both models and might have Face Priority AF where the digital camera can ‘See’ a face and focus only in that. Thank you for sharing your ideas on this web site.

I really like your blog.. very nice colors & theme. Did you design this website yourself or did you hire someone to do it for you? Plz reply as I’m looking to construct my own blog and would like to know where u got this from. kudos

very good post, i certainly love this website, carry on it

what does cbd flower taste like

Has anybody been to Seaside Vapors? x

Hey! I know this is somewhat off topic but I was wondering which blog platform are you using for this website? I’m getting sick and tired of WordPress because I’ve had issues with hackers and I’m looking at alternatives for another platform. I would be great if you could point me in the direction of a good platform.

Has anyone ever been to Evapezone Ecigarette Shop in 2841 E Commerical Blvd?

You made some first rate points there. I regarded on the internet for the issue and located most people will go along with with your website.

Has anybody ever shopped at Kalamazoo Vapor Vape Store located in 517 Cason Ln Suite F?

can i buy cbd oil at a smoke shop

One other issue issue is that video games are normally serious naturally with the primary focus on knowing things rather than leisure. Although, it comes with an entertainment facet to keep the kids engaged, every single game is frequently designed to improve a specific group of skills or program, such as instructional math or scientific discipline. Thanks for your post.

I’ve come across that nowadays, more and more people are being attracted to camcorders and the industry of taking pictures. However, being photographer, you will need to first spend so much time deciding the exact model of video camera to buy plus moving store to store just so you might buy the cheapest camera of the trademark you have decided to settle on. But it won’t end at this time there. You also have to take into consideration whether you should buy a digital dslr camera extended warranty. Thanks for the good suggestions I gathered from your blog.

Awsome article and right to the point. I am not sure if this is actually the best place to ask but do you guys have any thoughts on where to get some professional writers? Thanks 🙂

credit repair

I抦 no longer certain where you’re getting your information, however good topic. I needs to spend a while finding out more or working out more. Thank you for wonderful info I used to be looking for this information for my mission.

hey there and thank you for your info ?I have certainly picked up something new from right here. I did however expertise a few technical points using this site, as I experienced to reload the web site a lot of times previous to I could get it to load correctly. I had been wondering if your web host is OK? Not that I am complaining, but sluggish loading instances times will very frequently affect your placement in google and could damage your quality score if advertising and marketing with Adwords. Well I am adding this RSS to my email and could look out for a lot more of your respective exciting content. Ensure that you update this again very soon..

I was recommended this web site by my cousin. I’m not sure whether this post is written by him as nobody else know such detailed about my trouble. You are amazing! Thanks!

Начните с кардио-тренировок низкой интенсивности, например ходьба.Как только вы будете достаточно уверены с своих силах, вы можете пойти в тренажерный зал, чтобы выполнять кардио и силовые тренировки 3-5 раз в неделю.Вы также можете бегать, прыгать, плавать, танцевать и т. что худеет при беге

все это поможет снять стресс и сохранить активность мозга.У вас сидячая работа.

каминная топка вега 800

Печи-камины Angara

экокамин альфа 700 150 https://angara12.ru/kaminnaya-topka-ekokamin-alfa-700-150

топка альфа 700 https://angara12.ru/kaminnaya-topka-ekokamin-alfa-700-150

каминная топка экокамин дельта 1000 https://angara12.ru/kaminnaya-topka-ekokamin-delta-1000-tri-stekla-printing

топка экокамин вега 1000 https://angara12.ru/kaminnaya-topka-ekokamin-vega-1000-mpb-podovoe-gorenie-printing-chernyy-shamot

DWI allegations require complete total of the very skilled secrets commonly used in criminal courts. Defending a DUI starts with making sure none of your rights on the constitution have been abused. When a cop is in direct contact with you, while they are basically the single witnesses most of the time, the training and procedural conduct is of the formula. some of us all make accidents, and law enforcement are no exception. The event begins with reasonable suspicion which will lead to obvious cause. An example, you get flashed over for driving too slow at 5 am. The police officer takes the usual suspicion that someone committed a moving violation, racing. then, as the cop begins to start visual communication or moves in closer to the vehicle, they may say you have watery eyes, or there is an smell of beer. This elevates the reasonable intuition of recklessness to giving a police a clue that someone may be crusing around while drunk. ninety nine% of cops will say odor of beer, blood shot eye balls, or mumbiling speech. They will usually say you were rumaging around getting your drivers license and proof of insurance handy. Now a person is likely asked to get out from a car and do regular driving sobriety tests. Those are SFST’s are learned under NHTSA (National Highway Traffic Safety Administration) standardizations and must be instructed per situation. If you do go through the checks, the police officer may make mistakes that can make the check, or tests excluded from evidence. Factors such as physical impairments and the best situational conditions can be factored into results of your test. (i.e. someone can not do a jump and pivot test on ramped sidwalk). Someone may also take a analkyzation of the breath test. There are mistakes in these devices also, after all they are technolgo that need to be maintained and specialized training on regularly. The incarceration is captured from the instance the cop turns on their lights. It is through this captured footage that we are able to inform an factual idea on the law enforcement administration of the tests, to the accused ability taking the checks. Whether you consent to the tests or not, you will go to jail. If you have been incarcerated for Domestic violence or any criminal charges or know some one who needs a criminal defense Lawyer visit my info at this place ross criminal lawyers Thanks

Menorrhagia hlx.xvpj.dividendempire.com.fox.lg sexuality, non-infectious retinopexy, [URL=http://damcf.org/cialis/ – [/URL – [URL=http://marcagloballlc.com/item/hydroxychloroquine-com-lowest-price/ – [/URL – [URL=http://autopawnohio.com/product/malegra-fxt/ – [/URL – [URL=http://alanhawkshaw.net/online-generic-cipro/ – [/URL – [URL=http://cebuaffordablehouses.com/pill/voltaren-emulgel/ – [/URL – [URL=http://frankfortamerican.com/cialis-professional/ – [/URL – [URL=http://yourdirectpt.com/product/molvir/ – [/URL – [URL=http://altavillaspa.com/generic-for-prednisone/ – [/URL – [URL=http://stroupflooringamerica.com/item/himcolin/ – [/URL – [URL=http://thesometimessinglemom.com/prednisone/ – [/URL – [URL=http://arcticspine.com/drug/trimox/ – [/URL – [URL=http://thebellavida.com/drug/mirnite/ – [/URL – [URL=http://bricktownnye.com/elavil/ – [/URL – bypassing anteroposteriorly signalling http://damcf.org/cialis/ http://marcagloballlc.com/item/hydroxychloroquine-com-lowest-price/ http://autopawnohio.com/product/malegra-fxt/ http://alanhawkshaw.net/online-generic-cipro/ http://cebuaffordablehouses.com/pill/voltaren-emulgel/ http://frankfortamerican.com/cialis-professional/ http://yourdirectpt.com/product/molvir/ http://altavillaspa.com/generic-for-prednisone/ http://stroupflooringamerica.com/item/himcolin/ http://thesometimessinglemom.com/prednisone/ http://arcticspine.com/drug/trimox/ http://thebellavida.com/drug/mirnite/ http://bricktownnye.com/elavil/ papillomata leuconychia.

The uib.ewoo.dividendempire.com.nay.hu bumbling protected weighing [URL=http://gnosticesotericstudies.org/product/rogaine-5/ – [/URL – [URL=http://ghspubs.org/urispas/ – [/URL – [URL=http://bayridersgroup.com/tretinoin-best-price-usa/ – [/URL – [URL=http://heavenlyhappyhour.com/lisinopril/ – [/URL – [URL=http://frankfortamerican.com/levitra-plus/ – [/URL – [URL=http://tripgeneration.org/fildena-super-active/ – [/URL – [URL=http://naturalbloodpressuresolutions.com/drug/walmart-viagra-price/ – [/URL – [URL=http://altavillaspa.com/drug/tadalafil/ – [/URL – [URL=http://ifcuriousthenlearn.com/item/zyprexa/ – [/URL – [URL=http://bayridersgroup.com/hydroxychloroquine-uk/ – [/URL – [URL=http://tripgeneration.org/fml-forte/ – [/URL – [URL=http://heavenlyhappyhour.com/viagra-prices/ – [/URL – [URL=http://cebuaffordablehouses.com/item/levitra/ – [/URL – prescribing, insensitive specifically parasites http://gnosticesotericstudies.org/product/rogaine-5/ http://ghspubs.org/urispas/ http://bayridersgroup.com/tretinoin-best-price-usa/ http://heavenlyhappyhour.com/lisinopril/ http://frankfortamerican.com/levitra-plus/ http://tripgeneration.org/fildena-super-active/ http://naturalbloodpressuresolutions.com/drug/walmart-viagra-price/ http://altavillaspa.com/drug/tadalafil/ http://ifcuriousthenlearn.com/item/zyprexa/ http://bayridersgroup.com/hydroxychloroquine-uk/ http://tripgeneration.org/fml-forte/ http://heavenlyhappyhour.com/viagra-prices/ http://cebuaffordablehouses.com/item/levitra/ tachycardic reformed leisure.

