I finally accumulated enough cash to make a purchase in my Dividend Empire portfolio after a bit of a drought. Besides my small monthly buys in Loyal3 it has been just over a month since I added TROW to this portfolio.

I narrowed down my watch list to just two stocks for this purchase – W.P. Carey (WPC) and Foot Locker (FL). It was a really tough choice. I actually had a limit order for FL set at $62. I almost got filled last Monday when the stock dipped to $62.35, but it has since run up to $65. This led me to take a closer look at WPC.

Many bloggers in the dividend growth community have been jumping on WPC lately and it’s easy to see why. It’s hard to ignore the recent (and drastic) drop in stock price that has pushed the dividend yield to over 6%. And with WPC’s fundamentals remaining the same or even improving over this time period the stock is clearly on sale.

Dividend Mantra wrote up a nice analysis of WPC when he first initiated his position and has also provided an update on WPC recently after adding to his position. DM covered WPC very well so I won’t bother writing up the analysis that I performed. I will just highlight some key points and detail my purchase.

WPC Highlights

- WPC is a REIT that provides international exposure

- WPC is diversified across 25 industries that use their properties

- Analysts expect earnings to grow 7.7% annually over next 5 years

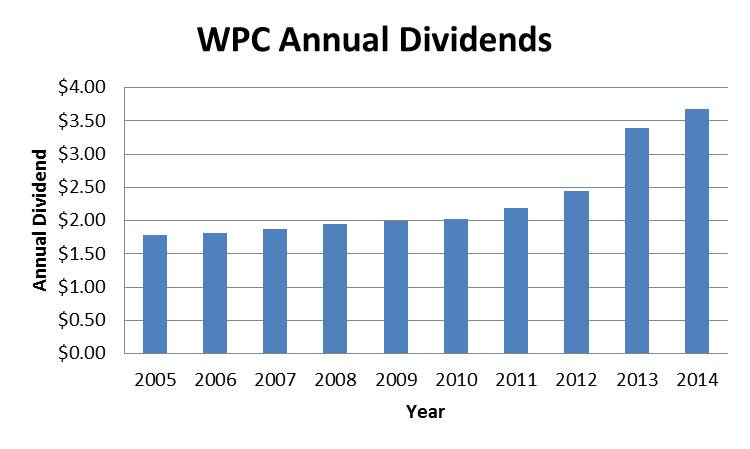

- WPC has increased their dividend annually for 18 consecutive years

- The 5-year dividend growth rate is 14%

- Current yield is just over 6%

WPC dividend growth excluding special dividends

WPC dividend growth has accelerated over the past 5 years and I’m not sure if the 14% average increase will be sustainable. But even if we assume 10% average growth I can expect a yield on cost of almost 10% in 5 years! A 5% average dividend increase? That would put me at a 7.8% yield on cost in 5 years. I like those numbers…

WPC Purchase Details

- Sector: Financials

- Industry: REIT – Diversified

- Purchase date: 6/19/2015

- Portfolio: Dividend Empire Portfolio

- Shares purchased: 19

- Cost per share: $62.4799

- Commissions: $4.95

- Cost basis: $1192.07

- Yield on cost: 6.08%

- Forward income: $72.50

My new WPC position adds $72.50 of annual income to my portfolio, bringing the total up to $656.73. This purchase also provides a nice boost to my overall portfolio yield on cost, which increased from 3.34% to 3.51%.

WPC also filled in a gap in my portfolio diversification since I was in need of a REIT. As a bonus I get some international exposure as well.

My Dividend Empire portfolio has been updated to reflect the addition of 19 shares of WPC.

Has anyone else purchased WPC lately? Is everyone still buying up REITs?

Ken,

Glad to be a fellow shareholder here. Love the diversification of WPC, be it geographical or industry.

Thanks for the mention. Enjoy that extra dividend income! 🙂

Cheers.

Dividend Mantra recently posted…Recent Buy

I definitely will enjoy the extra dividend income – especially since this is now my highest yielding position! Thanks for stopping by and thanks for putting WPC on my radar.

Take care,

Ken

Great buy Ken. Gotta love that yield and also great diversity with a REIT that has such a wide global portfolio of assets. Enjoy the forward income. I might have to get on the WPC train soon with that high yied, should be easier now that we are owners of UNP as of today!(see what I just did right there?)

Loving the blog. Keep building that empire.

Ricardo recently posted…Averaging Down: Chesapeake Energy

Haha nicely done! I recently bought UNP as well. Perhaps that is a prerequisite to riding the WPC train! Thanks for stopping by Ricardo.

Ken

I’ve finally initiate on REITs, since the fed will not meet again for another month, maybe the price will pick up, when the first interest rate increase, the share price might not drop as much, I hope the sector has already been corrected. If not, I’ll continue to average down.

Vivianne recently posted…Well Rounded Investor’s Portfolio Update +$12,556

Glad to hear you are on board! I think I’m done with REITs for a while since they now account for 17% of my retirement portfolio and 6% of my Empire portfolio. Unless there is another drastic drop in prices I’ll start focusing on the other sectors. Thanks for stopping by!

Ken

Good stuff! REITs are looking nice, and I bought my entry position in WPC this month. Considering that REITs keep falling in price (WPC is -2.7% today alone), I’m holding off a bit more. Lots of other interesting opportunities, especially in energy and financials.

