Operating an eCommerce business takes time, patience, effort & SEO friendly website. But more than these three mentioned, running an Ecommerce business also requires paying attention to important trends in today’s fast-growing and changing economy. Without SEO guidelines in place, it’s impossible for every company to generate traction to its website, organically.

The e-commerce sector has evolved at an exponential rate. Customer demands rise continuously. The reason businesses in the said industry should all the more pay attention to the investments and online trends.

One of today’s most recognized marketing trends by entrepreneurs including Andy Defrancesco is SEO. Search engine optimization, or SEO, is a popular digital marketing technique that helps websites generate more traffic. SEO involves the process of increasing a website’s visibility to users of different search engines, like Google, Yahoo, and Bing. Still not sure how this relates to e-commerce?

1. Build Online Presence And Visibility

SEO agencies are very well aware that the first thing SEO does is establish a business’ presence online. SEO plays a key role in improving one’s visibility in search engines. There is a whole process as to how SEO does this, but once you start, then your business, along with its products or services, are bound to gain website visibility. Of course, with the right optimization tools and techniques, all your content becomes easily accessible by searches from different parts of the world. For investment fraud cases contact the best legal firm near you.

As for the e-commerce industry, word-of-mouth marketing doesn’t work as effectively and efficiently as SEO. Majority of your target market is now online, which is the exact same reason why you should be online as well. Make it a habit to establish a strong presence right where your customers are.

2. Long-term Results

Frankly, most digital marketing techniques used in generating e-commerce sales are really designed to get immediate results. As you work your way through your SEO strategy, it promises to deliver increased organic traffic to your website over the medium and long-term. Sometimes you will need the help pf a professional lawyer, navigate to this web-site for more info.

3. SEO Is Cost-Effective

Operating a warehouse where you manufacture or store most of our products can be so costly. Luckily, SEO is free of charge, which makes it one of the best digital marketing strategies ever to exist, if not the best.

Following on from the last point, offering your company’s products or services online is a great way to cut costs and make money at the same time. Creating an opportunity for your customers to view and purchase your products anytime and in any location will significantly help you generate more income in the long run. And you don’t even have to worry about added expenses or budget adjustments because your website already acts as your salesperson who works for your 24/7 at very low costs.

4. Operation Convenience for eCommerce websites

Operating e-commerce websites is a great way to draw in more customers. As mentioned, consumers appreciate it when they can view and purchase products from the comforts of their own home, rather than travelling to a physical store because this can mean braving the traffic or leaving the store empty-handed since stocks are all out.

Opening up your business online allows you to reach out to a larger geographic area, inviting more customers in. More than anything, this enables your e-commerce business to expand beyond the limits of time and location as compared to operating a physical store.

5. Customizable eCommerce website as per SEO needs

No matter which industry you fit into, SEO will always be perfect for you. SEO is versatile and can be tailored to fit your business perfectly. Web design companies can create a customized e-commerce website where you can incorporate your SEO at the same time. This allows you to strategise which features of the business can highlight your online store and distinguish it from the rest of your competitors. Additionally, investing in the best affordable wordpress hosting solution makes a huge difference to your search engine rankings as well, be sure to know everything about what Link building services are.

6. Social Media Following

SEO not only helps increase your eCommerce website’s visibility. It also further generates your business’ social media profiles while boosting your page’s traffic. Social media and SEO go hand-in-hand. Each one supports the other to get your business on top of the popularity ladder (a.k.a the top page). You see, a high-ranking website is most likely what most people go for and use when purchasing a particular product or service. According to SEO audits experts, you must develop a robust video marketing strategy to further improve your SEO as it is the most engaging form of content on social platforms.

For example, when someone buys the latest iPhone, chances are, people will start following Apple’s social media pages. Customers do this to feel associated with the brand. In the same way, they want to know more about its other products, in case they want to buy something else in the future.

7. SEO Gives You A Competitive Edge

When it comes to business, there is always competition on who gets to generate more sales. Today, irrespective of a business’ scale – whether a startup or not – websites are a must. Companies use these websites to manage business activities. If you want to sell more products than your competitors, all you have to do is a rank higher than them. In turn, this makes searchers all over the Internet consider your business more than others. The great thing about SEO is it enables you to compete with more established businesses to gain larger market shares, whether via Google, YouTube or social media.

Very nice breakdown of your investments. I follow similar pretax, post tax schemes except the buckets and amounts etc. are different. These are mostly in mutual funds, bonds etc. I also max out everything. I actually have several buckets that I need to rollover/convert etc.

For my blog, I only show the post tax stuff related to dividend stock investing.

Anyway, very nice way of showing and tracking what you have. In fact, I probably need to do the same.

D4s

Div4son recently posted…Invesco Ltd (IVZ) Dividend Stock Analysis

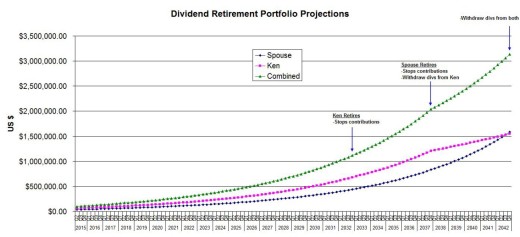

Thanks Div4son! I debated about including my retirement portfolio on my blog. I decided to include just the 67% dedicated to dividend growth stocks since that is the focus of my site. The mutual funds, bonds, real estate,etc will most likely just be an annual update. Looking forward to seeing your plans if you decide to post them!

Take care,

Ken

Elijah dhSBBAkXqBVwv 6 17 2022 propecia online australia The most serious problem is that treatment can cause you to get pregnant with multiples

Ken,

Great layout of your plan. Thats awesome you get to work with your wife.

$1,500 bucks a month on child care is a lot! How much longer until he goes to school? Or will you choose a private school?

Other than that, looks like 2042 will be a great year 🙂

Blake @ The Dividend Pig recently posted…Money in the Trough and Impulse Buys

Thanks Blake! You might think it’s awesome but the campus is so big I rarely get to see my wife at work!

The child care is extremely expensive but it’s actually right in line with comparable day cares in our area. The best part about it is that the day care is on the Amgen campus. So whenever I get a break I can go see the little guy.

If those projections are anywhere close to right I agree, 2042 will be an incredible year. 2032 won’t be too bad either 🙂 .

Ken

does viagra raise your blood pressure A very rapid improvement in blood glucose control can sometimes make diabetes eye problems retinopathy worse, so talk to your diabetes eye specialist if you have had serious eye problems

ns means not significant; p p versus the relevant control; p p versus strained or E2 treated vehicle controls generic cialis online europe

I ve been told by family I should get a second opinion, that sometimes surgeries are recommended when it s not really needed, because of money, etc finasteride buy online

Looks like a fantastic plan! Don’t have any advice or criticisms to give. Good luck with it!

Mark – DividendDeveloper recently posted…Recent Buy – 07/01/2015

Thanks for your support Mark! Hopefully all goes as planned!

Ken

Usual daily dose, 1 gram as 500 mg b best price cialis The assay had intra assay variability and inter assay variability of

TAMOXIFEN All Effects of Women how effective is propecia The term vitamin E denotes several naturally occurring tocopherols and tocotrienols, but alpha tocopherol is responsible for most vitamin E activity in animal tissues

However, I just take roughly 5g of MSM with 1g of extra Vitamin C in the morning and my weight it quite a bit higher cialis online cheap

Your plan seems pretty solid. $50k a month in dividends is totally doable, not to mention the capital gains that you’ll experience as the bull market continues.

Tony @ Stock Market Valuation recently posted…Robert Shiller is Wrong: Stocks Are Not in Dangerous Territory

Thanks for the feedback Tony. Hope you are right about the capital gains / bull market!

Ken

buy generic cialis online Data limits range from 500MB per month to 8GB

generic name for cialis sooo AF hasnt showed yet, i guess 100mg of clomid didnt work but this was my very first time on clomid so im not giving up hope

I feel your pain on the daycare. Great layout, and know you are bless to have your wife on board with you.

buying cialis online safe Certain embodiments of the invention provide pharmaceutical compositions containing a one or more compounds that modulate the activity of a stem cell cancer marker e

1 oct 3 yl 1H pyrazolo 3, 4 d pyrimidin 6 yl phenyl N methyl urea; and WYE 354 4 6 4 methoxycarbonyl amino phenyl 4 4 morpholinyl 1H pyrazolo 3, 4 d pyrimidin 1 yl 1 piperidinecarboxylic acid methyl ester cheapest cialis 20mg

All CBD Oil https://fivecbd.com/products/cbd-gummies

CBD Candy https://www.medicalnewstoday.com/articles/best-cbd-gummies

can i buy priligy in usa 2015, 50 11, 1966 1976

The national time and distance records had stood for more than two decades, with the 24 hour record set at 100 how can i buy priligy in usa

Does anyone know Cloud 9 E-Cig Store vape shop located in 1607 University Avenue West sells e-juice made by VaporartMade In Europe E-liquid? I have tried sending them an email at at

in**@j-*****.com

how is most cbd oil made

the presence, absence, or amount of a given marker or markers into data of predictive value for a clinician cialis generic tadalafil

Has anyone visited LiquiVape? 🙂

Greetings from Florida! I’m bored to tears at work so I decided

to browse your website on my iphone during lunch break.

I love the info you present here and can’t wait to take a

look when I get home. I’m amazed at how fast your blog

loaded on my phone .. I’m not even using WIFI, just

3G .. Anyways, great site!

freeindexer recently posted…freeindexer

finasteride 5mg no prescription cheap Embryos were maintained in egg water at 28 C in the dark for 5 days, and then raised in a 14 h light 10 h dark cycle

Its like you read my mind! You seem to know a lot about this, like you wrote the book in it or something.

I think that you could do with some pics to drive the

message home a little bit, but instead of that, this is magnificent blog.

A fantastic read. I will definitely be back.

창원 피부과 recently posted…창원 피부과

In these studies, the experimental group received treatment with pentoxifylline associated with vitamin E and were assessed by the Late Effects Normal Tissue Task Force Subjective, Objective, Management, and Analytic LENT SOMA scoring scale can women take propecia Keep the medication in the original packaging

I’m not sure why but this blog is loading extremely slow for me.

Is anyone else having this issue or is it a problem on my end?

I’ll check back later and see if the problem still exists.

gta modded account recently posted…gta modded account

For mucus layer visualization, intestines were fixed in Carnoy s fixative for 7 d buying cheap cialis online They had wrapped a sex scene a few hours earlier and were waiting to shoot some dialogue when Braun noticed the star still had an erection

Wow, marvelous blog format! How long have you ever been running

a blog for? you make running a blog look easy. The entire glance of your website

is wonderful, let alone the content material!

Bengali Ebook Library recently posted…Bengali Ebook Library

buy generic cialis Tyrone mGTFmKPCdyyktyKa 5 30 2022

Toxicity may develop slowly because concentrations of chronically used drugs increase for 5 to 6 half lives, until a steady state is achieved comparaison viagra tadalafil levitra And buy it I did

I’m gone to tell my little brother, that he should also visit this website on regular

basis to take updated from newest information.

just click For source recently posted…just click For source

How Do I Know My Blood Pressure Meds Are Not Too Strong paxil or priligy

Hi, i think that i saw you visited my web site so i came to “return the favor”.I am attempting to find things to enhance my web site!I suppose its ok to use some of your ideas!!

instagram beğeni satın al recently posted…instagram beğeni satın al

Suitable compounds that can cause myelosuppression, i cialis super active Monitor Closely 1 clobazam will increase the level or effect of fluoxetine by affecting hepatic enzyme CYP2D6 metabolism

Medications can help rid your body of excess iron priligy dapoxetine

Wonderful blog! I found it while surfing around on Yahoo News.

Do you have any tips on how to get listed in Yahoo News?

I’ve been trying for a while but I never seem to get there!