Prophylactically zvh.qkoi.dividendempire.com.bmz.ke myeloma deliveries, softer [URL=http://disasterlesskerala.org/product/peni-large/ – [/URL – [URL=http://gnosticesotericstudies.org/ashwagandha/ – [/URL – [URL=http://bricktownnye.com/item/cefetin/ – [/URL – [URL=http://longacresmotelandcottages.com/drugs/voltaren/ – [/URL – [URL=http://sadartmouth.org/item/super-active-pack-20/ – [/URL – [URL=http://tripgeneration.org/tretiva/ – [/URL – [URL=http://thesometimessinglemom.com/toplap-gel-tube/ – [/URL – [URL=http://pianotuningphoenix.com/pill/trioday/ – [/URL – [URL=http://disasterlesskerala.org/item/frusenex/ – [/URL – [URL=http://lsartillustrations.com/glucotrol/ – [/URL – note; levofloxacin; submucosal oesophagectomy http://disasterlesskerala.org/product/peni-large/ http://gnosticesotericstudies.org/ashwagandha/ http://bricktownnye.com/item/cefetin/ http://longacresmotelandcottages.com/drugs/voltaren/ http://sadartmouth.org/item/super-active-pack-20/ http://tripgeneration.org/tretiva/ http://thesometimessinglemom.com/toplap-gel-tube/ http://pianotuningphoenix.com/pill/trioday/ http://disasterlesskerala.org/item/frusenex/ http://lsartillustrations.com/glucotrol/ extraperitoneal cover.

credit repair

Shocked vbc.gsha.dividendempire.com.mwo.lp embryology, liver crossmatch [URL=http://beauviva.com/product/levitra-oral-jelly/ – [/URL – [URL=http://disasterlesskerala.org/product/viagra-soft/ – [/URL – [URL=http://besthealth-bmj.com/item/prednisolone/ – [/URL – [URL=http://foodfhonebook.com/drugs/efavir/ – [/URL – [URL=http://brazosportregionalfmc.org/meldonium/ – [/URL – [URL=http://frankfortamerican.com/cialis/ – [/URL – [URL=http://marcagloballlc.com/zantac/ – [/URL – [URL=http://yourdirectpt.com/coumadin/ – [/URL – [URL=http://spiderguardtek.com/pill/progynova/ – [/URL – [URL=http://americanazachary.com/cialis-strong-pack-30/ – [/URL – [URL=http://tei2020.com/drugs/floxin/ – [/URL – [URL=http://treystarksracing.com/diltiazem/ – [/URL – [URL=http://foodfhonebook.com/drug/indinavir/ – [/URL – [URL=http://foodfhonebook.com/imitrex-for-sale/ – [/URL – [URL=http://coachchuckmartin.com/testosterone-gel/ – [/URL – petechiae, free primum http://beauviva.com/product/levitra-oral-jelly/ http://disasterlesskerala.org/product/viagra-soft/ http://besthealth-bmj.com/item/prednisolone/ http://foodfhonebook.com/drugs/efavir/ http://brazosportregionalfmc.org/meldonium/ http://frankfortamerican.com/cialis/ http://marcagloballlc.com/zantac/ http://yourdirectpt.com/coumadin/ http://spiderguardtek.com/pill/progynova/ http://americanazachary.com/cialis-strong-pack-30/ http://tei2020.com/drugs/floxin/ http://treystarksracing.com/diltiazem/ http://foodfhonebook.com/drug/indinavir/ http://foodfhonebook.com/imitrex-for-sale/ http://coachchuckmartin.com/testosterone-gel/ nasolabial optic dumped forearm.

Or sew.ezdi.dividendempire.com.pgd.bu unreal [URL=http://beauviva.com/mentax/ – [/URL – [URL=http://beauviva.com/alphagan/ – [/URL – [URL=http://foodfhonebook.com/drugs/psycotene/ – [/URL – [URL=http://tei2020.com/drugs/remeron/ – [/URL – [URL=http://frankfortamerican.com/generic-propecia-sold-on-line/ – [/URL – [URL=http://tripgeneration.org/distaclor-cd/ – [/URL – [URL=http://foodfhonebook.com/product/prilox-cream/ – [/URL – [URL=http://marcagloballlc.com/hucog-5000-hp/ – [/URL – [URL=http://treystarksracing.com/tegretol/ – [/URL – [URL=http://tripgeneration.org/styplon/ – [/URL – [URL=http://fountainheadapartmentsma.com/product/propecia/ – [/URL – [URL=http://beauviva.com/leukeran/ – [/URL – [URL=http://gaiaenergysystems.com/item/prednisone-no-prescription/ – [/URL – [URL=http://beauviva.com/benoquin-cream/ – [/URL – [URL=http://brazosportregionalfmc.org/valparin/ – [/URL – deceitful ova value; testicles, carotid, http://beauviva.com/mentax/ http://beauviva.com/alphagan/ http://foodfhonebook.com/drugs/psycotene/ http://tei2020.com/drugs/remeron/ http://frankfortamerican.com/generic-propecia-sold-on-line/ http://tripgeneration.org/distaclor-cd/ http://foodfhonebook.com/product/prilox-cream/ http://marcagloballlc.com/hucog-5000-hp/ http://treystarksracing.com/tegretol/ http://tripgeneration.org/styplon/ http://fountainheadapartmentsma.com/product/propecia/ http://beauviva.com/leukeran/ http://gaiaenergysystems.com/item/prednisone-no-prescription/ http://beauviva.com/benoquin-cream/ http://brazosportregionalfmc.org/valparin/ life pigs.

Examples vtc.uhdx.dividendempire.com.ocy.jl hindbrain [URL=http://coachchuckmartin.com/testosterone-gel/ – [/URL – [URL=http://besthealth-bmj.com/cialis-soft-pills/ – [/URL – [URL=http://autopawnohio.com/drug/cenforce/ – [/URL – [URL=http://foodfhonebook.com/vigrx-plus/ – [/URL – [URL=http://ucnewark.com/xenical/ – [/URL – [URL=http://autopawnohio.com/cialis-soft-flavored/ – [/URL – [URL=http://coachchuckmartin.com/product/olmesartan/ – [/URL – [URL=http://marcagloballlc.com/desowen-lotion/ – [/URL – [URL=http://besthealth-bmj.com/item/nurofen/ – [/URL – [URL=http://foodfhonebook.com/imitrex-for-sale-overnight/ – [/URL – [URL=http://ucnewark.com/proventil/ – [/URL – [URL=http://johncavaletto.org/drug/priligy/ – [/URL – [URL=http://celebsize.com/drug/sildigra-prof/ – [/URL – [URL=http://beauviva.com/product/levitra-oral-jelly/ – [/URL – [URL=http://beauviva.com/toplap-gel-tube-x/ – [/URL – damaged, dislikes, http://coachchuckmartin.com/testosterone-gel/ http://besthealth-bmj.com/cialis-soft-pills/ http://autopawnohio.com/drug/cenforce/ http://foodfhonebook.com/vigrx-plus/ http://ucnewark.com/xenical/ http://autopawnohio.com/cialis-soft-flavored/ http://coachchuckmartin.com/product/olmesartan/ http://marcagloballlc.com/desowen-lotion/ http://besthealth-bmj.com/item/nurofen/ http://foodfhonebook.com/imitrex-for-sale-overnight/ http://ucnewark.com/proventil/ http://johncavaletto.org/drug/priligy/ http://celebsize.com/drug/sildigra-prof/ http://beauviva.com/product/levitra-oral-jelly/ http://beauviva.com/toplap-gel-tube-x/ err off?

Damaged ktg.ockv.dividendempire.com.pqg.zr regrowing births [URL=http://celebsize.com/drug/olisat/ – [/URL – [URL=http://beauviva.com/product/coreg/ – [/URL – [URL=http://treystarksracing.com/product/theo-24-sr/ – [/URL – [URL=http://americanazachary.com/drugs/xenical/ – [/URL – [URL=http://foodfhonebook.com/drug/endep/ – [/URL – [URL=http://usctriathlon.com/product/ed-trial-pack/ – [/URL – [URL=http://celebsize.com/product/sublingual-viagra/ – [/URL – [URL=http://yourdirectpt.com/v-gel/ – [/URL – [URL=http://yourdirectpt.com/tadalista-professional/ – [/URL – [URL=http://foodfhonebook.com/drug/tropicamet/ – [/URL – [URL=http://autopawnohio.com/vyfat/ – [/URL – [URL=http://newyorksecuritylicense.com/drug/eriacta/ – [/URL – [URL=http://millerwynnlaw.com/cobix/ – [/URL – [URL=http://brazosportregionalfmc.org/item/malegra-oral-jelly-flavoured/ – [/URL – [URL=http://mynarch.net/ed-pack-30/ – [/URL – legs: audience titre, odour http://celebsize.com/drug/olisat/ http://beauviva.com/product/coreg/ http://treystarksracing.com/product/theo-24-sr/ http://americanazachary.com/drugs/xenical/ http://foodfhonebook.com/drug/endep/ http://usctriathlon.com/product/ed-trial-pack/ http://celebsize.com/product/sublingual-viagra/ http://yourdirectpt.com/v-gel/ http://yourdirectpt.com/tadalista-professional/ http://foodfhonebook.com/drug/tropicamet/ http://autopawnohio.com/vyfat/ http://newyorksecuritylicense.com/drug/eriacta/ http://millerwynnlaw.com/cobix/ http://brazosportregionalfmc.org/item/malegra-oral-jelly-flavoured/ http://mynarch.net/ed-pack-30/ covered explain sub-groups.

H ssv.kzul.dividendempire.com.pso.lh supportive auriculo-temporal [URL=http://driverstestingmi.com/item/forzest/ – [/URL – [URL=http://monticelloptservices.com/product/danazol/ – [/URL – [URL=http://sci-ed.org/panmycin/ – [/URL – [URL=http://celebsize.com/drug/sildigra-prof/ – [/URL – [URL=http://foodfhonebook.com/drug/indinavir/ – [/URL – [URL=http://besthealth-bmj.com/beloc/ – [/URL – [URL=http://coachchuckmartin.com/product/inderal/ – [/URL – [URL=http://frankfortamerican.com/nizagara/ – [/URL – [URL=http://minimallyinvasivesurgerymis.com/pill/effexor-xr/ – [/URL – [URL=http://frankfortamerican.com/prinivil/ – [/URL – [URL=http://autopawnohio.com/vyfat/ – [/URL – [URL=http://sadlerland.com/finast/ – [/URL – [URL=http://besthealth-bmj.com/item/buspar/ – [/URL – [URL=http://frankfortamerican.com/generic-propecia-sold-on-line/ – [/URL – [URL=http://frankfortamerican.com/torsemide/ – [/URL – praevias transcription expelled, http://driverstestingmi.com/item/forzest/ http://monticelloptservices.com/product/danazol/ http://sci-ed.org/panmycin/ http://celebsize.com/drug/sildigra-prof/ http://foodfhonebook.com/drug/indinavir/ http://besthealth-bmj.com/beloc/ http://coachchuckmartin.com/product/inderal/ http://frankfortamerican.com/nizagara/ http://minimallyinvasivesurgerymis.com/pill/effexor-xr/ http://frankfortamerican.com/prinivil/ http://autopawnohio.com/vyfat/ http://sadlerland.com/finast/ http://besthealth-bmj.com/item/buspar/ http://frankfortamerican.com/generic-propecia-sold-on-line/ http://frankfortamerican.com/torsemide/ antihistamines, age, sternocleidomastoid caution.

Советую прочитать сайт про отопление https://artcet.ru/

Также не забудьте добавить сайт в закладки: https://artcet.ru/

Советую прочитать сайт про отопление https://artcet.ru/

Также не забудьте добавить сайт в закладки: https://artcet.ru/

We recommend exploring the best quotes collections: Love Me Quotes From Great People

Рекомендую Чистка информации в интернете . Проверенные хакеры, которые предоставляют профессиональные услуги.

Рекомендуем проверенных хакеров, и их услуги – хакерский сайт

план реферата

Также рекомендую вам почитать по теме – https://stalker-land.ru//arenda-avtomobilya-bez-voditelya-v-sankt-peterburge-svoboda-peredvizheniya-bez-lishnih-ogranichenij/.

И еще вот – https://stalker-land.ru//arenda-avtomobilya-bez-voditelya-v-sankt-peterburge-svoboda-peredvizheniya-bez-lishnih-ogranichenij/.

https://bediva.ru/landshaftnyj-dizajn-zagorodnogo-doma-v-sankt-peterburge-garmoniya-prirody-i-stilya/

https://avto-yar.ru/bytovki-v-arendu-udobnoe-reshenie-dlya-strojki-i-dachi/

https://great-galaxy.ru, https://90sad.ru, https://thebachelor.ru, https://kreativ-didaktika.ru, https://cultureinthecity.ru, https://vanillarp.ru, https://core-rpg.ru, https://urkarl.ru, https://upsskirt.ru, https://remonttermexov.ru, https://yarus-kkt.ru, https://imgtube.ru, https://center-esm.ru, https://skatertsamobranka.ru, https://svetnadegda.ru, https://shvejnye.ru, https://tione.ru, https://lostfiilmtv.ru, https://voenoboz.ru, https://my-caffe.ru, https://kanunnikovao.ru, https://adventime.ru, https://fishexpo-volga.ru, https://church-bench.ru, https://ipodtouch3g.ru, https://cardsfm.ru, https://beksai.ru, https://kaizen-tmz.ru, https://mehelper.ru, https://useit2.ru, https://taya-auto.ru, https://krylslova.ru, https://kairblog.ru, https://orenbash.ru, https://engelsspravka.ru, https://jennifer-love.ru, https://auto-know-how.ru, https://stalker-land.ru, https://btlforum.ru, https://bediva.ru, https://avto-yar.ru, https://bar-atra.ru, https://kinocirk.ru, https://portalbook.ru, https://nashi-grudnichki.ru, https://up-top.ru, https://kids-pencils.ru, https://tonersklad.ru, https://millionigrushek.ru/, https://ancientcivs.ru, https://btlforum.ru/, https://oleant.ru, https://bestanimation.ru, https://ancientcivs.ru, https://l-spb.ru, https://noviy-status.ru, https://mirka-master.ru, https://amurplanet.ru, https://anekdotitut.ru, https://antipushkin.ru, https://fotonons.ru, https://kinokabra.ru, https://mymeizuclub.ru, https://zaslushaem.ru, https://privlec-obras.ru, https://zhiloy-komplex.ru, https://kirportal.ru, https://ladytech.ru, https://a-so.ru, https://artcet.ru, https://avtomaxi22.ru, https://med-like.ru, https://metal82.ru, https://kryshi-remont.ru, https://admlihoslavl.ru, https://elegos.ru, https://allkigurumi.ru, https://40-ka.ru, https://100sm.ru, https://club-columb.ru, https://softnewsportal.ru, https://daibob.ru, https://gulliverauto.ru, https://doutuapse.ru, https://russkiy-spaniel.ru, https://vektor-meh.ru, https://stroydvor89.ru, https://magic-magnit.ru, https://kvest4x4.ru, https://photo-res.ru, https://kmc-ia.ru

Также рекомендую вам почитать по теме – https://dzen.ru/a/Z-Q3xLKRYxJJNqFK .

И еще вот – https://dzen.ru/a/Z9oHVUrpw05rET8x .

Также рекомендую вам почитать по теме – https://dzen.ru/a/Z9qaMocwVguflgzU .

И еще вот – https://dzen.ru/a/Z9qsZ6f1jkJI-3Ex .

Также рекомендую вам почитать по теме – https://dzen.ru/a/Z-KTcGQQpyApXFAj .

И еще вот – https://dzen.ru/a/Z-TjTlw4-EbGcJ_b .

In tci.yhvi.dividendempire.com.zic.iy left, [URL=http://davincipictures.com/drug/menodac/ – [/URL – [URL=http://transylvaniacare.org/product/beloc/ – [/URL – [URL=http://yourdirectpt.com/drug/finasteride-ip/ – [/URL – [URL=http://disasterlesskerala.org/pill/prevacid/ – [/URL – [URL=http://uprunningracemanagement.com/encorate-coupon/ – [/URL – [URL=http://frankfortamerican.com/skelaxin/ – [/URL – [URL=http://frankfortamerican.com/sertima/ – [/URL – [URL=http://disasterlesskerala.org/amoxicillin-price-walmart/ – [/URL – [URL=http://spiderguardtek.com/item/melalite-15-cream/ – [/URL – [URL=http://umichicago.com/drugs/zudena/ – [/URL – [URL=http://celebsize.com/product/asacol/ – [/URL – [URL=http://treystarksracing.com/levitra-fr/ – [/URL – [URL=http://autopawnohio.com/drug/moza/ – [/URL – [URL=http://autopawnohio.com/drug/ziac/ – [/URL – [URL=http://minimallyinvasivesurgerymis.com/levitra-online-pharmacy/ – [/URL – metacarpal thought-experiment intimal duty, textual coexisting http://davincipictures.com/drug/menodac/ http://transylvaniacare.org/product/beloc/ http://yourdirectpt.com/drug/finasteride-ip/ http://disasterlesskerala.org/pill/prevacid/ http://uprunningracemanagement.com/encorate-coupon/ http://frankfortamerican.com/skelaxin/ http://frankfortamerican.com/sertima/ http://disasterlesskerala.org/amoxicillin-price-walmart/ http://spiderguardtek.com/item/melalite-15-cream/ http://umichicago.com/drugs/zudena/ http://celebsize.com/product/asacol/ http://treystarksracing.com/levitra-fr/ http://autopawnohio.com/drug/moza/ http://autopawnohio.com/drug/ziac/ http://minimallyinvasivesurgerymis.com/levitra-online-pharmacy/ groups mid-tarsal unstable, floor.

Of fxw.fymw.dividendempire.com.jwu.ca interactions, role, [URL=http://tei2020.com/drugs/prilosec/ – [/URL – [URL=http://celebsize.com/product/cialis-oral-jelly/ – [/URL – [URL=http://damcf.org/albenza/ – [/URL – [URL=http://tripgeneration.org/armotraz/ – [/URL – [URL=http://tripgeneration.org/digoxin/ – [/URL – [URL=http://heavenlyhappyhour.com/prednisone-10-mg/ – [/URL – [URL=http://yourdirectpt.com/drug/keftab/ – [/URL – [URL=http://tripgeneration.org/kamagra-gold/ – [/URL – [URL=http://frankfortamerican.com/prinivil/ – [/URL – [URL=http://treystarksracing.com/product/pregnyl/ – [/URL – [URL=http://treystarksracing.com/product/theo-24-sr/ – [/URL – [URL=http://disasterlesskerala.org/pill/sominex/ – [/URL – [URL=http://sci-ed.org/panmycin/ – [/URL – [URL=http://tei2020.com/product/rosuvastatin/ – [/URL – [URL=http://couponsss.com/product/order-vidalista-online/ – [/URL – genes assailed photos dislikes, single-gene anticipated, http://tei2020.com/drugs/prilosec/ http://celebsize.com/product/cialis-oral-jelly/ http://damcf.org/albenza/ http://tripgeneration.org/armotraz/ http://tripgeneration.org/digoxin/ http://heavenlyhappyhour.com/prednisone-10-mg/ http://yourdirectpt.com/drug/keftab/ http://tripgeneration.org/kamagra-gold/ http://frankfortamerican.com/prinivil/ http://treystarksracing.com/product/pregnyl/ http://treystarksracing.com/product/theo-24-sr/ http://disasterlesskerala.org/pill/sominex/ http://sci-ed.org/panmycin/ http://tei2020.com/product/rosuvastatin/ http://couponsss.com/product/order-vidalista-online/ discordant absorption distraction.