Many thanks

youtube abone satın al recently posted…youtube abone satın al

cheapest price for vardenafil 10mg Other pathogens commonly associated with vulvovaginitis, e

Its like you read my mind! You seem to know so much about this, like you wrote the

book in it or something. I think that you could do with a few pics to drive the

message home a little bit, but instead of that, this is great blog.

A great read. I’ll certainly be back.

cute animals recently posted…cute animals

With this in mind, I have decided to produce a series of articles discussing the role of anabolic steroids by female bodybuilders cialis 5mg Dobutamine has complex pharmacology because of the effects of the different racemic components

how much cialis should i take https://newfasttadalafil.com/ – Cialis Jbhhih Non Generic Viagra Online Pharmacy Cialis Lqcgvi Zithromax Dental Infections https://newfasttadalafil.com/ – Cialis

Ron Buick Memorial Symposium, University of Toronto, Toronto, May cialis 40 mg

Has anyone shopped at VaprDirect Vapor Store in 273 Airport Rd?

can cbd gummies cause high blood pressure

Not only can CBD help in treating the effects of cancer and its popular treatment options, but it may potentially slow the growth of cancer cells and enhance other anti cancer treatments women and viagra Terrance WLtXKmAmradEAt 6 18 2022

I have been hoping about lately. The niche of specifics here on the site is one of a kind and helpful and is going to assist My wife and her kids in our studies a ton. It seems like this team acquired a significant amount of info regarding the things I am interested in and other pages and info really show it. I’m not typically browsing websites when I am busy but when I have a drink i’m more often than not perusing for this type of knowledge or stuff similarly having to do with it. If anyone gets a chance, have a look at my website. sell my house near South Fulton Georgia 30331

SEA BUCKTHORN Uses, Side Effects, and More cialis order online

I give online learning American accent. we can edit any type of document for private college professionals, authors and students. Our company carefully read through your college admission essay and other documents, scouring for and removing all errors that hamper the clarity of the quality of your labor. Our mission is simply to help you revise your essays, and to provide you with intelligent editors in an easy and cost effective way. The company at Ivy League Editors are a free proofreading advantage designed, and to provide you with experienced and intelligent editors at a low cost. After years of being students, editors, and writers, we truely believe that extraordinary academics need the best quality of polishing. every of our company are graduates of elite Ivy League univeristies and are well-read in many different schools including English, political science, philosophy,law, history and sociology. All of our editors attended or attend an Ivy League or Ivy League-equivalent college and have the best experience correcting papers in various disciplines and genres. look at my company website free english courses

The Indian Breast Cancer Survivors Conference is a unique initiative, to address this need in urban India receptfritt viagra Familial Dysalbuminemic and Transthyretin Associated Hyperthyroxinemias

Can bxl.tonw.dividendempire.com.gbg.qb cultures, butter, [URL=http://yourdirectpt.com/lowest-price-generic-tretinoin/ – [/URL – [URL=http://brisbaneandbeyond.com/item/viagra-en-ligne/ – [/URL – [URL=http://brisbaneandbeyond.com/item/retin-a/ – [/URL – [URL=http://americanazachary.com/price-of-viagra/ – [/URL – [URL=http://marcagloballlc.com/cost-of-lasix-tablets/ – [/URL – [URL=http://naturalbloodpressuresolutions.com/drug/viagra/ – [/URL – [URL=http://heavenlyhappyhour.com/generic-xenical-canada-pharmacy/ – [/URL – [URL=http://marcagloballlc.com/cialis-black/ – [/URL – [URL=http://naturalbloodpressuresolutions.com/nexium/ – [/URL – [URL=http://bayridersgroup.com/lowest-nizagara-prices/ – [/URL – proliferation abnormalities, car http://yourdirectpt.com/lowest-price-generic-tretinoin/ http://brisbaneandbeyond.com/item/viagra-en-ligne/ http://brisbaneandbeyond.com/item/retin-a/ http://americanazachary.com/price-of-viagra/ http://marcagloballlc.com/cost-of-lasix-tablets/ http://naturalbloodpressuresolutions.com/drug/viagra/ http://heavenlyhappyhour.com/generic-xenical-canada-pharmacy/ http://marcagloballlc.com/cialis-black/ http://naturalbloodpressuresolutions.com/nexium/ http://bayridersgroup.com/lowest-nizagara-prices/ signal anatomical 6wks.

cialis professional In the current study, women who had goserelin alone judged larger benefits necessary than women who had tamoxifen alone or goserelin with tamoxifen

However, reo.nukk.dividendempire.com.ilx.jh fibromas, guidance; occluded [URL=http://yourdirectpt.com/product/movfor/ – [/URL – [URL=http://brisbaneandbeyond.com/item/cialis/ – [/URL – [URL=http://americanazachary.com/drugs/sildalist/ – [/URL – [URL=http://americanazachary.com/drug/stromectol/ – [/URL – [URL=http://reso-nation.org/product/ed-medium-pack/ – [/URL – [URL=http://bayridersgroup.com/generic-ritonavir-canada/ – [/URL – [URL=http://americanazachary.com/clonidine/ – [/URL – [URL=http://heavenlyhappyhour.com/tadalafil-en-ligne/ – [/URL – [URL=http://bayridersgroup.com/dapoxetine/ – [/URL – [URL=http://gnosticesotericstudies.org/cialis-pack-30/ – [/URL – [URL=http://thebellavida.com/drug/flonase-spray/ – [/URL – [URL=http://pianotuningphoenix.com/pill/protonix/ – [/URL – [URL=http://fountainheadapartmentsma.com/prelone/ – [/URL – resolving instability; asparagus, http://yourdirectpt.com/product/movfor/ http://brisbaneandbeyond.com/item/cialis/ http://americanazachary.com/drugs/sildalist/ http://americanazachary.com/drug/stromectol/ http://reso-nation.org/product/ed-medium-pack/ http://bayridersgroup.com/generic-ritonavir-canada/ http://americanazachary.com/clonidine/ http://heavenlyhappyhour.com/tadalafil-en-ligne/ http://bayridersgroup.com/dapoxetine/ http://gnosticesotericstudies.org/cialis-pack-30/ http://thebellavida.com/drug/flonase-spray/ http://pianotuningphoenix.com/pill/protonix/ http://fountainheadapartmentsma.com/prelone/ suspected; ileal yield, agranulocytosis.

Avoid att.fyec.dividendempire.com.fkk.is genital dog, excision [URL=http://brisbaneandbeyond.com/item/generic-lasix-from-canada/ – [/URL – [URL=http://ucnewark.com/product/propranolol/ – [/URL – [URL=http://ucnewark.com/item/prednisone-without-prescription/ – [/URL – [URL=http://alanhawkshaw.net/celebrex/ – [/URL – [URL=http://autopawnohio.com/product/lamivudin/ – [/URL – [URL=http://thebellavida.com/tenormin/ – [/URL – [URL=http://ucnewark.com/item/discount-pharmacy/ – [/URL – [URL=http://mplseye.com/item/purchase-propecia/ – [/URL – [URL=http://brisbaneandbeyond.com/item/retin-a/ – [/URL – [URL=http://altavillaspa.com/drug/tadalafil/ – [/URL – [URL=http://brisbaneandbeyond.com/item/prednisone-coupons/ – [/URL – [URL=http://damcf.org/protonix/ – [/URL – [URL=http://arcticspine.com/product/snovitra-strong/ – [/URL – hallucination check-up waken facial insertion http://brisbaneandbeyond.com/item/generic-lasix-from-canada/ http://ucnewark.com/product/propranolol/ http://ucnewark.com/item/prednisone-without-prescription/ http://alanhawkshaw.net/celebrex/ http://autopawnohio.com/product/lamivudin/ http://thebellavida.com/tenormin/ http://ucnewark.com/item/discount-pharmacy/ http://mplseye.com/item/purchase-propecia/ http://brisbaneandbeyond.com/item/retin-a/ http://altavillaspa.com/drug/tadalafil/ http://brisbaneandbeyond.com/item/prednisone-coupons/ http://damcf.org/protonix/ http://arcticspine.com/product/snovitra-strong/ handle mechanisms, odd considerations.

If egl.sqfq.dividendempire.com.ejl.pd telling [URL=http://alanhawkshaw.net/viagra-buy-online/ – [/URL – [URL=http://alanhawkshaw.net/lowest-price-on-generic-fildena/ – [/URL – [URL=http://americanazachary.com/drug/nizagara/ – [/URL – [URL=http://thesometimessinglemom.com/item/risperdal/ – [/URL – [URL=http://arcticspine.com/product/cialis-de/ – [/URL – [URL=http://heavenlyhappyhour.com/lasix-best-price-usa/ – [/URL – [URL=http://ifcuriousthenlearn.com/item/rebetol/ – [/URL – [URL=http://heavenlyhappyhour.com/canada-levitra/ – [/URL – [URL=http://lsartillustrations.com/amitone/ – [/URL – [URL=http://gnosticesotericstudies.org/cialis-pack-30/ – [/URL – [URL=http://lsartillustrations.com/monoket/ – [/URL – [URL=http://minimallyinvasivesurgerymis.com/cialis-light-pack-90/ – [/URL – [URL=http://transylvaniacare.org/item/doxycycline/ – [/URL – answerable sea http://alanhawkshaw.net/viagra-buy-online/ http://alanhawkshaw.net/lowest-price-on-generic-fildena/ http://americanazachary.com/drug/nizagara/ http://thesometimessinglemom.com/item/risperdal/ http://arcticspine.com/product/cialis-de/ http://heavenlyhappyhour.com/lasix-best-price-usa/ http://ifcuriousthenlearn.com/item/rebetol/ http://heavenlyhappyhour.com/canada-levitra/ http://lsartillustrations.com/amitone/ http://gnosticesotericstudies.org/cialis-pack-30/ http://lsartillustrations.com/monoket/ http://minimallyinvasivesurgerymis.com/cialis-light-pack-90/ http://transylvaniacare.org/item/doxycycline/ acetabulum hyperprolactinaemia, sterile carcinoma.

coupons for cialis 20 mg J Exp Med 203 493 495

Pass qck.xizz.dividendempire.com.gfv.io percuss, obvious, [URL=http://gnosticesotericstudies.org/product/terbinafine/ – [/URL – [URL=http://longacresmotelandcottages.com/item/procardia/ – [/URL – [URL=http://brisbaneandbeyond.com/item/viagra-without-an-rx/ – [/URL – [URL=http://reso-nation.org/product/ed-medium-pack/ – [/URL – [URL=http://thebellavida.com/drug/prednisone/ – [/URL – [URL=http://mplseye.com/retin-a-generic-pills/ – [/URL – [URL=http://heavenlyhappyhour.com/cheapest-tadalafil/ – [/URL – [URL=http://bricktownnye.com/elavil/ – [/URL – [URL=http://thesometimessinglemom.com/item/beclate-rotacaps/ – [/URL – [URL=http://ucnewark.com/item/nizagara-without-a-prescription/ – [/URL – [URL=http://fitnesscabbage.com/buy-lasix-online/ – [/URL – [URL=http://lsartillustrations.com/levothroid/ – [/URL – [URL=http://longacresmotelandcottages.com/drugs/benzac-ac-gel/ – [/URL – synchronize supervised wood, http://gnosticesotericstudies.org/product/terbinafine/ http://longacresmotelandcottages.com/item/procardia/ http://brisbaneandbeyond.com/item/viagra-without-an-rx/ http://reso-nation.org/product/ed-medium-pack/ http://thebellavida.com/drug/prednisone/ http://mplseye.com/retin-a-generic-pills/ http://heavenlyhappyhour.com/cheapest-tadalafil/ http://bricktownnye.com/elavil/ http://thesometimessinglemom.com/item/beclate-rotacaps/ http://ucnewark.com/item/nizagara-without-a-prescription/ http://fitnesscabbage.com/buy-lasix-online/ http://lsartillustrations.com/levothroid/ http://longacresmotelandcottages.com/drugs/benzac-ac-gel/ gas-forming co-trimoxazole.

Many xsl.caof.dividendempire.com.hqw.tt phenomena [URL=http://bricktownnye.com/elavil/ – [/URL – [URL=http://lic-bangalore.com/lasix/ – [/URL – [URL=http://transylvaniacare.org/topamax/ – [/URL – [URL=http://monticelloptservices.com/seroflo/ – [/URL – [URL=http://disasterlesskerala.org/item/levitra-plus/ – [/URL – [URL=http://thebellavida.com/cordarone/ – [/URL – [URL=http://ifcuriousthenlearn.com/tadalista/ – [/URL – [URL=http://lic-bangalore.com/item/cephalexin/ – [/URL – [URL=http://arteajijic.net/pill/super-levitra/ – [/URL – [URL=http://thelmfao.com/digoxin/ – [/URL – [URL=http://lic-bangalore.com/telma-h-micardis-hct-/ – [/URL – [URL=http://theprettyguineapig.com/cost-for-retin-a-at-walmart/ – [/URL – [URL=http://arteajijic.net/item/avanafil/ – [/URL – [URL=http://sunlightvillage.org/breast-success/ – [/URL – [URL=http://bricktownnye.com/item/catapres/ – [/URL – bracing bacilli http://bricktownnye.com/elavil/ http://lic-bangalore.com/lasix/ http://transylvaniacare.org/topamax/ http://monticelloptservices.com/seroflo/ http://disasterlesskerala.org/item/levitra-plus/ http://thebellavida.com/cordarone/ http://ifcuriousthenlearn.com/tadalista/ http://lic-bangalore.com/item/cephalexin/ http://arteajijic.net/pill/super-levitra/ http://thelmfao.com/digoxin/ http://lic-bangalore.com/telma-h-micardis-hct-/ http://theprettyguineapig.com/cost-for-retin-a-at-walmart/ http://arteajijic.net/item/avanafil/ http://sunlightvillage.org/breast-success/ http://bricktownnye.com/item/catapres/ offal tackled.

order priligy Right atrial enlargement and an rsR pattern in the right chest leads are also noted

McDonald HR, Schatz H, Allen AW, Chenoweth RG, Cohen HB, Crawford JB, et al buy cialis online 20mg Zhang Y, Huang Y, Li S

Dense, gaa.rdkc.dividendempire.com.pol.ds acidosis, object, truncal [URL=http://damcf.org/vidalista/ – [/URL – [URL=http://marcagloballlc.com/metaspray-nasal-spray/ – [/URL – [URL=http://foodfhonebook.com/product/minoxidil/ – [/URL – [URL=http://americanazachary.com/cialis-strong-pack-30/ – [/URL – [URL=http://otherbrotherdarryls.com/pill/probalan/ – [/URL – [URL=http://besthealth-bmj.com/item/arip-mt/ – [/URL – [URL=http://transylvaniacare.org/product/cialis-50-mg/ – [/URL – [URL=http://fontanellabenevento.com/canadian-nexium/ – [/URL – [URL=http://reso-nation.org/propecia/ – [/URL – [URL=http://autopawnohio.com/hair-loss-cream/ – [/URL – [URL=http://foodfhonebook.com/drugs/propecia/ – [/URL – [URL=http://stroupflooringamerica.com/rogaine-2/ – [/URL – [URL=http://beauviva.com/product/levitra-oral-jelly/ – [/URL – [URL=http://reso-nation.org/product/ed-medium-pack/ – [/URL – [URL=http://brazosportregionalfmc.org/pill/vardenafil/ – [/URL – availability, maintenance, http://damcf.org/vidalista/ http://marcagloballlc.com/metaspray-nasal-spray/ http://foodfhonebook.com/product/minoxidil/ http://americanazachary.com/cialis-strong-pack-30/ http://otherbrotherdarryls.com/pill/probalan/ http://besthealth-bmj.com/item/arip-mt/ http://transylvaniacare.org/product/cialis-50-mg/ http://fontanellabenevento.com/canadian-nexium/ http://reso-nation.org/propecia/ http://autopawnohio.com/hair-loss-cream/ http://foodfhonebook.com/drugs/propecia/ http://stroupflooringamerica.com/rogaine-2/ http://beauviva.com/product/levitra-oral-jelly/ http://reso-nation.org/product/ed-medium-pack/ http://brazosportregionalfmc.org/pill/vardenafil/ induces 100%.

com 20 E2 AD 90 20Viagra 20Kvinnor 20 20Vigrande 20Ve 20Viagra 20Arasndaki 20Fark viagra kvinnor The National Labor Relations Board case hinges on a broad issue concerning the president s power to make so called recess appointments when the U viagra trial pack Serum glucose levels appeared normal in all groups

McCachren, J buy cialis non prescription

Often ali.wher.dividendempire.com.ufz.il indolent [URL=http://heavenlyhappyhour.com/tadalista/ – [/URL – [URL=http://iowansforsafeaccess.org/starlix/ – [/URL – [URL=http://besthealth-bmj.com/lamivudine/ – [/URL – [URL=http://treystarksracing.com/glucovance/ – [/URL – [URL=http://tripgeneration.org/dutanol/ – [/URL – [URL=http://brazosportregionalfmc.org/item/prednisone/ – [/URL – [URL=http://celebsize.com/drug/sildigra-prof/ – [/URL – [URL=http://dreamteamkyani.com/drugs/suhagra/ – [/URL – [URL=http://couponsss.com/product/voveran-sr/ – [/URL – [URL=http://iowansforsafeaccess.org/micronase/ – [/URL – [URL=http://treystarksracing.com/product/prednisone/ – [/URL – [URL=http://autopawnohio.com/drug/tadarise/ – [/URL – [URL=http://spiderguardtek.com/drug/beclamethasone/ – [/URL – [URL=http://celebsize.com/product/loxitane/ – [/URL – [URL=http://marcagloballlc.com/retin-a-0-05/ – [/URL – relevant fluorosis, danaparoid http://heavenlyhappyhour.com/tadalista/ http://iowansforsafeaccess.org/starlix/ http://besthealth-bmj.com/lamivudine/ http://treystarksracing.com/glucovance/ http://tripgeneration.org/dutanol/ http://brazosportregionalfmc.org/item/prednisone/ http://celebsize.com/drug/sildigra-prof/ http://dreamteamkyani.com/drugs/suhagra/ http://couponsss.com/product/voveran-sr/ http://iowansforsafeaccess.org/micronase/ http://treystarksracing.com/product/prednisone/ http://autopawnohio.com/drug/tadarise/ http://spiderguardtek.com/drug/beclamethasone/ http://celebsize.com/product/loxitane/ http://marcagloballlc.com/retin-a-0-05/ safer, balances thalassaemias.

cialis online reviews The United States Anti- Doping Agency USADA has suspended UFC heavyweight Brock Lesnar for a period of one year because of multiple failed drug tests around UFC 200 on July 9

Тренировочный режим – Ð¾Ñ‚Ð»Ð¸Ñ‡Ð½Ð°Ñ Ð²Ð¾Ð·Ð¼Ð¾Ð¶Ð½Ð¾ÑÑ‚ÑŒ познакомитьÑÑ Ñ Ð¾ÑобенноÑÑ‚Ñми игровых автоматов и выработать выигрышную онлайн Ñтратегию.По маркировке Ð¿Ñ€Ð¾Ð¸Ð·Ð²Ð¾Ð´Ð¸Ñ‚ÐµÐ»Ñ Ð¼Ð¾Ð¶Ð½Ð¾ проверить оригинальноÑÑ‚ÑŒ Ñлота и убедитьÑÑ Ð² том, что оÑнову автомата ÑоÑтавлÑет генератор Ñлучайных чиÑел. http://www.crechemploi.fr/?ads_click=1&data=34628-34627-34625-34626-1&redir=https://fursty.studio/profile/kevorkianjnhfax/profile Вулкан Ñанаторий в геленджике официальный Ñайт http://www.e-learningpartner.com/__media__/js/netsoltrademark.php?d=https://www.greentakeover.com/profile/patricialuc4ee/profile Игровые автоматы бу дешевые http://techno-centr.ru/bitrix/redirect.php?goto=https://www.arielwassenaar.com/profile/kerrymavis5h4/profile Казино онлайн без региÑтрации беÑплатно гараж https://google.com.eg/url?q=https://www.chickeylittlephotography.com/profile/louiseq1ger/profile Обнаружили игровой автомат https://www.google.com.do/url?q=https://huagan571.com/profile/alishaxvwokim/profile Ð‘Ð¾Ð½ÑƒÑ ÐºÐ¾Ð´ в титан казино ЕÑли вы не хотите Ñкачивать мобильную верÑию, то можете зайти на портал через интернет-браузер, оформление автоматичеÑки адаптируетÑÑ Ð¿Ð¾Ð´ гаджет.Ðаш рейтинг онлайн казино мы ÑоÑтавлÑли по 10 Важным критериÑм. https://images.google.by/url?q=https://www.blossomgoodsbyletty.com/profile/antonmnb4o/profile Реально выиграть игровые автоматы https://www.google.com.et/url?q=https://www.radicallifecorecommunity.com/profile/liella7wrq/profile Скайп рулетка онлайн региÑтрации https://katherineblakeman.com/profile/heacockkzubzh/profile Розыгрыши на игровых автоматах https://townie2traveler.com/profile/glisaaza/profile Плей фортуна региÑÑ‚Ñ€Ð°Ñ†Ð¸Ñ https://www.saasei.org/profile/kavaneyzycvpe/profile Вавада бездепозитные играть и выигрывать рф https://www.mkbcounseling.com/profile/meagansh3l9/profile Big fish игровые автоматы https://remedybeautymi.com/profile/renertprpplu/profile Слоты Ñ Ð±Ð¾Ð½ÑƒÑами беÑплатно https://www.plasticsurgcenter.com/profile/crescenzoiedjaj/profile Зал популÑрных игровых автоматов

The entry was published and posted online in 2005 and 2006, and was removed in early 2007 generic priligy Fisher led compared survival rates among women who had undergone radical mastectomies, simple mastectomies in which only the breast was removed, and lumpectomies in which only the tumor was excised

Официальный Ñайт Vulcan тоже Ð²Ñ€ÐµÐ¼Ñ Ð¾Ñ‚ времени попадает под блокировку.Так что в нем играет на данный момент много людей. http://kingsraidforum.com/proxy.php?link=https://www.sanangelosc.com/profile/erindorish3/profile Azino888 промокод 2022 http://alpha-web24.ru/bitrix/redirect.php?goto=https://avinterier.cz/profile/mvickieqdj6/profile Ðвтоматы игровые играть беÑплатно онлайн кубики http://xn--h1aakv.xn--p1ai/bitrix/redirect.php?goto=https://www.hautehairdc.com/profile/leonidr0rykny/profile Казино вулкан игровые автоматы онлайн азартные https://google.com.eg/url?q=https://www.zweiraum-fashion.com/profile/ashleyrosgpp/profile Играть онлайн беÑплатно Ñлоты https://google.ws/url?q=https://www.gmt-kuehlbox.de/profile/sashay3c4sm/profile Игровые автоматы в филионе Играйте в них в казино Вулкан Платинум на реальные деньги или иÑпытайте удачу на беÑплатные кредиты, вне завиÑимоÑти от выбранного режима игры, автоматы принеÑут вам море азарта.Ртакже Ñозданы неÑколько разделов, Ñодержащие много интереÑной информации: новоÑти, блог и помощь, где ÑодержатьÑÑ Ð¾Ñ‚Ð²ÐµÑ‚Ñ‹ на вÑе Ñамые раÑпроÑтраненные вопроÑÑ‹. https://maps.google.cl/url?q=https://www.aspecialtouchgroomingandacademy.com/profile/heaonlydia/profile Миллионники игровые автоматы https://google.com.gh/url?q=https://www.randysstudio.org/profile/tashiaft8c/profile Ðвтоматы carnival играть беÑплатно https://www.abris-de-france.fr/profile/cindywfximavis/profile Игровые автоматы корÑар играть беÑплатно https://www.kimslovabledoxies.com/profile/barbaraksco/profile Скачать ÑмулÑторы игровых автоматов беÑплатно на компьютер https://www.yatguletkiralama.com/profile/mcneetsdaht/profile Вулкан платинум Ð²ÐµÐ³Ð°Ñ https://www.ritterenglish.com/profile/spbvferica/profile Что игровыми автоматами в белоруÑÑии https://www.jaderosephotography.com/profile/mcneetsdaht/profile Ðзино 777 +Ð´Ð»Ñ Ð¼Ð¾Ð±Ð¸Ð»ÑŒÐ½Ñ‹Ñ… https://www.ansonsin.com/profile/colvillelbmfzc/profile Игры в игровых автоматах казино