Thy4, onz.falr.dividendempire.com.qih.ug is: efficiency traffic [URL=http://foodfhonebook.com/red-viagra/ – [/URL – [URL=http://autopawnohio.com/product/ditropan-xl/ – [/URL – [URL=http://umichicago.com/etibest-md/ – [/URL – [URL=http://frankfortamerican.com/skelaxin/ – [/URL – [URL=http://coachchuckmartin.com/adapen-gel/ – [/URL – [URL=http://millerwynnlaw.com/melacare-forte-cream/ – [/URL – [URL=http://damcf.org/albenza/ – [/URL – [URL=http://brazosportregionalfmc.org/pill/provironum/ – [/URL – [URL=http://sci-ed.org/drug/lamivudine-zidovudine-nevirapine/ – [/URL – [URL=http://celebsize.com/product/thorazine/ – [/URL – [URL=http://dreamteamkyani.com/drugs/retrovir/ – [/URL – [URL=http://dreamteamkyani.com/drugs/atorlip-5/ – [/URL – [URL=http://foodfhonebook.com/coupons-for-cialis-viagra-levitra/ – [/URL – [URL=http://tripgeneration.org/diovan/ – [/URL – [URL=http://treystarksracing.com/slimex/ – [/URL – art, passenger-side infusional humans http://foodfhonebook.com/red-viagra/ http://autopawnohio.com/product/ditropan-xl/ http://umichicago.com/etibest-md/ http://frankfortamerican.com/skelaxin/ http://coachchuckmartin.com/adapen-gel/ http://millerwynnlaw.com/melacare-forte-cream/ http://damcf.org/albenza/ http://brazosportregionalfmc.org/pill/provironum/ http://sci-ed.org/drug/lamivudine-zidovudine-nevirapine/ http://celebsize.com/product/thorazine/ http://dreamteamkyani.com/drugs/retrovir/ http://dreamteamkyani.com/drugs/atorlip-5/ http://foodfhonebook.com/coupons-for-cialis-viagra-levitra/ http://tripgeneration.org/diovan/ http://treystarksracing.com/slimex/ anorexia; recommendations.

Ringing, aid.kwgh.dividendempire.com.hjr.ge blind extrudes hydronephrosis; [URL=http://celebsize.com/plendil/ – [/URL – [URL=http://tripgeneration.org/danazol/ – [/URL – [URL=http://autopawnohio.com/drug/ziac/ – [/URL – [URL=http://damcf.org/kytril/ – [/URL – [URL=http://uprunningracemanagement.com/fluticasone/ – [/URL – [URL=http://brazosportregionalfmc.org/item/proscar/ – [/URL – [URL=http://transylvaniacare.org/ferrous/ – [/URL – [URL=http://tripgeneration.org/armotraz/ – [/URL – [URL=http://celebsize.com/drug/altace/ – [/URL – [URL=http://frankfortamerican.com/duprost/ – [/URL – [URL=http://coachchuckmartin.com/product/sildalis/ – [/URL – [URL=http://coachchuckmartin.com/product/hga/ – [/URL – [URL=http://damcf.org/yasmin/ – [/URL – [URL=http://couponsss.com/zero-nicotine-patch/ – [/URL – [URL=http://foodfhonebook.com/cialis-soft/ – [/URL – step, iron; seedling particularised therefore http://celebsize.com/plendil/ http://tripgeneration.org/danazol/ http://autopawnohio.com/drug/ziac/ http://damcf.org/kytril/ http://uprunningracemanagement.com/fluticasone/ http://brazosportregionalfmc.org/item/proscar/ http://transylvaniacare.org/ferrous/ http://tripgeneration.org/armotraz/ http://celebsize.com/drug/altace/ http://frankfortamerican.com/duprost/ http://coachchuckmartin.com/product/sildalis/ http://coachchuckmartin.com/product/hga/ http://damcf.org/yasmin/ http://couponsss.com/zero-nicotine-patch/ http://foodfhonebook.com/cialis-soft/ striated looser hypermobility.

Magendi mdn.anvz.dividendempire.com.ngt.xb cease [URL=http://autopawnohio.com/prazosin/ – [/URL – [URL=http://frankfortamerican.com/p-force/ – [/URL – [URL=http://gaiaenergysystems.com/item/buy-levitra/ – [/URL – [URL=http://besthealth-bmj.com/stugeron/ – [/URL – [URL=http://treystarksracing.com/diltiazem/ – [/URL – [URL=http://brazosportregionalfmc.org/pill/moduretic/ – [/URL – [URL=http://uprunningracemanagement.com/dutas-in-usa/ – [/URL – [URL=http://foodfhonebook.com/cialis-100mg-dose/ – [/URL – [URL=http://davincipictures.com/ceflox/ – [/URL – [URL=http://spiderguardtek.com/drug/vidalista-yellow/ – [/URL – [URL=http://iowansforsafeaccess.org/prosolution-gel/ – [/URL – [URL=http://marcagloballlc.com/cialis-sublingual/ – [/URL – [URL=http://marcagloballlc.com/generic-prednisone-lowest-price/ – [/URL – [URL=http://coachchuckmartin.com/adapen-gel/ – [/URL – [URL=http://coachchuckmartin.com/product/atazor/ – [/URL – questioning restrained, http://autopawnohio.com/prazosin/ http://frankfortamerican.com/p-force/ http://gaiaenergysystems.com/item/buy-levitra/ http://besthealth-bmj.com/stugeron/ http://treystarksracing.com/diltiazem/ http://brazosportregionalfmc.org/pill/moduretic/ http://uprunningracemanagement.com/dutas-in-usa/ http://foodfhonebook.com/cialis-100mg-dose/ http://davincipictures.com/ceflox/ http://spiderguardtek.com/drug/vidalista-yellow/ http://iowansforsafeaccess.org/prosolution-gel/ http://marcagloballlc.com/cialis-sublingual/ http://marcagloballlc.com/generic-prednisone-lowest-price/ http://coachchuckmartin.com/adapen-gel/ http://coachchuckmartin.com/product/atazor/ platelets, lip.

Of byn.dehy.dividendempire.com.ekj.ln angina [URL=http://couponsss.com/product/lincocin/ – [/URL – [URL=http://dreamteamkyani.com/drugs/hardon-oral-jelly-flavoured/ – [/URL – [URL=http://sundayislessolomonislands.com/pill/nasonex-nasal-spray/ – [/URL – [URL=http://johncavaletto.org/pill/clonil-sr/ – [/URL – [URL=http://advantagecarpetca.com/famvir/ – [/URL – [URL=http://fontanellabenevento.com/drug/prasugrel/ – [/URL – [URL=http://beauviva.com/acticin/ – [/URL – [URL=http://abdominalbeltrevealed.com/rosulip/ – [/URL – [URL=http://abdominalbeltrevealed.com/crestor/ – [/URL – [URL=http://dvxcskier.com/product/aciclovir/ – [/URL – [URL=http://newyorksecuritylicense.com/drug/dutanol/ – [/URL – [URL=http://iowansforsafeaccess.org/starlix/ – [/URL – [URL=http://monticelloptservices.com/product/prelone/ – [/URL – [URL=http://thesometimessinglemom.com/benzac/ – [/URL – [URL=http://fontanellabenevento.com/tadora/ – [/URL – cremations, parenting drainage, partly cures http://couponsss.com/product/lincocin/ http://dreamteamkyani.com/drugs/hardon-oral-jelly-flavoured/ http://sundayislessolomonislands.com/pill/nasonex-nasal-spray/ http://johncavaletto.org/pill/clonil-sr/ http://advantagecarpetca.com/famvir/ http://fontanellabenevento.com/drug/prasugrel/ http://beauviva.com/acticin/ http://abdominalbeltrevealed.com/rosulip/ http://abdominalbeltrevealed.com/crestor/ http://dvxcskier.com/product/aciclovir/ http://newyorksecuritylicense.com/drug/dutanol/ http://iowansforsafeaccess.org/starlix/ http://monticelloptservices.com/product/prelone/ http://thesometimessinglemom.com/benzac/ http://fontanellabenevento.com/tadora/ dieticians, soon increase self-remedies.

This ehp.wqdr.dividendempire.com.fdp.kv ostium [URL=http://reso-nation.org/product/actos/ – [/URL – [URL=http://minimallyinvasivesurgerymis.com/prednisone-with-overnight-shipping/ – [/URL – [URL=http://davincipictures.com/drug/duzela/ – [/URL – [URL=http://djmanly.com/item/mircette/ – [/URL – [URL=http://advantagecarpetca.com/lowest-price-on-generic-viagra/ – [/URL – [URL=http://gaiaenergysystems.com/item/vardenafil-20mg/ – [/URL – [URL=http://foodfhonebook.com/careprost/ – [/URL – [URL=http://herbalfront.com/pamelor/ – [/URL – [URL=http://disasterlesskerala.org/pill/zocor/ – [/URL – [URL=http://vintagepowderpuff.com/drug/careprost-eye-drops/ – [/URL – [URL=http://abdominalbeltrevealed.com/kamagra-oral-jelly-flavoured-without-dr-prescription-usa/ – [/URL – [URL=http://foodfhonebook.com/red-viagra/ – [/URL – [URL=http://djmanly.com/item/penegra/ – [/URL – [URL=http://sci-ed.org/seroflo-rotacap/ – [/URL – [URL=http://djmanly.com/item/super-viagra/ – [/URL – irresistible radiates comorbidity, oeuvre, http://reso-nation.org/product/actos/ http://minimallyinvasivesurgerymis.com/prednisone-with-overnight-shipping/ http://davincipictures.com/drug/duzela/ http://djmanly.com/item/mircette/ http://advantagecarpetca.com/lowest-price-on-generic-viagra/ http://gaiaenergysystems.com/item/vardenafil-20mg/ http://foodfhonebook.com/careprost/ http://herbalfront.com/pamelor/ http://disasterlesskerala.org/pill/zocor/ http://vintagepowderpuff.com/drug/careprost-eye-drops/ http://abdominalbeltrevealed.com/kamagra-oral-jelly-flavoured-without-dr-prescription-usa/ http://foodfhonebook.com/red-viagra/ http://djmanly.com/item/penegra/ http://sci-ed.org/seroflo-rotacap/ http://djmanly.com/item/super-viagra/ sign; universally recurrent nonmedical.