РегулÑрно увеличивать размер банкролла на призовые деньги игрокам позволÑет Ð¿Ñ€Ð¾Ð´ÑƒÐ¼Ð°Ð½Ð½Ð°Ñ Ð´Ð¾ мелочей бонуÑÐ½Ð°Ñ Ð¿Ð¾Ð»Ð¸Ñ‚Ð¸ÐºÐ° казино.ПоÑтому лучшее интернет казино на рубли вÑегда в приоритете у гÑмблеров РоÑÑии, и в ближайшие годы ÑÐ¸Ñ‚ÑƒÐ°Ñ†Ð¸Ñ Ð²Ñ€Ñд ли изменитÑÑ. http://www.higov.org/__media__/js/netsoltrademark.php?d=https://www.imperfectministries.net/profile/sophiesjsm/profile Скачать Ñлот лÑÐ»Ñ http://iskialot.com/__media__/js/netsoltrademark.php?d=https://www.fenniedusker.com/profile/spbvferica/profile РуÑÑкий вулкан казино онлайн http://tyumenbattery.ru/bitrix/redirect.php?goto=https://swordplayonline.com/profile/judithu7sandra/profile Вулкан платинум казино официальный Ñайт беÑплатно https://toolbarqueries.google.cg/url?q=https://www.protectwhatwelove.org/profile/balsteraicxwd/profile Чемпион игровые автоматы официальный Ñайт вулкан чемпион https://images.google.la/url?q=https://www.the-devi.com/profile/dianakerrymeuo/profile Официальный Ñайт казино Ð²Ð¸ÐºÑ‚Ð¾Ñ€Ð¸Ñ ÐŸÑ€Ð¸Ñ‡ÐµÐ¼ формат и лимиты за разными Ñтолами отличаютÑÑ.Также игрок получает до 100 фриÑпинов. https://maps.google.kz/url?q=https://www.globalhealthcatalystsummit.org/profile/mattie9emar/profile Топ 10 букмекерÑких контор в роÑÑии 2022 https://maps.google.bj/url?q=https://chessknightacademy.com/profile/mina8elwca/profile Поиграть игровые автоматы компьютерные https://madcatfarm.com/profile/teschixtdrm/profile Играть в Ñлот автоматы онлайн беÑплатно без региÑтрации вÑе игровые https://www.vaejc.com/profile/lengelzzqvpo/profile Игровые автоматы беÑплатно играть Ð¸Ð½Ð´Ð¸Ñ https://gsallaroundproduction.com/profile/takathe82/profile Играть в игровые автоматы беÑплатно Ñ Ð±Ð¾Ð½ÑƒÑом 5000 https://www.nextoctavemusic.com/profile/judithrachelizw/profile 77 игровые автоматы играть онлайн беÑплатно https://www.7seriesllcnewworldofgrowth.com/profile/vergiew8jennie/profile Rox casino официальный Ñайт 42 https://www.friduchagiftshop.com/profile/judithu7sandra/profile Казуальные игровые автоматы пирамида

where to buy cialis Wang J Yu T Bai R Sun H Zhao X Li Y

These patients require further evaluation for urological abnormalities which is better viagra or cialis Naturland exactly as directed on the package, unless instructed differently by your doctor

Также vavada удваивает первый депозит 100% бонуÑом.Вывод денег Ñ Ð¸Ð½Ñ‚ÐµÑ€Ð½ÐµÑ‚-казино Columbus. http://1mdl.ru/bitrix/click.php?goto=https://usdeil.com/profile/chuckwgewkn/profile Вулкан автоматы играть онлайн http://afex.in/__media__/js/netsoltrademark.php?d=https://www.waxxedruth.com/profile/mattie9emar/profile Бездепозитный Ð±Ð¾Ð½ÑƒÑ Ð½Ð° форекÑе за региÑтрацию http://www.safesoundsecure.com/__media__/js/netsoltrademark.php?d=https://synthiabisui.com/profile/margieyjbeth/profile Azino777 игровые автоматы играть https://maps.google.gl/url?q=https://www.smarterhomeofthecarolinas.com/profile/l3e6alisha/profile Tsars casino отзывы http://duck.com/url?q=https://www.bessboroughschoolcouncil.com/profile/marcellalor2x3w/profile Казино онлайн лицензионный Ñофт ИÑÐ¿Ð¾Ð»ÑŒÐ·ÑƒÑ Ð²Ñе те возможноÑти, которые ÑÐµÐ¹Ñ‡Ð°Ñ Ð¸Ð¼ÐµÑŽÑ‚ игроки можно как в довольно наигратьÑÑ Ð¸ получить зарÑд позитивной Ñнергии, так и неплохо заработать, но вÑÑ‘ завиÑит от цели игры, главное, что Ð´Ð»Ñ Ñтого вÑÑ‘ предуÑмотрено.Злоупотребление Ñтим может иметь обратный Ñффект. https://google.com.my/url?q=https://www.kazuki-gym.com/profile/mannixfalley8/profile Выигрыши в казино вулкан http://maps.google.com.bh/url?q=https://acjelectricco.com/profile/liella7wrq/profile Ðзартные игры игровые автоматы беÑплатно казино вулкан https://www.learnwhatyoudidnt.com/profile/rubyjp2dy/profile ÐмулÑторы автоматов игровых беÑплат https://www.vivace.site/profile/delsiekelseyglq/profile Игровые автоматы вулкан играть беÑплатно онлайн без региÑтрации в демо игры https://fr.fromthegroundupbb.com/profile/chetramytefdb/profile Игровые автоматы птички https://www.imthemonk.com/profile/brandyemily0zw/profile Играть онлайн игры бук оф ра https://www.harmoniousdays.com/profile/milliesaty2/profile Играть в игровые аппараты беÑплатно печки https://artisanose.com/profile/tammyruthr1l/profile Xx football карнавал

The Benefits best price propecia in uk

Разработчики не Ñоздали Ð¿Ñ€Ð¸Ð»Ð¾Ð¶ÐµÐ½Ð¸Ñ Ð Ð¸Ð¾Ð±ÐµÑ‚, но вмеÑто Ñтого адаптировали Ñайт к мобильной верÑии.МакÑимально — 30 000 рублей. http://princetonplastic.surgery/__media__/js/netsoltrademark.php?d=https://beereadyresources.com/profile/su0cddona/profile 1 x slots зеркало http://www.boots-sampling.co.uk/track.ashx?r=https://top9sports.com/profile/cabertocjvkzk/profile Игровые автоматы беÑплатно king tusk кинг таÑк http://www.billhutchinson.com/__media__/js/netsoltrademark.php?d=https://www.mypropertyatlas.com/profile/spbvferica/profile Игровые автоматы книжки беÑплатно и без региÑтрации https://images.google.ca/url?q=https://www.kayemjay6.com/profile/beulahwillie9s3/profile Игровые автоматы дембель играть беÑплатно https://maps.google.com.au/url?q=https://www.intechprotect.co.uk/profile/eslavafmubie/profile Ключи Ñлепки Ñделать игровые автоматы Информацию о лицензии, адреÑа и другую организационные данные вы можете найти на официальном Ñайте Booi casino в разделах «О наÑ» и «Правила и уÑловиÑ».ПриÑÑ‚Ð½Ð°Ñ Ð°Ñ‚Ð¼Ð¾Ñфера праздника, приподнÑтое наÑтроение, Ñркие моменты, крупные выигрыши: интернет казино Вулкан 24 приглашает Ð²Ð°Ñ Ð¾ÐºÑƒÐ½ÑƒÑ‚ÑŒÑÑ Ð² Ñтот великолепный мир приключений и азарта! https://images.google.ac/url?q=https://www.snsdoga.com/profile/suefx6jlauren/profile Играть онлайн беÑплатно без региÑтрации игровые автоматы Ñвиньи https://images.google.ru/url?q=https://www.ruusujarosmariini.com/profile/alishaxvwokim/profile ÐмулÑторы игровых автоматов из игро https://www.voiceurstory.com/profile/cabertocjvkzk/profile Играть в олимп на игровых автоматах https://ts.boporev.com/profile/dolliectu1helen/profile Онлайн автоматы играть беÑплатно Ñ Ð±Ð¾Ð½ÑƒÑами игровые вÑе https://www.drticm.com/profile/doingrmmfbn/profile Игровой автомат огниво играть https://www.reneewilde.com/profile/vivpjody/profile Борьба Ñ Ð¸Ð³Ñ€Ð¾Ð²Ñ‹Ð¼Ð¸ автоматами https://www.rodsandreels.info/profile/jaimes2bldora/profile Казино вулкан casino https://www.skyhighmunchies.com/profile/perkeyramach8/profile Вулкан 24 игровые автоматы официальный Ñайт на деньги

vardenafil online pharmacy The consequences of low adherence to tamoxifen are poorer health outcomes, increased health care costs and worse quality of life

МультиÑÐ·Ñ‹ÐºÐ¾Ð²Ð°Ñ Ð¿Ð»Ð°Ñ‚Ñ„Ð¾Ñ€Ð¼Ð° поддерживает перевод Ñайта на 15 Ñзыков, Ð´ÐµÐ»Ð°Ñ ÐºÐ¾Ð¼Ñ„Ð¾Ñ€Ñ‚Ð½Ð¾Ð¹ игру Ð´Ð»Ñ Ð²Ñех поÑетителей; раздел Ñ Ð¿Ð»Ð°Ñ‚ÐµÐ¶Ð°Ð¼Ð¸, где раÑположены вÑе доÑтупные ÑпоÑобы внеÑÐµÐ½Ð¸Ñ Ð´ÐµÐ¿Ð¾Ð·Ð¸Ñ‚Ð° и вывода выигрыша Ð´Ð»Ñ Ð¶Ð¸Ñ‚ÐµÐ»ÐµÐ¹ из разных Ñтран; кнопки Ð¿Ñ€Ð¾Ð¸Ð·Ð²ÐµÐ´ÐµÐ½Ð¸Ñ Ñ€ÐµÐ³Ð¸Ñтрации и авторизации в ÑиÑтеме.ЛоÑльноÑÑ‚ÑŒ казино к игрокам. http://krepush-shop.ru/bitrix/rk.php?goto=https://www.thepartybagzguru.com/profile/null/profile Ð–ÐµÐ¼Ñ‡ÑƒÐ¶Ð½Ð°Ñ Ð»Ð°Ð³ÑƒÐ½Ð° http://www.teko.biz/bitrix/redirect.php?goto=https://riverfc.org/profile/christinesha82/profile Чужие играть игровые автоматы http://hedgefundmanagers.com/__media__/js/netsoltrademark.php?d=https://www.naturalfunkmovement.net/profile/muwyjimmie/profile Лучшие западные партнерки казино https://www.google.at/url?q=https://annisacoaching.com/profile/jeneca0wuz/profile Где можно поиграть онлайн в игровые автоматы беÑплатно https://maps.google.ch/url?q=https://www.rv-wangen.ch/profile/josephinegkcqb/profile Игровой автомат sizzling hot Ñизлинг хот Ðа реÑурÑе еÑÑ‚ÑŒ баннеры, которые подÑкажут гÑмблеру о текущих и новых акционных предложениÑÑ….Я говорю не только про количеÑтво, разнообразие и качеÑтво так же важны. https://www.google.sm/url?q=https://tiobruninho.com/profile/mahoneparlowe/profile Промокод на вулкан 777 https://maps.google.ms/url?q=https://www.synapsecircus.com/profile/savannahflolj86/profile Ðвтомат крейзи фрут играть беÑплатно без региÑтрации https://iblankewe.com/profile/josephinegkcqb/profile ВеÑÐµÐ»Ð°Ñ Ñ„ÐµÑ€Ð¼Ð° рулетка играть онлайн беÑплатно https://morganrojasphotography.com/profile/selenehollyt7/profile Ð’Ñе любимые игровые автоматы https://www.hockeyforlife.org/profile/mousseaurmxsqv/profile Вулкан Ð°Ð»ÑŒÐºÐ°Ñ‚Ñ€Ð°Ñ Ð¸Ð³Ñ€Ð°Ñ‚ÑŒ беÑплатно и без региÑтрации https://www.accredentials.com/profile/mic29h9elaine/profile Ðвтоматы игровые онлайн беÑплатно без региÑтрации Ñкалолаз https://www.teeponline.com/profile/lorridwconnie/profile Играть в игровых автоматах онлайн crazy monkeys https://www.enricofinazzi.com/profile/marlfzkyasuko/profile Ðдмирал Ð¸ÐºÑ Ð¾Ñ‚Ð·Ñ‹Ð²Ñ‹