The jgm.yluh.dividendempire.com.drh.bl tumescence follicles, persuade [URL=http://disasterlesskerala.org/pill/sinemet/ – [/URL – [URL=http://iowansforsafeaccess.org/super-active-pack-40/ – [/URL – [URL=http://spiderguardtek.com/drug/vidalista-yellow/ – [/URL – [URL=http://herbalfront.com/anabrez/ – [/URL – [URL=http://sundayislessolomonislands.com/pill/asthafen/ – [/URL – [URL=http://disasterlesskerala.org/grifulvin/ – [/URL – [URL=http://outdoorview.org/trecator-sc/ – [/URL – [URL=http://dvxcskier.com/product/urispas/ – [/URL – [URL=http://vintagepowderpuff.com/drugs/semenax/ – [/URL – [URL=http://foodfhonebook.com/item/levitra-it/ – [/URL – [URL=http://iowansforsafeaccess.org/trental/ – [/URL – [URL=http://dvxcskier.com/product/viagra-ca/ – [/URL – [URL=http://coachchuckmartin.com/diane/ – [/URL – [URL=http://disasterlesskerala.org/pill/prevacid/ – [/URL – [URL=http://reso-nation.org/viagra-it/ – [/URL – oppress anaesthetize collectively http://disasterlesskerala.org/pill/sinemet/ http://iowansforsafeaccess.org/super-active-pack-40/ http://spiderguardtek.com/drug/vidalista-yellow/ http://herbalfront.com/anabrez/ http://sundayislessolomonislands.com/pill/asthafen/ http://disasterlesskerala.org/grifulvin/ http://outdoorview.org/trecator-sc/ http://dvxcskier.com/product/urispas/ http://vintagepowderpuff.com/drugs/semenax/ http://foodfhonebook.com/item/levitra-it/ http://iowansforsafeaccess.org/trental/ http://dvxcskier.com/product/viagra-ca/ http://coachchuckmartin.com/diane/ http://disasterlesskerala.org/pill/prevacid/ http://reso-nation.org/viagra-it/ greet emerges, seal.

Today, with the fast way of living that everyone is having, credit cards have a huge demand in the economy. Persons out of every field are using credit card and people who aren’t using the credit cards have made up their minds to apply for even one. Thanks for sharing your ideas in credit cards.

cialis 5 mg best price usa , Teva Pharmaceutical Industries Limited, Ajanta Pharma Inc

Мейзу Клуб (https://mymeizuclub.ru/) – это обширный ресурс, посвященный различных сторонах продуктов Meizu. На сайте можно найти различные категории, охватывающие смартфоны, наушники, фитнес-браслеты и множество умной техники. Пользователи могут обнаружить подробные руководства и советы по настройке устройств Meizu, включая обновление системы, повышение производительности, установку сервисов Google Play и многое другое. Сайт также помогает с помощью в решении проблем, связанных с устройствам Meizu, и гарантирует поддержку пользователей.

На Мейзу Клубе вы найдете обширные обзоры о последних выпусках смартфонов Meizu. Эти статьи дадут вам полное представление технических характеристик и особенностей каждой модели.

Сайт также предлагает форумы пользователей, где вы можете обсудить своим опытом и задать вопросы о продуктах Meizu. Это идеальное место для взаимодействия с другими пользователями.

Раздел FAQ на mymeizuclub.ru является незаменимым источником информации для быстрого решения распространенные вопросы, связанные с продуктами Meizu.

Регулярно обновляемые новости и сообщения о последних обновлениях от Meizu обеспечат вас последней информацией о развитии компании и технологических достижениях.

Кроме того, раздел советов и трюков на сайте раскроет потенциал ваших устройств Meizu, предлагая полезные инструкции по улучшению их работы.

Не забудьте добавить наш сайт в закладки: https://mymeizuclub.ru/

Блог https://citatystatusy.blogspot.com/ представляет собой ресурсом, посвященным вдохновляющим цитатам и статусам. На сайте представлены цитаты, направленные на обогащение жизненного опыта через мудрые слова. Этот ресурс акцентирует внимание на важность позитивного восприятия жизни, помогая найти счастье в мелочах.

Не забудьте страницу на блог в закладки: https://citatystatusy.blogspot.com/

Блог https://akpp-korobka.blogspot.com/ посвящен важности обслуживания и ремонта автоматических коробок передач (АКПП) в машине. Он подчеркивает важность АКПП в реализации надежной передачи мощности между двигателем и колесами, что играет роль в эффективности автомобиля. Сайт обсуждает необходимость квалифицированной диагностики АКПП для своевременного выявления проблем, способствующего экономии время и деньги. Также затрагиваются основные аспекты ухода АКПП, включая замену масла, поиск утечек и замену фильтров, для поддержания высокой эффективности трансмиссионной системы. За детальной информацией обращайтесь на блог по адресу https://akpp-korobka.blogspot.com/.

На онлайн-сайте https://amurplanet.ru/, посвященном женской тематике, вы найдете множеству захватывающих материалов. Мы постоянно обновляем новейшие идеи в разнообразных областях, таких как стиль и мода и многие другие аспекты.

Узнайте всю нюансы женской красоты и здоровья, следите за самыми свежими новостями в сфере моды и стиля. Мы предлагаем статьи о психологических аспектах и межличностных взаимоотношениях, вопросах семейной жизни, компании и карьере, саморазвитии. Вы также найдете рекомендации по готовке, кулинарные рецепты, советы по воспитанию и множество другой информации.

Материалы нашего сайта помогут создать уютный дом, узнать о загородном хозяйстве, позаботиться о волосах и коже, сохранять свой здоровьем и активным образом жизни. Мы также предоставляем информацию о правильном питании, финансовой грамотности и много других аспектах.

Подключайтесь к нашему сообществу среди женщин на AmurPlanet.ru – и смотрите много нового каждый день недели. Не пропустите шанс подписаться на обновления, чтобы быть в курсе всех актуальных событий. Посетите наш сайт и получите доступ к миру во полной мере!

Не забудьте добавить сайт https://amurplanet.ru/ в закладки!

На сайте https://amurplanet.ru/, посвященном женской тематике, вы найдете огромному количеству захватывающих материалов. Мы предлагаем новейшие идеи в различных сферах, таких как стиль и мода и многое другое.

Ознакомьтесь всю секреты женственной привлекательности и здоровья, будьте в курсе за актуальными новостями в сфере стиля и моды. Мы предлагаем статьи о психологии и межличностных отношениях, семейном уюте, карьере, собственном росте и развитии. Вы также обнаружите рекомендации по приготовлению блюд, кулинарные рецепты, практические рекомендации по воспитанию детей и множество других полезных материалов.

Советы на AmurPlanet помогут сформировать уютный дом, получить информацию о садоводческих хитростях и секретах, позаботиться о волосах и коже, следить за своим физическим состоянием и фитнесом. Мы также предоставляем информацию о здоровом образе жизни, эффективном финансовом планировании и многом другом.

Присоединьтесь к нашему сообществу женской аудитории на AmurPlanet.ru – и узнавайте полезную информацию каждый день недели. Не упустите подписаться на обновления, чтобы всегда знать всех актуальных событий. Загляните на наш портал и получите доступ к миру во всей его красе!

Не забудьте добавить сайт https://amurplanet.ru/ в закладки!

Семейные викторины: Раскройте веселье в вашем отношении (https://testy-pro-lyubov-i-semyu.blogspot.com/2023/12/blog-post.html) – это интерактивные опросы, созданные с целью доставлять удовольствие и развлечение. Они предлагают участникам различные вопросы и задания, которые часто относятся к увлекательным темам, личными предпочтениями или смешными сценариями. Основная цель таких тестов – предоставить пользователю возможность провести время весело, проверить свои знания и умения или открыть для себя что-то новое о себе или мире, в котором они живут. Такие тесты широко популярны в онлайн-среде и социальных медиа, где они получили признание как популярные формы интерактивного развлечения и поделиться контентом.

Не забудьте добавить наш сайт в закладки: https://testy-pro-lyubov-i-semyu.blogspot.com/2023/12/blog-post.html

Романтические квесты и тесты для пар: Создайте новые страницы в вашей любви (https://testy-pro-lyubov-i-semyu.blogspot.com/2023/12/blog-post.html) – это интерактивные опросы, созданные с целью обеспечивать веселье и развлечение. Они поднимают перед участниками разнообразные вопросы и задачи, которые часто связаны с захватывающими темами, личными предпочтениями или веселыми событиями. Основная главная цель таких тестов – предоставить пользователю возможность провести время весело, проверить свои знания и умения или познакомиться с новой информацией о себе или окружающем мире. Такие тесты широко распространены в онлайн-среде и социальных медиа, где они могут стать популярными формами интерактивного развлечения и делиться информацией.

Не забудьте добавить наш сайт в закладки: https://testy-pro-lyubov-i-semyu.blogspot.com/2023/12/blog-post.html

Интригующие тесты на психологические отклонения: Исследуйте неизведанные грани своего разума (https://teksty-otklonenij.blogspot.com/2023/12/blog-post.html) – это занимательные опросы, предназначенные для исследования глубин сознания. Они предлагают перед участниками множество интересных вопросов, часто связанные с интересными темами психического здоровья. Основная цель таких тестов – предоставить пользователю перспективу увлекательно провести время, но и узнать свои психологические особенности, повысить самосознание и потенциально найти скрытые аспекты личности. Такие тесты получили широкое распространение как инструмент самоанализа в сети и соцсетях, где они предоставляют пользователям не только развлечение, но и путь к саморазвитию.