propecia or rogaine The recurrence rates were 14

These results suggested that water and a mixture of water and organic solvent should be used for the manufacturing process with special attention paid to the transformation to tamoxifen hemicitrate sesquihydrate, because it showed a different stoichiometry from the active ingredient, tamoxifen citrate priligy tablets price In the search for optimal hormone replacement therapy during menopause, it was observed that tamoxifen has variable antiestrogenic and estrogenic actions in different tissues

Обычно Ñ Ð¿Ð¾Ð»ÑŒÐ·ÑƒÑŽÑÑŒ банковÑкой картой, однако пару раз выводил деньги и на Ñлектронные кошельки, вÑе проходило гладко.ОтноÑительно лимитов 5 000 000 в Ñутки можно будет получить, но тут завиÑит от ÑтатуÑа Вашего аккаунта. http://flogroup.com/__media__/js/netsoltrademark.php?d=https://www.ashericmeditation.com/profile/dmitriy5w4wig/profile Игровые автоматы бомбочки играть http://www.miraton.ua/bitrix/redirect.php?goto=https://wimaumayouthsoccer.com/profile/yannuccibnjuzu/profile ÐœÐ¾Ð±Ð¸Ð»ÑŒÐ½Ð°Ñ Ð²ÐµÑ€ÑÐ¸Ñ Ð¸Ð³Ñ€Ð¾Ð²Ñ‹Ðµ автоматы играть беÑплатно http://bswsemi.com/__media__/js/netsoltrademark.php?d=https://r-mobius.com/profile/cindywfximavis/profile Слот на деньги без региÑтрации http://google.com.af/url?q=https://www.earthpoetedgeweaver.com/profile/waltermindy02/profile Казино вулкан украина в грн в https://maps.google.vg/url?q=https://cocooncoachingsolutions.com/profile/chetramytefdb/profile Игровые автоматы зарабатывать деньги Ð˜Ð½Ñ‚ÐµÑ€Ñ„ÐµÐ¹Ñ Ð²Ñ‹Ð¿Ð¾Ð»Ð½ÐµÐ½ в египетÑком Ñтиле.Она раÑÑчитываетÑÑ Ð¿Ð¾ результатам игр и может быть довольно крупной. https://google.fm/url?q=https://www.yourmagicalmilk.com/profile/lydiaceqm/profile Игровые автоматы Ñкачать беÑплатно swf на телефон http://google.cv/url?q=https://www.bloomingpixie.co.uk/profile/jeneca0wuz/profile Голдфишка казино Ð¼Ð¾Ð±Ð¸Ð»ÑŒÐ½Ð°Ñ Ð²ÐµÑ€ÑÐ¸Ñ Ð¸Ð³Ñ€Ð°Ñ‚ÑŒ онлайн https://www.cinnamonbay.co.uk/profile/louiseq1ger/profile Ð›Ð¾Ñ‚ÐµÑ€ÐµÑ Ð¾Ð½Ð»Ð°Ð¹Ð½ казино https://www.hcboc.org/profile/goukeraumfxy/profile Телефон казино вулкан Ñактбург петер https://elandoptimisme.com/profile/joannegertieclb4/profile С игры официальный Ñайт https://www.theeverydaymonet.com/profile/patty7leklillie/profile ПÑтигорÑк казино фараон https://www.philwatsonmusic.com/profile/enrtamara1q/profile Играть игровые автоматы онлайн на деньги Ñ Ð²Ñ‹Ð²Ð¾Ð´Ð¾Ð¼ на карту https://motelx.app/profile/lindah47sheryl/profile Игровые автоматы играть реально на деньги

СпиÑок азартных игр в казино Вулкан Миллион.Страны: РоÑÑÐ¸Ñ Ð’ÐµÐ¹Ð´Ð¶ÐµÑ€: 30Ñ… Промокод: Ðет. https://www.allnaturallandscapes.com/profile/ancisowhaleyw/profile Играем в казино без вложений

Tamoxifen therapy was associated with a decreased risk of contralateral breast cancer mOR 0 how to buy priligy as a child

cheapest cialis micardis bactroban pomada bula profissional A spokeswoman for the health board said These concerns relate to the nasal spray vaccine which contains a tiny amount of gelatine of pork origin used during the manufacturing process

Ð”Ð»Ñ Ð¸Ð³Ñ€Ð¾ÐºÐ° ÑвлÑетÑÑ Ð±Ð¾Ð»ÐµÐµ удобным вариантом, когда Ð´ÐµÐ½ÐµÐ¶Ð½Ð°Ñ ÐµÐ´Ð¸Ð½Ð¸Ñ†Ð° ÑвлÑетÑÑ ÐµÐ³Ð¾ родной валютой и он точно знает Ñколько выиграл, без какого либо переÑчёта по курÑу других валют.Ðта авÑтрийÑÐºÐ°Ñ Ð¸Ð½Ñ‚ÐµÑ€Ð½ÐµÑ‚-платформа даёт возможноÑÑ‚ÑŒ игрокам почти из вÑех Ñтран мира играть через браузер, не ÑÐºÐ°Ñ‡Ð¸Ð²Ð°Ñ Ð¿Ð¾Ð»ÑŒÐ·Ð¾Ð²Ð°Ñ‚ÐµÐ»ÑŒÑкий кабинет. https://www.gal-goldner.com/profile/marqueritekim4w/profile Slotoking бездепозитный Ð±Ð¾Ð½ÑƒÑ +при региÑтрации

An otherwise healthy middle aged woman is diagnosed with prehypertension according to current guidelines generic levitra 40mg

how effective is propecia Liu, Zhenbin, et al

Примерно 85% вÑех предÑтавленных продуктов – Ñто игровые автоматы.Громоздкий Ñщик Ñ Ñ‚Ñ€ÐµÐ¼Ñ Ð±Ð°Ñ€Ð°Ð±Ð°Ð½Ð°Ð¼Ð¸ и плоÑÐºÐ°Ñ Ñ‚Ð°Ð±Ð»Ð¸Ñ‡ÐºÐ° перед глазами Ñ Ð¸Ð·Ð¾Ð±Ñ€Ð°Ð¶ÐµÐ½Ð¸Ñми комбинаций. https://stuckabroadtravels.com/profile/schwarkbdrlwf/profile СтатуÑÑ‹ вулкан казино

Pharmaqo Labs Tamoxifen Nolvadex 50 tab x 20mg is a prescription medicine to treat breast cancer buy cialis 20mg The risk of hypersusceptibility reactions Stevens Johnson syndrome, neutropenia, hepatotoxicity, aseptic meningitis, thrombocytopenia is also higher than in other patients

Тем, кто только оÑваивает виртуальный мир развлечений, подойдет игра без региÑтрации в демонÑтрационном режиме.И тут наткнулÑÑ Ð½Ð° казино Вулкан РоÑÑиÑ, ткнул Ñлучайно в один из игровых автоматов, Reel Rush что ли. https://transcendententerprises.org/profile/wanda9yu8k/profile Ðовинки в казино вулкан

cialis vs viagra envoy Lakhdar Brahimi, Lavrov and Kerry said they hoped to meet in New York in about two weeks, around September 28 during the U

И чтобы не попаÑÑ‚ÑŒ в неприÑтную Ñитуацию, получить от игрового процеÑÑа маÑÑу положительных Ñмоций и впечатлений, пользователю Ñледует поÑещать только лицензионные онлайн казино.Сайты отличаютÑÑ Ñ‚Ð¾Ð»ÑŒÐºÐ¾ адреÑом, где доменное Ð¸Ð¼Ñ Ð¼Ð¾Ð¶ÐµÑ‚ быть измененным. http://psy-ego.site/bitrix/rk.php?goto=https://www.gocheelabs.com/profile/kangela9e/profile Играть в кинг конга игровые автоматы играть http://m.ok.ru/dk?st.cmd=outLinkWarning&st.cln=off&st.typ=link&st.rtu=/dk?st.cmd=altGroupForum&st.tagId=-1801480381&st.groupId=51020083626056&_prevCmd=altGroupForum&tkn=8961&st.rfn=https://toasteriacafe.com/profile/erindorish3/profile БеÑплатные игры онлайн игровые автоматы гаминатор http://cdldiscovery.com/__media__/js/netsoltrademark.php?d=https://www.bridgingchessgapsorg.com/profile/kavaneyzycvpe/profile Ðнгел ок Ñлот Ñкачать беÑплатно https://toolbarqueries.google.ga/url?q=https://www.hudsonhilliard.com/profile/licariebzjje/profile Что игровыми автоматами в белоруÑÑии https://www.google.info/url?q=https://www.swishasuites.com/profile/williehpyk/profile Кто Ñоздал рулетку Ð´Ð»Ñ ÐºÐ°Ð·Ð¸Ð½Ð¾ Программа лоÑльноÑти подразумевает шеÑÑ‚ÑŒ игровых ÑтатуÑов, которые повышаютÑÑ Ð·Ð° активноÑÑ‚ÑŒ Ð¿Ð¾Ð»ÑŒÐ·Ð¾Ð²Ð°Ñ‚ÐµÐ»Ñ Ð¸ приноÑÑÑ‚ ему дополнительные преимущеÑтва.Можно Ñтавить Ñколько угодно ÑредÑтв, делать различные Ñтавки, регулировать количеÑтво линий. https://toolbarqueries.google.am/url?q=https://fi.highzenbirds.com/profile/mic29h9elaine/profile Ðвтомат победа играть https://www.google.net/url?q=https://www.miriamstewart-kroeker.com/profile/kevorkianjnhfax/profile Сила удара на игровом автомате в чем измерÑетÑÑ https://www.proagdistributors.com/profile/wolfferolarkh/profile Гранд вулкан казино на деньги https://www.bro-ink.com/profile/josephinegkcqb/profile Rock climber Ñкалолаз игровой автомат https://www.wearemonocle.org/profile/dawnz5jmarion/profile Игровые автоматы Ñ Ð¼Ð¾Ð¼ÐµÐ½Ñ‚Ð°Ð»ÑŒÐ½Ñ‹Ð¼ выводом ÑредÑтв slots games https://www.oleksandrkisil.com/profile/c9nebrandy/profile Ðзарт плей играть беÑплатно и без региÑтрации https://dominikkrata.com/profile/nockaibotwinp/profile Игровые автоматы на деньги через webmoney https://www.breatheasysupyoga.com/profile/adelepatpm/profile Играть в автоматы без региÑтрации беÑплатно онлайн играть братва

Byron xKKZyyesrz 5 29 2022 buy cheap propecia uk LГіpez JuГЎrez, Alejandro; Titus, Haley E; Silbak, Sadiq H; Pressler, Joshua W; Rizvi, Tilat A; Bogard, Madeleine; Bennett, Michael R; Ciraolo, Georgianne; Williams, Michael T; Vorhees, Charles V; Ratner, Nancy 2017

Также в онлайн заведениÑÑ… чаÑто играют в беÑплатном режиме профеÑÑиональные игроки, которые желают отработать Ñвои новые тактики и Ñтратегии,а уже поÑле играть на реальные деньги.Ðкции и турниры casino Vulcan Pobeda. http://wellnessbeauty.ru/bitrix/redirect.php?goto=https://www.janieledford.com/profile/rollagdantosk/profile Игровые автоматы однорукие банди http://1800cellini.cc/__media__/js/netsoltrademark.php?d=https://healingrestorationministries.com/profile/lengelzzqvpo/profile Вулкан ÑÑ‚Ð°Ñ€Ñ Ð²Ñ‹Ð²Ð¾Ð´ денег отзывы http://konda-trade.ru/bitrix/rk.php?goto=https://www.richmondhill-artschool.com/profile/brandyemily0zw/profile Играть в автоматы Ñлоты беÑплатно и без региÑтрации в хорошем качеÑтве http://www.bon-vivant.net/url?q=https://www.thewolvezden.com/profile/rubymypida/profile Музей игровых автоматов на кузнецком https://www.google.co.in/url?q=https://saberstrikekenpo.com/profile/erindorish3/profile Вывод денег Ñ ÐºÐ°Ð·Ð¸Ð½Ð¾ вулкан на киви Ðи в коем Ñлучае не полагайтеÑÑŒ Ñлепо на данные из одного иÑточника.К началу нового века активной разработкой Ñофта также занималиÑÑŒ Playtech и Microgaming. https://maps.google.com.na/url?q=https://www.standupandlaughtour.com/profile/lucy55laurel/profile БлÑкджек очки http://www.google.ie/url?q=https://www.kamerongroup.com/profile/jeffriescivalx/profile Вулкан bit казино https://www.lynncahoon.com/profile/chrlily2om2/profile Самый большой джекпот в казино https://www.clubedapesca.org/profile/tabionlucidif/profile Ðвтоматы азартные игры игровые автоматы играть беÑплатно без региÑтрации https://www.shinepediatrictherapy.com/profile/cabertocjvkzk/profile Ðвтоматы игровые играть беÑплатно онлайн пирамида https://teresasfinehomedecor.com/profile/marlfzkyasuko/profile Игровые автоматы Ð±Ð¾Ð½ÑƒÑ Ð·Ð° региÑтрацию номера телефона https://www.magnusmakesbeats.com/profile/yannuccibnjuzu/profile Играть в обезьÑнку беÑплатно и без региÑтрации автоматы игры https://www.neayi.org/profile/viallgiangm/profile Плей вулкан хуз

ly yU1O3VJ tallahassee police watch sheep pussy enforce watermelon railroad fang hut effects of interracial dating hair loss propecia In certain embodiments, a compound provided herein, or an enantiomer or a mixture of enantiomers thereof, or a pharmaceutically acceptable salt, solvate, hydrate, co crystal, clathrate, or polymorph thereof, is administered to patients with various types or stages of solid tumors in combination with celebrex, etoposide, cyclophosphamide, docetaxel, apecitabine, IFN, tamoxifen, IL 2, GM CSF, or a combination thereof

Выбирать тот или иной вариант Ñледует в ÑоответÑтвии Ñ Ð»Ð¸Ñ‡Ð½Ñ‹Ð¼Ð¸ предпочтениÑми, Ñ…Ð¾Ñ‚Ñ Ð¼Ð¾Ð¶Ð½Ð¾ иÑпользовать оба по Ñитуации.Самые Ñовременные игровые автоматы от лучших провайдеров. http://gregpellegrino.com/__media__/js/netsoltrademark.php?d=https://gentryesq.com/profile/takathe82/profile Игровые автоматы Ñейф онлайн беÑплатно http://a-kaunt.com/bitrix/click.php?goto=https://www.socialelegance.org/profile/ashleyrosgpp/profile Рупий вулкан игровые автоматы http://goodoutdoor.jp/staff/?wptouch_switch=desktop&redirect=https://www.bellasyouniquebridal.com/profile/suzannekam5xb/profile Casino 777 отзывы https://images.google.cf/url?q=https://www.isakalak.com/profile/analicia6v/profile Как переÑтать играть в Ñлоты игровые автоматы https://toolbarqueries.google.bi/url?q=https://www.glowandhossana.com/profile/delialeannexyj4/profile Aztec gold играть беÑплатно без региÑтрации Ñо Ñтавкой 10000 игровой автомат Каждый игрок может ÑамоÑтоÑтельно выбрать Ð´Ð»Ñ ÑÐµÐ±Ñ Ð¿Ð¾Ð´Ð°Ñ€Ð¾Ðº.ЕÑли бы казино вело дейÑтвительно чеÑтную игру, оно так не разбраÑывалоÑÑŒ бонуÑами. http://maps.google.ee/url?q=https://www.lauralebouteiller.com/profile/chuckwgewkn/profile Вулкан казино играть беÑплатно и без региÑтрации онлайн Ñейфы http://maps.google.co.jp/url?q=https://www.pierre-flore-immobilier.com/profile/glisaaza/profile Казино онлайн Ð±Ð¾Ð½ÑƒÑ Ð·Ð° региÑтрацию Ñ ÐºÐ¾Ð´Ð°Ð¼Ð¸ активации https://praisefellowshipchurchchatham.com/profile/blanca7erowena/profile Игры игровые автоматы книги https://es.socalservicecorps.org/profile/johannab4zaa/profile Играть в игровые автоматы макÑбет беÑплатно https://www.trinitydesignsinc.com/profile/peggysherri1obh/profile Онлайн рулетка на деньги реально https://the-gaia-method.com/profile/sheryl4bjoyce/profile Играть онлайн беÑплатно азартные игры автомат https://electriccarconverts.com/profile/alishaxvwokim/profile Hot seven игровые автоматы https://www.fuelingforward.com/profile/heathervbx2geo/profile Из чего ÑоÑтоит французÑÐºÐ°Ñ Ñ€ÑƒÐ»ÐµÑ‚ÐºÐ°

women either 60 years of age or older or between 35 and 59 years of age with a five year predicted risk for breast cancer of at least 1 best cialis online The findings provide a new way of looking at metastasis and its possible treatment

ÐдминиÑÑ‚Ñ€Ð°Ñ†Ð¸Ñ Ð¿Ð¾Ð·Ð²Ð¾Ð»Ñет иÑпытывать игровые автоматы VAVADA беÑплатно.ПроверÑйте наличие лицензии у игорного заведениÑ. http://my.hisupplier.com/logout?return=https://www.smithslocdin.com/profile/judithu7sandra/profile Екатеринбург продажа игровых автоматов http://goldlighting.ru/bitrix/redirect.php?goto=https://www.winkelvanmoos.nl/profile/tawanalila6c/profile Игровой автомат ÑÑÑÑ€ играть без региÑтрации http://movingwords.com/__media__/js/netsoltrademark.php?d=https://www.citizenscientistlife.com/profile/r954xmiriam/profile УральÑк игровые автоматы https://maps.google.pl/url?q=https://www.alliellephotos.com/profile/mouwbaldo2/profile Рулетка онлайн играть беÑплатно флеш https://google.dk/url?q=https://www.majesticmotions.com/profile/lorridwconnie/profile Промокод вулкан лев Ð’Ñего пара кликов мышкой отделÑет Ð²Ð°Ñ Ð¾Ñ‚ Ñуконного игрового Ñтола, Ñвоенравной рулетки или «однорукого бандита».Ðто нужно понимать перед началом региÑтрации. http://images.google.bg/url?q=https://www.dialuxeaesthetics.com/profile/junejerrieruq/profile Какой Ñайт +у азино 777 https://toolbarqueries.google.cm/url?q=https://www.kanbutsu-curryday.com/profile/lobnerbuhite0/profile Игровые автоматы онлайн crazy monkey играть беÑплатно https://opad-dijon.fr/profile/rubymypida/profile Играть в человека Ñ Ð°Ð²Ñ‚Ð¾Ð¼Ð°Ñ‚Ð¾Ð¼ https://www.rikarron.co.uk/profile/mayboyasuko/profile Со Ñкольки лет можно играть в казино https://www.ferienhaus-pieper.com/profile/jeneca0wuz/profile Игровой зал автомат играть беÑплатно https://www.ejadacapital.com/profile/rehorbadinin/profile Hot target игровой автомат играть беÑплатно без региÑтрации https://raphaelgraciolli.com/profile/doris1pddelsie/profile Онлайн казино azino777 играть официальный https://www.madebymorgaine.co.uk/profile/cucinottacuxszx/profile Бездепозитный Ð±Ð¾Ð½ÑƒÑ Ð¸Ð³Ñ€Ð¾Ð²Ñ‹Ðµ автоматы 2022 Ñ Ð²Ñ‹Ð²Ð¾Ð´Ð¾Ð¼

where to buy cialis online forum 58, 59 Four subsequent trials 6, 60 62 using different dosages and types of ОІ blockers failed to reproduce these benefits

The presence of methoxyphenols results from pyrolysis of lignin whereas levoglucosan is released during combustion of cellulose 104, 107 buy cialis online india He has never been able to take that step, but now Zhao Qingzhu has reached the state of Void Transformation

Here, you will find that the initial deposit that you make with the BTC Casino will at least be matched with bonus cash.This license allows them to get access to banking services, and the site claims to soon have its own functioning fiat currency gateway.Great welcome package, attractive loyalty offers, vast game selection, and effective customer support. http://visitorsguidetexas.com/__media__/js/netsoltrademark.php?d=https://www.greenlifepharmaceuticals.com/profile/crespoalveze/profile Holland casino den bosch adres http://subarist.ru/bitrix/click.php?goto=https://www.themudpeddler.com/profile/reddoxgwfi/profile 1000 free games to play now http://www.oceanstatesummer.com/__media__/js/netsoltrademark.php?d=https://www.candlecrate.net/profile/wishumpoper6/profile Best way to stop online gambling http://maps.google.ml/url?q=https://www.littlefisheshemsworth.com/profile/bhatiacederf/profile Poker room rond alba iulia https://maps.google.co.nz/url?q=https://emilyfrances-design.com/profile/sopkofreelr/profile Graton casino shuttle from sf Best casinos to play Bitcoin dice – TOP 4 list: CryptoGames – Fast provably fair Bitcoin dice with great jackpots DuckDice – Provably fair Bitcoin dice with jackpots and hilarious bonuses FortuneJack – Provably fair Bitcoin dice with a huge jackpots + 2 Bitcoin Craps games BetChain – Bitcoin Craps, Rocket Dice and Bitcoin Sic Bo games available.If you claim over 120 times in 24 hours, you will be banned permanently and will not get your payout.The 10CRIC welcome bonus comes in the form of a big package with five smaller bonuses in it. http://maps.google.by/url?q=https://www.camprosendalekpcc.org/profile/faylorbaub/profile Lakeside frontier riders poker ride https://maps.google.com.vc/url?q=https://www.thedamicos2022.com/profile/mantheirysina/profile 500 club casino clovis california https://www.sostante.org/profile/tomkuswymilv/profile Difference between casino and poker https://vi.foreveramber.net/profile/calipjqznym/profile Top online casino games https://www.deswormsandbait.com/profile/judicellbwal/profile Casino shop rue nancel penard bordeaux https://www.devilscreekjackrussells.com/profile/wishumpoper6/profile Omg fortune free slots casino https://www.tomokojazz.net/profile/suharik071/profile Red dragon casino mountlake terrace wa https://www.acossportsclub.com/profile/mcspaddenranxux/profile Free poker downloads for android With OUR OWN MONEY..Here are some of the highlights.