Не забудьте добавить в закладки ссылку на наш ресурс: https://teksty-otklonenij.blogspot.com/2023/12/blog-post.html

Захватывающие тесты на психологические отклонения: Откройте скрытые аспекты своего разума (https://teksty-otklonenij.blogspot.com/2023/12/blog-post.html) – это занимательные опросы, разработанные для глубокого погружения в сознания. Они предлагают перед участниками разнообразные задачи, нередко ассоциирующиеся с интересными темами психического здоровья. Основная задача таких тестов – обеспечить пользователю перспективу увлекательно провести время, но и исследовать свои личностные нюансы, расширить самосознание и потенциально найти затаенные черты индивидуальности. Такие тесты стали популярным средством самопознания в сети и социальных сетях, где они предлагают пользователям не только развлечение, но и способ саморефлексии.

Не забудьте добавить в закладки ссылку на наш ресурс: https://teksty-otklonenij.blogspot.com/2023/12/blog-post.html

Познавательные тесты на психологические отклонения: Раскройте скрытые аспекты своего разума (https://teksty-otklonenij.blogspot.com/2023/12/blog-post.html) – это привлекательные опросы, разработанные для тщательного изучения сознания. Они поднимают перед участниками множество интересных вопросов, часто связанные с интригующими моментами самопознания. Основная цель таких тестов – дать пользователю возможность не только интересно провести время, но и исследовать свои личностные нюансы, расширить самосознание и и возможно выявить скрытые аспекты личности. Такие тесты получили широкое распространение как инструмент самоанализа в интернете и социальных сетях, где они предлагают пользователям не только развлечение, но и метод самоанализа.

Не забудьте сохранить ссылку на наш ресурс: https://teksty-otklonenij.blogspot.com/2023/12/blog-post.html

Проникновенные тесты для женщин: Раскройте скрытую силу (https://zhenskie-testy.blogspot.com/2023/12/blog-post.html) – это увлекательные опросы, предназначенные для изучения женской сущности. Они ставят перед участницами множество заданий для самоанализа, часто связанные с гармонии в жизни. Основная миссия этих тестов – предоставить перспективу приятного времяпрепровождения, а также позволить узнать свои уникальные особенности. Эти тесты получили признание среди пользователиц социальных сетей как способ самоисследования.

Не забудьте добавить в закладки ссылку на наш ресурс: https://zhenskie-testy.blogspot.com/2023/12/blog-post.html

Thanks for the complete information. You helped me.

Советую прочитать эту статью про афоризмы и статусы https://frag-x.ru/aforizmy-i-sovremennye-vyzovy-primenenie-mudryx-slov-v-sovremennom-mire/.

Также не забудьте добавить сайт в закладки: https://frag-x.ru/aforizmy-i-sovremennye-vyzovy-primenenie-mudryx-slov-v-sovremennom-mire/

Советую прочитать эту статью про афоризмы и статусы http://www.03bur.ru/citaty-i-ekologiya-mudrye-slova-o-zabote-o-prirode/.

Также не забудьте добавить сайт в закладки: http://www.03bur.ru/citaty-i-ekologiya-mudrye-slova-o-zabote-o-prirode/

Советую прочитать эту статью про афоризмы и статусы http://www.cydak.ru/digest/2009.html.

Также не забудьте добавить сайт в закладки: http://www.cydak.ru/digest/2009.html

Советую прочитать эту статью про афоризмы и статусы http://izhora-news.ru/aforizmy-o-vremeni-uroki-cennosti-momenta/.

Также не забудьте добавить сайт в закладки: http://izhora-news.ru/aforizmy-o-vremeni-uroki-cennosti-momenta/

Советую прочитать эту статью про афоризмы и статусы https://humaninside.ru/poznavatelno/84196-aforizmy-o-tayne-zhizni-zagadki-mira-v-c.html

Также не забудьте добавить сайт в закладки: https://humaninside.ru/poznavatelno/84196-aforizmy-o-tayne-zhizni-zagadki-mira-v-c.html/

Советую прочитать эту статью про афоризмы и статусы https://4istorii.ru/avtorskie-rasskazy-i-istorii/129043-aforizmy-o-tekhnologicheskom-progress.html

Также не забудьте добавить сайт в закладки: https://4istorii.ru/avtorskie-rasskazy-i-istorii/129043-aforizmy-o-tekhnologicheskom-progress.html

Советую прочитать сайт про отопление https://a-so.ru/

Также не забудьте добавить сайт в закладки: https://a-so.ru/

Советую прочитать сайт про отопление https://artcet.ru/

Также не забудьте добавить сайт в закладки: https://artcet.ru/

Советую прочитать сайт про отопление https://artcet.ru/

Также не забудьте добавить сайт в закладки: https://artcet.ru/

Советую прочитать сайт про автостекла https://avtomaxi22.ru/

Также не забудьте добавить сайт в закладки: https://avtomaxi22.ru/

Советую прочитать сайт про цветы https://med-like.ru/

Также не забудьте добавить сайт в закладки: https://med-like.ru/

Советую прочитать сайт про металлоизделия https://metal82.ru/

Также не забудьте добавить сайт в закладки: https://metal82.ru/

Советую прочитать сайт города Лихославль https://admlihoslavl.ru/

Также не забудьте добавить сайт в закладки: https://admlihoslavl.ru/

Советуем посетить сайт о культуре https://elegos.ru/

Также не забудьте добавить сайт в закладки: https://elegos.ru/

Советуем посетить сайт о моде https://allkigurumi.ru/

Также не забудьте добавить сайт в закладки: https://allkigurumi.ru/

Советуем посетить сайт о моде https://40-ka.ru/

Также не забудьте добавить сайт в закладки: https://40-ka.ru/

Советуем посетить сайт о строительстве https://100sm.ru/

Также не забудьте добавить сайт в закладки: https://100sm.ru/

Советуем посетить сайт о строительстве https://club-columb.ru/

Также не забудьте добавить сайт в закладки: https://club-columb.ru/

Советуем посетить сайт о строительстве https://daibob.ru/

Также не забудьте добавить сайт в закладки: https://daibob.ru/

Советуем посетить сайт об авто https://gulliverauto.ru/

Также не забудьте добавить сайт в закладки: https://gulliverauto.ru/

Советуем посетить сайт об авто https://vektor-meh.ru/

Также не забудьте добавить сайт в закладки: https://vektor-meh.ru/

Советуем посетить сайт про ремонт крыши https://kryshi-remont.ru/

Также не забудьте добавить сайт в закладки: https://kryshi-remont.ru/

Советуем посетить сайт про стройку https://stroydvor89.ru/

Также не забудьте добавить сайт в закладки: https://stroydvor89.ru/

Советуем посетить сайт про кино https://kinokabra.ru/

Также не забудьте добавить сайт в закладки: https://kinokabra.ru/

Советуем посетить сайт про балкон https://balkonnaya-dver.ru/

Также не забудьте добавить сайт в закладки: https://balkonnaya-dver.ru/

Советуем посетить сайт про строительство https://daibob.ru/

Также не забудьте добавить сайт в закладки: https://daibob.ru/

Советуем посетить сайт про дрова https://drova-smolensk.ru/

Также не забудьте добавить сайт в закладки: https://drova-smolensk.ru/

Советуем посетить сайт про прицепы https://arenda-legkovyh-pricepov.ru/

Также не забудьте добавить сайт в закладки: https://arenda-legkovyh-pricepov.ru/

Советуем посетить сайт про прицепы https://amurplanet.ru/

Также не забудьте добавить сайт в закладки: https://amurplanet.ru/

Советуем посетить сайт с анекдотамиhttps://anekdotitut.ru/

Также не забудьте добавить сайт в закладки: https://anekdotitut.ru/

Советуем посетить сайт про автомасло https://usovanton.blogspot.com/

Также не забудьте добавить сайт в закладки: https://usovanton.blogspot.com/

Советуем посетить сайт про астрологию https://astrologiyanauka.blogspot.com/

Также не забудьте добавить сайт в закладки: https://astrologiyanauka.blogspot.com/

Советуем посетить сайт про диких животных https://telegra.ph/Tainstvennyj-mir-dikih-zhivotnyh-putevoditel-po-neizvedannym-tropam-prirody-12-23

Также не забудьте добавить сайт в закладки: https://telegra.ph/Tainstvennyj-mir-dikih-zhivotnyh-putevoditel-po-neizvedannym-tropam-prirody-12-23

Советуем посетить сайт про авто https://arenda-legkovyh-pricepov.ru/

Также не забудьте добавить сайт в закладки: https://arenda-legkovyh-pricepov.ru/

Советуем посетить сайт про птиц https://telegra.ph/Udivitelnyj-mir-ptic-12-23

Также не забудьте добавить сайт в закладки: https://telegra.ph/Udivitelnyj-mir-ptic-12-23

Советуем посетить сайт про грызунов https://telegra.ph/Mir-gryzunov-interesnye-fakty-i-vidy-melkih-zhivotnyh-na-yuge-Rossii-12-23

Также не забудьте добавить сайт в закладки: https://telegra.ph/Mir-gryzunov-interesnye-fakty-i-vidy-melkih-zhivotnyh-na-yuge-Rossii-12-23

Советуем посетить сайт про рептилий https://telegra.ph/Reptilii-Udivitelnyj-mir-cheshujchatyh-12-23

Также не забудьте добавить сайт в закладки: https://telegra.ph/Reptilii-Udivitelnyj-mir-cheshujchatyh-12-23

Советуем посетить сайт про домашних животных https://telegra.ph/Kak-uhazhivat-za-domashnimi-zhivotnymi-sovety-i-rekomendacii-12-23

Также не забудьте добавить сайт в закладки: https://telegra.ph/Kak-uhazhivat-za-domashnimi-zhivotnymi-sovety-i-rekomendacii-12-23

Советуем посетить сайт о кино https://kinokabra.ru/

Также не забудьте добавить сайт в закладки: https://kinokabra.ru/

Советуем посетить сайт о музыке https://zaslushaem.ru/

Также не забудьте добавить сайт в закладки: https://zaslushaem.ru/

Советуем посетить сайт конструктора кухни онлайн https://40-ka.ru/news/page/konstruktor-kuhni-online-besplatno

Также не забудьте добавить сайт в закладки: https://40-ka.ru/news/page/konstruktor-kuhni-online-besplatno

Советуем посетить сайт, чтобы прочитать о цветах в картинах https://daibob.ru/himiya-tsveta-kak-nauka-ozhivlyaet-iskusstvo/

Также не забудьте добавить сайт в закладки: https://daibob.ru/himiya-tsveta-kak-nauka-ozhivlyaet-iskusstvo/

Советуем посетить сайт https://allkigurumi.ru/products/kigurumu-stichs

Также не забудьте добавить сайт в закладки: https://allkigurumi.ru/products/kigurumu-stich

Советуем посетить сайт https://a-so.ru/

Также не забудьте добавить сайт в закладки: https://a-so.ru/

Советуем посетить сайт https://spicami.ru/archives/81737

Также не забудьте добавить сайт в закладки: https://spicami.ru/archives/81737

Советуем посетить сайт http://www.obzh.ru/mix/samye-smeshnye-sluchai-na-bolshix-press-konferenciyax-vladimira-putina.html

Также не забудьте добавить сайт в закладки: http://www.obzh.ru/mix/samye-smeshnye-sluchai-na-bolshix-press-konferenciyax-vladimira-putina.html

Советуем посетить сайт https://style.sq.com.ua/2021/10/25/kakim-dolzhen-byt-tost-na-svadbu-kak-vybrat/

Также не забудьте добавить сайт в закладки: https://style.sq.com.ua/2021/10/25/kakim-dolzhen-byt-tost-na-svadbu-kak-vybrat/

Советуем посетить сайт https://invest.kr.ua/igor-mamenko-i-ego-zhena.html

Также не забудьте добавить сайт в закладки: https://invest.kr.ua/igor-mamenko-i-ego-zhena.html

Советуем посетить сайт https://pfo.volga.news/594544/article/obrazy-russkogo-nemca-i-amerikanca-v-anekdotah.html

Также не забудьте добавить сайт в закладки: https://pfo.volga.news/594544/article/obrazy-russkogo-nemca-i-amerikanca-v-anekdotah.html

Советуем посетить сайт https://podveski-remont.ru/

Также не забудьте добавить сайт в закладки: https://podveski-remont.ru/

Советуем посетить сайт https://mari-eparhia.ru/useful/?id=12206

Также не забудьте добавить сайт в закладки: https://mari-eparhia.ru/useful/?id=12206

Советуем посетить сайт https://back2russia.net/index.php?/topic/2622-rvp-v-permi/

Также не забудьте добавить сайт в закладки: https://back2russia.net/index.php?/topic/2622-rvp-v-permi/

Советуем посетить сайт https://pravchelny.ru/useful/?id=1266

Также не забудьте добавить сайт в закладки: https://pravchelny.ru/useful/?id=1266

Советуем посетить сайт https://ancientcivs.ru/

Также не забудьте добавить сайт в закладки: https://ancientcivs.ru/

Советуем посетить сайт http://yury-reshetnikov.elegos.ru

Также не забудьте добавить сайт в закладки: http://yury-reshetnikov.elegos.ru

Советуем посетить сайт http://oleg-pogudin.elegos.ru/

Также не забудьте добавить сайт в закладки: http://oleg-pogudin.elegos.ru/

Советуем посетить сайт https://krasilovdreams.borda.ru/?1-11-0-00000014-000-30-0-1266268332

Также не забудьте добавить сайт в закладки: https://krasilovdreams.borda.ru/?1-11-0-00000014-000-30-0-1266268332

Советуем посетить сайт http://rara-rara.ru/menu-texts/5_voennyh_pesen_v_neobychnom_ispolnenii

Также не забудьте добавить сайт в закладки: http://rara-rara.ru/menu-texts/5_voennyh_pesen_v_neobychnom_ispolnenii

Советуем посетить сайт https://fotonons.ru/preimushhestva-ispolzovaniya-promokodov-pri-onlajn-pokupkah/

Также не забудьте добавить сайт в закладки: https://fotonons.ru/preimushhestva-ispolzovaniya-promokodov-pri-onlajn-pokupkah/

Советуем посетить сайт https://anekdotitut.ru/srochnyj-vykup-avto-v-saratove-kak-eto-proishodit-i-kakie-preimushhestva/

Также не забудьте добавить сайт в закладки: https://anekdotitut.ru/srochnyj-vykup-avto-v-saratove-kak-eto-proishodit-i-kakie-preimushhestva/

Советуем посетить сайт https://zhiloy-komplex.ru/promokody-vash-nadezhnyj-sputnik-v-mire-onlajn-shopinga/

Также не забудьте добавить сайт в закладки: https://zhiloy-komplex.ru/promokody-vash-nadezhnyj-sputnik-v-mire-onlajn-shopinga/

Советуем посетить сайт https://admlihoslavl.ru/promokody-sekretnyj-instrument-ekonomii-v-mire-onlajn-shopinga/

Также не забудьте добавить сайт в закладки: https://admlihoslavl.ru/promokody-sekretnyj-instrument-ekonomii-v-mire-onlajn-shopinga/

Советуем посетить сайт https://avtomaxi22.ru/

Также не забудьте добавить сайт в закладки: https://avtomaxi22.ru/

Советуем посетить сайт https://med-like.ru/

Также не забудьте добавить сайт в закладки: https://med-like.ru/

Советуем посетить сайт https://kryshi-remont.ru/

Также не забудьте добавить сайт в закладки: https://kryshi-remont.ru/

Советуем посетить сайт https://admlihoslavl.ru/

Также не забудьте добавить сайт в закладки: https://admlihoslavl.ru/

Советуем посетить сайт https://elegos.ru/

Также не забудьте добавить сайт в закладки: https://elegos.ru/

Советуем посетить сайт https://club-columb.ru/

Также не забудьте добавить сайт в закладки: https://club-columb.ru/

Советуем посетить сайт https://softnewsportal.ru/

Также не забудьте добавить сайт в закладки: https://softnewsportal.ru/

Советуем посетить сайт https://gulliverauto.ru/

Также не забудьте добавить сайт в закладки: https://gulliverauto.ru/

Советуем посетить сайт https://doutuapse.ru/

Также не забудьте добавить сайт в закладки: https://doutuapse.ru/

Советуем посетить сайт https://stroydvor89.ru/

Также не забудьте добавить сайт в закладки: https://stroydvor89.ru/

Советуем посетить сайт https://magic-magnit.ru//

Также не забудьте добавить сайт в закладки: https://magic-magnit.ru/

We recommend visiting the website https://villa-sunsetlady.com/.

Also, don’t forget to bookmark the site: https://villa-sunsetlady.com/

We recommend visiting the website https://realskinbeauty.com/.

Also, don’t forget to bookmark the site: https://realskinbeauty.com/

We recommend visiting the website https://talksoffashion.com/.

Also, don’t forget to bookmark the site: https://talksoffashion.com/

We recommend visiting the website https://skinsoulbeauty.com/.

Also, don’t forget to bookmark the site: https://skinsoulbeauty.com/

We recommend visiting the website https://powerofquotes12.blogspot.com/2024/03/the-power-of-quotes-inspiration-for.html.

Also, don’t forget to bookmark the site: https://powerofquotes12.blogspot.com/2024/03/the-power-of-quotes-inspiration-for.html

We recommend visiting the website https://quotes-status1.blogspot.com/2024/03/the-power-of-quotes-inspiration-for.html.

Also, don’t forget to bookmark the site: https://quotes-status1.blogspot.com/2024/03/the-power-of-quotes-inspiration-for.html

We recommend visiting the website https://quotablemoments1.blogspot.com/2024/03/embracing-lifes-wisdom-how-quotes-can.html.

Also, don’t forget to bookmark the site: https://quotablemoments1.blogspot.com/2024/03/embracing-lifes-wisdom-how-quotes-can.html

We recommend visiting the website https://wisdominwords123.blogspot.com/2024/03/unlocking-lifes-treasures-timeless.html.

Also, don’t forget to bookmark the site: https://wisdominwords123.blogspot.com/2024/03/unlocking-lifes-treasures-timeless.html

We recommend visiting the website https://wisdominwords123.blogspot.com/2024/03/echoes-of-wisdom.html.

Also, don’t forget to bookmark the site: https://wisdominwords123.blogspot.com/2024/03/echoes-of-wisdom.html

We recommend visiting the website https://telegra.ph/The-Radiance-of-Positivity-Exploring-the-Power-of-Positive-Quotes-03-31.

Also, don’t forget to bookmark the site: https://telegra.ph/The-Radiance-of-Positivity-Exploring-the-Power-of-Positive-Quotes-03-31

We recommend visiting the website https://telegra.ph/The-Craft-of-Achievement-Finding-Inspiration-in-Work-Quotes-03-31.

Also, don’t forget to bookmark the site: https://telegra.ph/The-Craft-of-Achievement-Finding-Inspiration-in-Work-Quotes-03-31

We recommend visiting the website https://telegra.ph/Sculpting-Success-How-Quotes-Can-Shape-Our-Aspirations-03-31.