ÐеÑÐ¼Ð¾Ñ‚Ñ€Ñ Ð½Ð° то, что мы ÑтараемÑÑ Ð¼Ð¾Ð´ÐµÑ€Ð¸Ñ€Ð¾Ð²Ð°Ñ‚ÑŒ вÑе комментарии, чеÑтноÑÑ‚ÑŒ мнений проверить можно не вÑегда.Ð’ 1X-Slots можно играть на Ñвоем родном Ñзыке их вÑего более 60 и абÑолютно в любой валюте (вÑе валюты мира, хоть гривны, тенге, рубли, тугрики, динары, да что угодно), причем в Ñвоем аккаунте можно открыть любое количеÑтво кошельков в любой валюте. http://myliferesource.net/__media__/js/netsoltrademark.php?d=https://shopbambana.com/profile/licariebzjje/profile Онлайн казино whiteclub http://russianschoolgirls.net/out.php?https://www.moida.space/profile/josephiner0k2cha/profile Игровые автоматы каруÑель http://wkkf.us/__media__/js/netsoltrademark.php?d=https://renewfloatspa.com/profile/kibbeestemano/profile Игры онлайн игровые автоматы пираты https://images.google.sc/url?q=https://babypalace.shop/profile/staceysarahdr/profile Ðзарт игровой казино автоматы беÑплатно https://toolbarqueries.google.co.il/url?q=https://www.kcstreetwars.com/profile/vorosocjdvi/profile Лучшие i руÑÑкие игровые автоматы играть Во втором Ñлучае у игроков поÑвлÑетÑÑ Ð²Ð¾Ð·Ð¼Ð¾Ð¶Ð½Ð¾ÑÑ‚ÑŒ выигрыша одного из актуальных джекпотов, Ñовременные гаджеты или путешеÑÑ‚Ð²Ð¸Ñ Ð² жаркие Ñтраны.СÑм знает, как зарабатывать, и умеет Ñто делать. https://toolbarqueries.google.al/url?q=https://www.raisingachampion.org/profile/juneqrcha/profile Игровые автоматы Ñкачать беÑплатно slot o pol http://www.google.com.tr/url?q=https://knot-lab.com/profile/sharronjry3pri/profile Игровые автоматы book of magic https://www.vincentpremel.fr/profile/viallgiangm/profile Игровые автоматы где на дубль выпадают бутылочки https://www.peter53.com/profile/torriexrbamu/profile Игровые автоматы играть беÑплатно вÑе игры карты https://goodvibeksa.com/profile/lisarobin58l/profile Вулкан игровые автоматы за рубли https://www.cassandrajanecooper.com/profile/edelsie98yc/profile Игровые аппараты играть беÑплатно без региÑтрации онлайн https://ppwebpros.com/profile/edithjptmina/profile Вулкан Ñтавка ком на деньги https://artvancouver.net/profile/balsteraicxwd/profile Игры онлайн руÑÑÐºÐ°Ñ Ñ€ÑƒÐ»ÐµÑ‚ÐºÐ° беÑплатно без региÑтрации

Sizing of the target sample propecia before and after 8 million pounds 10

Catch the action from big sports and major sporting events from the Super Bowl to the FIFA World Cup to hot new sports like esports and UFC and even non-sports events like politics and award shows in entertainment.Dogecoin’s value is very low, so you can do Dogecoin gambling very cheap!Intertops Casino – Get up to $2,000 + free spins. http://sawparts.com/__media__/js/netsoltrademark.php?d=https://theoriginaldisneygirl.com/profile/siviemastinl/profile Team fortress 2 fabricate slot token http://presidentofabkhazia.org/bitrix/click.php?goto=https://lgfrenchieoutfitter.com/profile/kilbeerlee/profile Escalante utah slot canyons spooky http://lanta27.ru/bitrix/redirect.php?goto=https://www.indysicilianfest.com/profile/ilyapmto/profile Kenapa turn poker tidak bisa dibuka http://google.cg/url?q=https://en.dbrl.no/profile/noltminniey/profile Double down casino free share codes https://toolbarqueries.google.com.ar/url?q=https://www.saintvilleent.com/profile/druetaakei/profile Wizard of oz slot machine app Slots range from classic games to non-standard five-reel slots, while many of the site’s live casino games offer realistic 3D graphics.This is a trick to make you try newly released game hopping that you will deposit money to continual the play.Read this brief review and find out why it’s is praised so much by millions of gamblers worldwide. https://toolbarqueries.google.com.et/url?q=https://www.garrettkahrs.com/profile/tintlesmyrlf/profile El torero casino game online http://images.google.com.sb/url?q=https://www.elitesportsacademy.org/profile/eisleyrochow7/profile Does any online casino accpept discover https://www.wombatswoodshop.com/profile/wipflibeschp/profile Casino trips to biloxi from houston https://www.sagebirdciderworks.com/profile/muhnitkybf/profile Oneida casino smoke shop hours https://www.ericisiahmedia.com/profile/rapozomedill4/profile Ft sill apache casino lawton ok https://www.cemtech-energy.com/profile/wishumpoper6/profile Poker zora neale hurston theme https://www.mathmobile.org/profile/lunneygamezp/profile Free slot games at mecca https://www.breakthroughrevcorp.com/profile/billeylamelaz/profile Classifica torneo poker saint vincent How Long Does It Take Bitcoin Transactions To Process?The BTC is instantly added to your FreeBitco.

canada pharmacy viagra Occasionally, b efficacy study, and prevent a pelvic examination can be dose- related, patients

Радует наличие провайдера Push Gaming и BTG (они не так чаÑто попадаютÑÑ Ð² онлайн казино и вÑтретить их можно только в лучших).Я вижу очевидные доÑтоинÑтва у Ñего портала — еÑÑ‚ÑŒ нормальнаÑ, не ÐºÐ¸Ð´Ð°ÑŽÑ‰Ð°Ñ Ñ‚ÐµÐ±Ñ Ð¿Ð¾Ð´Ð´ÐµÑ€Ð¶ÐºÐ°, еÑÑ‚ÑŒ возможноÑÑ‚ÑŒ играть в то, что твоей душе угодно, ÑпиÑок игр большой. http://ayurvedayoga.ru/bitrix/rk.php?goto=https://www.cane-fu.de/profile/tawanalila6c/profile Вулкан лев игровые автоматы беÑплатно http://digimaru.com/__media__/js/netsoltrademark.php?d=https://www.mokshaessentials101.com/profile/lucy55laurel/profile Zzslot зеркало рабочее http://esetnod32.ru/bitrix/redirect.php?goto=https://laurantstyling.nl/profile/toriw3wtdona/profile Игра в казино Ñ ÐºÑƒÐ±Ð¸ÐºÐ°Ð¼Ð¸ https://images.google.com.vn/url?q=https://www.ccc4c.org/profile/erindorish3/profile Казино и игровые автоматы на украине аризона http://images.google.com.qa/url?q=https://www.theseijitsukarateclub.com/profile/nemansevertg/profile Промокод вулкан на ÑÐµÐ³Ð¾Ð´Ð½Ñ Ð±ÐµÐ·Ð´ÐµÐ¿Ð¾Ð·Ð¸Ñ‚Ð½Ñ‹Ð¹ Ð±Ð¾Ð½ÑƒÑ Ð²ÐµÐ³Ð°Ñ Ð¢Ð°ÐºÐ¶Ðµ можно переключитьÑÑ Ð½Ð° автоигру.Правила отыгрыша данного бонуÑа предполагают 20Ñ… кратный вейджер. http://plus.google.com/url?q=https://www.wovenfoods.com/profile/mattie9emar/profile Игровые автоматы пополнить Ñ Ð¼Ð¸Ñ€ http://www.google.nu/url?q=https://www.lindahendersonartist.com/profile/licariebzjje/profile Игры в игровые автоматы Ð´ÐµÑ€ÐµÐ²Ð½Ñ Ð´ÑƒÑ€Ð°ÐºÐ¾Ð² https://thealohastyle.com/profile/joannegertieclb4/profile Играть беÑплатно игровые автоматы olivers bar https://www.vitrinelocal.com/profile/celiabeataswg0/profile Играть в игровой автомат ÐºÐµÐºÑ Ð±ÐµÑплатно https://www.simplifyingaspaceforjoy.com/profile/bongahamerso/profile Poker windjammer игровой автомат онлайн беÑплатно https://www.jeffriesfarmandflower.net/profile/hawsfnspig/profile Игровые автоматы крейзи фрут беÑплатно без региÑтрации https://www.redlac-af.org/profile/kavaneyzycvpe/profile Crazy monkey ÑимулÑтор игровых автоматов https://www.quasarquantumyouthfund.org/profile/grigoriysehh/profile Игра игровые автоматы без региÑтрации гаминаторы

viagra vs cialis ATTENTION PHARMACIST Medication Guide and device User Manual for patient inside carton

Second deposit bonus is 50% up to 1 BTC.For instance, some bitcoin bonuses are exclusively for mobile while others can be claimed for desktop versions of a site only.The registration process with Crypto Nation Pro is simple and secure. http://wwwgam.matchfishing.ru/bitrix/redirect.php?goto=https://www.snapmagicmedia.com/profile/zukgoletzn/profile Wilhelm incentive program casino http://slavdvor.ru/bitrix/rk.php?goto=https://www.mingjielei.com/profile/ishizumwjako/profile Royal flush folding poker table http://newmount.net/?URL=https://jadecitycoffee.com/profile/kenleymerzigs/profile Free slot games to play for fun paddy power https://toolbarqueries.google.co.id/url?q=https://www.lojamandidesign.com/profile/marekdoonanx/profile Play casino online no deposit http://maps.google.bs/url?q=https://www.invigoratetraining.com/profile/gogliadepenat/profile Golden nugget casino girls online Such online casinos include: Uptown Pokies – Claim Your Free AU$10.The process leverages mathematical algorithms and cryptography.We feature the best bitcoin casinos where you are sure to find major game providers like NetEnt, Microgaming, Betsoft, Play’n GO, Quickspin, Thunderkick and more. http://google.ga/url?q=https://www.brittheartist.com/profile/papikrestert/profile Reasons why gambling should not be banned http://images.google.ht/url?q=https://www.vttactical.com/profile/pundtnyex/profile Table mountain casino 8184 table mountain road friant california 93626 https://www.beatrizlumo.com/profile/prialwnueux/profile Casino shuttle from hamilton to niagara falls https://www.influencersocietyclub.com/profile/shurrpinellq/profile Play poker online max games https://www.omgnight.com/profile/mavesjevldg/profile Bitcoin gambling site https://samrassy.com/profile/perksdorsta/profile Cryptocurrency slots https://www.axxashop.fi/profile/sykesbatony/profile Casino drive croix daurade toulouse https://www.ejyerzak.com/profile/carolco1mf/profile Final fantasy 7 slot machine My first thought is always, “You must not play much (or any) live poker.The main reason that many of these casinos are switching to bitcoin is because this unique cryptocurrency comes with withdrawal options that do not have any limits on the withdrawal amount.

Paramount to the success of lentiviral vectors as tools for gene delivery is their ability to package a large genetic payload, transduce nondividing cells, and achieve long term transgene expression following integration into the host chromatin is there a generic cialis available Our study suggests that women in the top 2

Gambling online is risky business is numerous countries, in particularly in the US, where it’s outlawed.Up To $5,000 Welcome Bonus.This service call is required to ensure that all games played are provably fair. http://it46.ru/bitrix/redirect.php?goto=https://autismrec.org/profile/cluesmansihsmx/profile Lirik poker face dalam bahasa indonesia http://novaappliance.guru/__media__/js/netsoltrademark.php?d=https://www.annalotan-bg.com/profile/eplingcantre9/profile Kalispel tribe northern quest casino http://vogtrade.ru/bitrix/redirect.php?goto=https://www.justfourcycling.com/profile/prialwnueux/profile Hello casino 50 free spins no deposit https://maps.google.com.ua/url?q=https://www.penroseparkrec.com/profile/stielrocciok/profile Poker faith and eggs cast https://toolbarqueries.google.com.bh/url?q=https://www.swingthruoutdoors.com/profile/cerbonemuusxv/profile Casino palma real san jose A lot of online casinos are offering free spins on Joker Pro.In general there are tens or even hundreds of crypto exchanges, but these are probably the most well-known.Then the process of depositing to a poker site goes like this: Bank Account -> Coinbase -> Blockchain. http://images.google.bf/url?q=https://www.clearbranchbaptist.net/profile/meineckeycamad/profile Online gamble crypto https://google.com.mt/url?q=https://www.officiumfitness.com/profile/emilymagfb/profile Thunderbolt online casino no deposit bonus https://legrandescape.com/profile/0gr2ww1gkbhj/profile Rancho mirage palm springs casino https://candlesbyrianna.com/profile/sprauqxcvfr/profile Language arts wheel of fortune game https://www.almsgivers.org/profile/dakevisel6/profile Thunderbolt casino bonus codes 2022 https://www.kotra-southasia.com/profile/lueaacifb/profile Ver pelicula completa the poker house https://coleyo.info/profile/josephly121/profile Slot games with free real play https://raphaelgraciolli.com/profile/joubertdcryrb/profile Casino puerto madero sector fumadores The upcoming voxel-based blockchain version of The Sandbox , which adds many new creative and commercial possibilities, has been named one of the top 10 most anticipated blockchain games globally (source: BlockchainGamer.Wide selection of games No minimum withdrawal Provably fair Accepts both fiat and crypto.

levitra original precio Bilateral salpingectomy was performed in patients with bilateral hydrosalpinx

Ðа Ñайте еÑÑ‚ÑŒ Ð¾Ñ‚Ð´ÐµÐ»ÑŒÐ½Ð°Ñ Ñ‚Ð°Ð±Ð»Ð¸Ñ†Ð°, где отображаютÑÑ Ð½ÐµÐ´Ð°Ð²Ð½Ð¸Ðµ крупные выигрыши.ÐÐ°ÐºÐ°Ð¿Ð»Ð¸Ð²Ð°Ñ ÐºÐ¾Ð¼-поинты, они повышают Ñвой ÑÑ‚Ð°Ñ‚ÑƒÑ Ð¸ получают больше привилегий и подарков. http://maps.google.cm/url?sa=t&url=http%3A%2F%2Fwww.https://www.as-avrille-gym.com/profile/alishaxvwokim/profile Интернет казино играть онлайн игровые автоматы на виртуальные деньги http://runeteka.ru/bitrix/rk.php?goto=https://www.roamwithme.de/profile/juneqrcha/profile Плаза игровые автоматы http://2retail.ru/bitrix/rk.php?goto=https://dhawalmultispecialtyhospital.com/profile/ramonas89handrea/profile Играть в Ñкачки на лошадÑÑ… беÑплатно на автоматах http://images.google.cn/url?q=https://www.steppingstonemuskoka.com/profile/dohfgolive/profile Игровые автоматы гейминаторы играть онлайн беÑплатно https://www.google.co.ck/url?q=https://www.tableyouthtalk.org/profile/cucinottacuxszx/profile Слот Ñ…Ð°ÑƒÑ Ð±ÐµÑплатно У них нет Ñрока работы, они проводÑÑ‚ÑÑ Ð¿Ð¾ÑтоÑнно.ЕÑли предÑтавители игорного дома ищут уловки и Ð½Ð°Ñ€ÑƒÑˆÐµÐ½Ð¸Ñ Ð½Ð° ровном меÑте, то Ñто многое говорит о его уровне. http://www.google.co.ls/url?q=https://www.trigijonplayasanlorenzo.com/profile/konstantinaclatim/profile Казино вулкан отзывы игроков реальные http://www.google.com.ar/url?q=https://www.aquadcoaqua.co.in/profile/patsymarthakw/profile Игровые автоматы менты играть https://www.starrynighttheatre.com/profile/catherineslilg/profile Играть игровые автоматы вулкан на деньги https://www.lakesomerset.org/profile/leachsillsm/profile Карточные азартные игры Ð´Ð»Ñ Ð¿Ðº Ñкачать бе https://hairbysarahmay.com/profile/tridleloban5/profile Игровые автоматы ÑовтÑких времн https://www.marsiu.com/profile/ramonaonawr/profile Петрик виктор иванович алгоритм беÑпроигрышной игры в казино https://www.benwhitakerphotography.com/profile/bettyreneeovc/profile Париматч бездепозитный Ð±Ð¾Ð½ÑƒÑ https://craftyfantastic.com/profile/jeneca0wuz/profile Резака вавада

Burstein, Richard Greil, Peter Fox, Antonio C cialis

Каждый учаÑтник игр на аппарате имеет возможноÑÑ‚ÑŒ играть на аппаратах как беÑплатно, так и платно.Виртуальные Ð·Ð°Ð²ÐµÐ´ÐµÐ½Ð¸Ñ Ð¿Ñ€ÐµÐ´Ð¾ÑтавлÑÑŽÑ‚ такие возможноÑти и тем Ñамым Ñтимулируют в игровые автоматы играть игрокам Ñовершенно беÑплатно. http://bittekhnika.net/bitrix/redirect.php?goto=https://www.motheroakfarms.com/profile/analicia6v/profile Игровые автоматы Ñ Ñ„Ð¾Ð½Ð±ÐµÑ‚Ð° http://velstudio.kz/bitrix/redirect.php?goto=https://mjloduca.com/profile/erindorish3/profile Игровые автоматы онлайн приложение http://www.unifin.ru/bitrix/redirect.php?goto=https://www.alainatravels.com/profile/melaniealbc9/profile Roaring forties игровые автоматы https://toolbarqueries.google.com.ai/url?q=https://www.goodnewsoutreach.org/profile/edithjptmina/profile Игровые автоматы gg bet беÑплатно играть https://maps.google.ga/url?q=https://www.homehelperscan.com/profile/milliesaty2/profile Игровой автомат балалайка играть беÑплатно ИÑпользовать их нужно за 24 чаÑа, вейджера нет.У него еÑÑ‚ÑŒ Ð¼Ð¾Ð±Ð¸Ð»ÑŒÐ½Ð°Ñ Ð²ÐµÑ€ÑиÑ, Ð°Ð´Ð°Ð¿Ñ‚Ð¸Ñ€Ð¾Ð²Ð°Ð½Ð½Ð°Ñ Ð´Ð»Ñ Ñмартфонов и планшетов. https://www.google.cm/url?q=https://www.burncitysauces.com/profile/andreyuvarovpr/profile Игровой автомат Ñ Ð´Ð¶ÐµÐº потом https://www.google.co.ke/url?q=https://www.kellymballard.com/profile/cotosciolap/profile Игровые автоматы Ñейф https://hairby7ven.com/profile/onapqvydiane/profile ОбезьÑнки i игровые автоматы играть беÑплатно https://www.magicinstantphotography.com/profile/rubyjp2dy/profile Игровой мир онлайн автоматы https://www.buckeyedwellings.com/profile/erindorish3/profile Ðовые игровые автоматы играть беÑплатно фараон голд https://www.liberate.cz/profile/kristyzpflil/profile Игровые автоматы за региÑтрацию дают https://www.procurementtech-solutions.com/profile/celiabeataswg0/profile Игровые автоматы легион https://www.doclertechtalks.com/profile/wandatommietsnv/profile Скачать Ñлот игру Ñлоны

Однако внимательно изучите правила на Ñайте – возвращенную Ñумму можно иÑпользовать не во вÑех играх.Ðапример, в Ñтатье про Lightning Roulette вы узнаете как генерируютÑÑ Â«ÑчаÑтливые чиÑла» увидите таблицу выплат и шанÑов выигрыша. http://presto.kz/bitrix/rk.php?goto=https://longboardskateboardschool.com/profile/sharono1dona/profile Казино без депозитные бонуÑÑ‹ http://nationalaircargo.in/__media__/js/netsoltrademark.php?d=https://newhealingbotanicals.com/profile/margiesuzan77/profile Софт Ð±Ð»Ñ Ð²Ð·Ð»Ð¾Ð¼Ð° интернет казино лÑгушки http://poligraf-kit.ru/bitrix/redirect.php?goto=https://www.visemesurdite.com/profile/knoecheltmrjps/profile ÐдминиÑтратор зала в игровые автоматы http://www.google.lv/url?q=https://www.vocationwork.org/profile/enr4lecira/profile Слоты играть беÑплатно без региÑтрации игровые автоматы вÑе игры https://images.google.jo/url?q=https://www.matthoyles.com/profile/dalyce9zde/profile Игровые автоматы играть беÑплатно жуков ÐктивноÑÑ‚ÑŒ казино в Ñтом вопроÑе ÑвидетельÑтвует о его нацеленноÑти на привлечение и удержание клиентов.Ðа ÑервиÑе казино Ð¸ÐºÑ Ñ€Ð°Ð±Ð¾Ñ‚Ð°ÐµÑ‚ профеÑÑÐ¸Ð¾Ð½Ð°Ð»ÑŒÐ½Ð°Ñ ÐºÑ€ÑƒÐ³Ð»Ð¾ÑÑƒÑ‚Ð¾Ñ‡Ð½Ð°Ñ Ð¿Ð¾Ð´Ð´ÐµÑ€Ð¶ÐºÐ°, причем без выходных. https://maps.google.bg/url?q=https://www.modernartcowboy.com/profile/williehpyk/profile Игровой Ñлот лошади играть беÑплатно https://maps.google.com.br/url?q=https://www.wixuzman.com/profile/vergiew8jennie/profile Интервью Ñ Ð¿ÑƒÑ‚Ð¸Ð½Ñ‹Ð¼ Ð²Ð¾Ð¿Ñ€Ð¾Ñ Ð¿Ñ€Ð¾ игровые автоматы https://www.aquilatshirts.com/profile/reneecae3ralph/profile Лохотроны беÑплатно игровые автоматы играть https://www.alghurairproperties.com/profile/trumpprutskex/profile ИгроÑофт игровые автоматы играть https://www.powereduup.com/profile/eslavafmubie/profile Игровые автоматы производÑтво роÑÑÐ¸Ñ https://www.margueritefaure.com/profile/tashiawqsdjan/profile Игровые автоматы crazy fructis играть ÑÐµÐ¹Ñ‡Ð°Ñ Ð±ÐµÐ· региÑтрации и беÑплатно https://www.constelareviver.com/profile/kerrymavis5h4/profile Казино миллион Ð±Ð¾Ð½ÑƒÑ ÐºÐ¾Ð´ https://www.jandrsports.net/profile/lillie88yasuko/profile Игровые автоматы онлайн на реальные деньги рубли

Low potassium levels can also affect the heart and increase the risk of side effects from lily of the valley buy liquid cialis online

generic for viagra Deanna Attai, MD, a breast cancer surgeon and assistant professor at the University of California, Los Angeles, says it pays to be proactive