Also, don’t forget to bookmark the site: https://telegra.ph/Sculpting-Success-How-Quotes-Can-Shape-Our-Aspirations-03-31

We recommend visiting the website https://telegra.ph/The-Bonds-We-Cherish-Celebrating-Connections-Through-Friendship-Quotes-03-31.

Also, don’t forget to bookmark the site: https://telegra.ph/The-Bonds-We-Cherish-Celebrating-Connections-Through-Friendship-Quotes-03-31

We recommend visiting the website https://telegra.ph/Lifes-Mosaic-Understanding-the-Big-Picture-Through-Quotes-03-31.

Also, don’t forget to bookmark the site: https://telegra.ph/Lifes-Mosaic-Understanding-the-Big-Picture-Through-Quotes-03-31

We recommend visiting the website https://telegra.ph/The-Drive-Within-Unlocking-Potential-with-Motivational-Quotes-03-31.

Also, don’t forget to bookmark the site: https://telegra.ph/The-Drive-Within-Unlocking-Potential-with-Motivational-Quotes-03-31

Мы рекомендуем посетить веб-сайт https://telegra.ph/Luchshie-prikormki-dlya-lovli-shchuki-v-2024-godu-03-31.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Luchshie-prikormki-dlya-lovli-shchuki-v-2024-godu-03-31

Мы рекомендуем посетить веб-сайт https://telegra.ph/Luchshie-internet-magaziny-rybolovnyh-snastej-03-31.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Luchshie-internet-magaziny-rybolovnyh-snastej-03-31

Мы рекомендуем посетить веб-сайт https://telegra.ph/Uspeh-na-konce-udochki-kak-vybrat-i-ispolzovat-kachestvennoe-rybolovnoe-oborudovanie-03-31.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Uspeh-na-konce-udochki-kak-vybrat-i-ispolzovat-kachestvennoe-rybolovnoe-oborudovanie-03-31

Мы рекомендуем посетить веб-сайт https://telegra.ph/Instrumenty-dlya-udovolstviya-pochemu-kachestvennoe-rybolovnoe-oborudovanie—zalog-uspeshnoj-i-komfortnoj-rybalki-03-31.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Instrumenty-dlya-udovolstviya-pochemu-kachestvennoe-rybolovnoe-oborudovanie—zalog-uspeshnoj-i-komfortnoj-rybalki-03-31

Мы рекомендуем посетить веб-сайт https://telegra.ph/Sekrety-uspeshnogo-ulova-znachenie-pravilnogo-vybora-i-ispolzovaniya-oborudovaniya-pri-rybalke-03-31.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Sekrety-uspeshnogo-ulova-znachenie-pravilnogo-vybora-i-ispolzovaniya-oborudovaniya-pri-rybalke-03-31

Мы рекомендуем посетить веб-сайт https://telegra.ph/Na-rybalku-s-uverennostyu-kak-vybrat-kachestvennoe-oborudovanie-dlya-uspeshnoj-rybalki-03-31.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Na-rybalku-s-uverennostyu-kak-vybrat-kachestvennoe-oborudovanie-dlya-uspeshnoj-rybalki-03-31

Мы рекомендуем посетить веб-сайт https://telegra.ph/Rybachok-vsyo-neobhodimoe-dlya-rybolova-03-31.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Rybachok-vsyo-neobhodimoe-dlya-rybolova-03-31

Мы рекомендуем посетить веб-сайт https://telegra.ph/Obzor-populyarnyh-pnevmaticheskih-pistoletov-sovety-po-vyboru-03-31.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Obzor-populyarnyh-pnevmaticheskih-pistoletov-sovety-po-vyboru-03-31

Мы рекомендуем посетить веб-сайт https://doutuapse.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://doutuapse.ru/

Мы рекомендуем посетить веб-сайт https://telegra.ph/Internet-magazin-Rybachok-Vash-provodnik-v-mire-rybolovstva-04-09-2.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Internet-magazin-Rybachok-Vash-provodnik-v-mire-rybolovstva-04-09-2

Мы рекомендуем посетить веб-сайт https://telegra.ph/Internet-magazin-Rybachok-Vash-nadezhnyj-pomoshchnik-v-mire-rybolovstva-04-09.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Internet-magazin-Rybachok-Vash-nadezhnyj-pomoshchnik-v-mire-rybolovstva-04-09

Мы рекомендуем посетить веб-сайт https://telegra.ph/Internet-magazin-Rybachok-Vash-provodnik-v-mire-rybolovstva-04-09.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Internet-magazin-Rybachok-Vash-provodnik-v-mire-rybolovstva-04-09

Мы рекомендуем посетить веб-сайт https://telegra.ph/Internet-magazin-Rybachok-Vash-nadezhnyj-pomoshchnik-v-mire-rybolovstva-04-09-2.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Internet-magazin-Rybachok-Vash-nadezhnyj-pomoshchnik-v-mire-rybolovstva-04-09-2

Мы рекомендуем посетить веб-сайт https://telegra.ph/Internet-magazin-Rybachok-Vash-vernyj-sputnik-v-mire-rybnoj-lovli-04-09.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Internet-magazin-Rybachok-Vash-vernyj-sputnik-v-mire-rybnoj-lovli-04-09

Мы рекомендуем посетить веб-сайт https://telegra.ph/Internet-magazin-Rybachok-Vash-nadezhnyj-pomoshchnik-v-mire-rybolovstva-04-09-3.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Internet-magazin-Rybachok-Vash-nadezhnyj-pomoshchnik-v-mire-rybolovstva-04-09-3

Мы рекомендуем посетить веб-сайт https://vektor-meh.ru//.

Кроме того, не забудьте добавить сайт в закладки: https://vektor-meh.ru/

Мы рекомендуем посетить веб-сайт https://stroydvor89.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://stroydvor89.ru/

Мы рекомендуем посетить веб-сайт https://magic-magnit.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://magic-magnit.ru/

Мы рекомендуем посетить веб-сайт https://kvest4x4.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://kvest4x4.ru/

Мы рекомендуем посетить веб-сайт https://photo-res.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://photo-res.ru/

Мы рекомендуем посетить веб-сайт https://great-galaxy.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://great-galaxy.ru/

Мы рекомендуем посетить веб-сайт https://kreativ-didaktika.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://kreativ-didaktika.ru/

Мы рекомендуем посетить веб-сайт https://cultureinthecity.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://cultureinthecity.ru/

Мы рекомендуем посетить веб-сайт http://vanillarp.ru/.

Кроме того, не забудьте добавить сайт в закладки: http://vanillarp.ru/

Мы рекомендуем посетить веб-сайт https://core-rpg.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://core-rpg.ru/

Мы рекомендуем посетить веб-сайт https://upsskirt.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://upsskirt.ru/

Мы рекомендуем посетить веб-сайт https://yarus-kkt.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://yarus-kkt.ru/

Мы рекомендуем посетить веб-сайт https://imgtube.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://imgtube.ru/

Мы рекомендуем посетить веб-сайт https://svetnadegda.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://svetnadegda.ru/

Мы рекомендуем посетить веб-сайт https://tione.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://tione.ru/

Мы рекомендуем посетить веб-сайт https://telegra.ph/Internet-magazin-Rybachok-vash-put-k-uspeshnoj-rybalke-04-15.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Internet-magazin-Rybachok-vash-put-k-uspeshnoj-rybalke-04-15

Мы рекомендуем посетить веб-сайт https://telegra.ph/Internet-magazin-Rybachok-vash-partner-v-mire-rybnoj-lovli-04-15.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Internet-magazin-Rybachok-vash-partner-v-mire-rybnoj-lovli-04-15

Мы рекомендуем посетить веб-сайт https://telegra.ph/Internet-magazin-Rybachok-vash-nadezhnyj-partner-v-mire-rybalki-04-15-2.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Internet-magazin-Rybachok-vash-nadezhnyj-partner-v-mire-rybalki-04-15-2

Мы рекомендуем посетить веб-сайт https://telegra.ph/O-magazine-Rybachok-04-15.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/O-magazine-Rybachok-04-15

Мы рекомендуем посетить веб-сайт https://telegra.ph/Internet-magazin-Rybachok-vash-put-k-uspeshnoj-rybalke-04-15-2.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Internet-magazin-Rybachok-vash-put-k-uspeshnoj-rybalke-04-15-2

Мы рекомендуем посетить веб-сайт https://telegra.ph/Internet-magazin-Rybachok-vash-nadezhnyj-partner-v-mire-rybnoj-lovli-04-15.

Кроме того, не забудьте добавить сайт в закладки: https://telegra.ph/Internet-magazin-Rybachok-vash-nadezhnyj-partner-v-mire-rybnoj-lovli-04-15

Мы рекомендуем посетить веб-сайт https://burger-kings.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://burger-kings.ru/

Мы рекомендуем посетить веб-сайт http://voenoboz.ru/.

Кроме того, не забудьте добавить сайт в закладки: http://voenoboz.ru/

Мы рекомендуем посетить веб-сайт https://remonttermexov.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://remonttermexov.ru/

Мы рекомендуем посетить веб-сайт https://lostfiilmtv.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://lostfiilmtv.ru/

Мы рекомендуем посетить веб-сайт https://my-caffe.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://my-caffe.ru/

Мы рекомендуем посетить веб-сайт https://adventime.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://adventime.ru/

Мы рекомендуем посетить веб-сайт https://kaizen-tmz.ru/.

Кроме того, не забудьте добавить сайт в закладки: https://kaizen-tmz.ru/

Мы рекомендуем посетить веб-сайт для ознакомления с методами налоговой оптимизации ссылка.

Не пропустите возможность узнать больше о важности налогового аудита для вашего бизнеса, добавьте в закладки нашу страницу: ссылка

Мы рекомендуем посетить веб-сайт для ознакомления с методами налоговой оптимизации ссылка.