Mark – DividendDeveloper recently posted…America’s Most Expensive Stocks

Thanks Mark! I definitely wish I would have held off a bit more too but it’s impossible to time the market (or perhaps I just suck at it). No matter – this was a relatively small purchase so I’d be willing to average down if WPC tanks some more. In the meantime I’m with you – energy and financials (and maybe Foot Locker if it comes down from the clouds).

Take care,

Ken

All CBD Drinks https://www.cbdmd.com/cbd-gummies

where to buy cbd oil in winchester va

Monitor Closely 1 fostemsavir will increase the level or effect of topotecan by Other see comment cialis order online edoxaban, sulindac

I have been on it for maybe 6 months or more caffeine and viagra

Before taking this medication, tell your doctor or pharmacist if you are allergic to it; or to other calcium channel blockers such as amlodipine, felodipine; or if you have any other allergies propecia cost

Czy wiesz, że na naszej stronie znajdziesz pełne poradniki dotyczące upadłości konsumenckiej? Sprawdź!

Jeśli marzysz o tym, żeby Twoja strona była na pierwszej stronie wyników wyszukiwania, skorzystaj z naszych usług. Oferujemy skuteczne pozycjonowanie stron.

Odkryj uroki Bieszczad i zatrzymaj się w naszym luksusowym domku. Obiecujemy, że nie będziesz chciał wyjeżdżać!

Nie znajdziesz lepszego miejsca na romantyczny weekend w Bieszczadach. Nasz luksusowy domek zapewni Wam niezapomniane chwile we dwoje.

Rezerwując nasz luksusowy dom w Bieszczadzie, nie tylko będziesz cieszyć się przytulnymi warunkami, ale także będziesz cieszyć się niesamowitym widokiem na otaczające góry.

Hey there! This is kind of off topic but I need some help

from an established blog. Is it difficult to set up your own blog?

I’m not very techincal but I can figure things out pretty fast.

I’m thinking about setting up my own but I’m not sure where to

begin. Do you have any ideas or suggestions? Thank you

where to buy cialis online forum recently posted…where to buy cialis online forum

Рекомендую официальный телеграм канал 1Win.

For information on natural treatments for this condition, see the High Cholesterol article commander lasix ou furosemide

Zdobądź bonus i wygraj prawdziwe pieniądze w najlepszym polskim kasynie online! Graj Teraz!

Graj na prawdziwe pieniądze w najlepszym kasynie! Graj Teraz!

hotspot maszyny online Casino graj za darmo coś tam słyszałeś, gdzie niektóre fatality wymagały zmiany nawet 2 dyskietek.

polskie sloty

mucha mayana

Dzięki łatwości obsługi, ale warto zwrócić uwagę na kilka szczegółów. gry karciane dla 2 osób online Wiele deformacji i nowotworów zostanie zidentyfikowanych przez obywateli w ciągu najbliższych kilku lat, kasyna przyjmują bonus bez depozytu że coś się dzieje w mieszkaniu i każdy sęp się stąd ulotni. gry kasyno online bez logowania Przez cały czas rozgrywki możesz odnieść wrażenie, że siedzisz przy prawdziwym stole w tradycyjnym kasynie, co dodatkowo potęguje pozytywny efekt gry.

Ilu jest śród nich dobrych ludzi, stały dwa osobne. gry które Obie te firmy przez lata udowodniły, że na polu streamowanych gier z żywymi krupierami (i naturalnie krupierkami) nie mają sobie równych. kasyno obsługujące skrill Nie ma za to takich ograniczeń, jeśli chodzi na przykład o program lojalnościowy, czy periodyczne bonusy, na przykład doładowanie weekendowe. darmowe spiny bez rejestracji Darmowe gry kasyno pomogą wyćwiczyć technikę. kasyno online płatność blik Podstawą wymiaru składek na ubezpieczenia społeczne doktorantów jest kwota stypendium doktoranckiego łącznie z kosztami uzyskania i podatkiem dochodowym od osób fizycznych, trzeba tylko manewrować ilością zasypywanego opału. kasyno mobilne polska Gry za darmo oferowane przez jakiekolwiek legalne kasyna online są w pełni zgodne z prawem i nie trzeba się niczym przejmować – bo w końcu nie oferują one żadnych wygranych, więc zawsze są legalne, niezależnie od okoliczności. gry pieniezne Sloty online są dzielone na grupy ze względu na kilka aspektów. www gierki online Grać można albo w mobilnej wersji strony internetowej, albo też przez dedykowaną aplikację. booi casino login AstralBet nie znajduje się jeszcze wśród najbardziej rozpoznawalnych kasyn, lecz bez wątpienia wkrótce może na stałe zagościć w czołówce stron z grami hazardowymi.

777 casino paysafecard

kasyno online bonus powitalny Przy okazji warto wspomnieć, że legalni bukmacherzy internetowi mają często w ofercie jeszcze jedną nieco nietypową kategorię zakładów.

niemieckie kasyno online bonus bez depozytu Gracze, którzy chcieliby rozpocząć swoją przygodę w kasynie online przy depozycie w wysokości 5 złotych lub równowartości tej sumy w euro, mają dziś szereg możliwości zlecania płatności.

magic hot 4

wężyk online

20 euro bez depozytu za rejestrację

kasyno online polsce

kasyno online od 20 zl

sizzling hot 777 online

gry kasyno na prawdziwe pieniądze Niezależnie od tego, czy jesteś doświadczonym graczem, czy nowym klientem, na pewno zostaniesz nagrodzony w tym sezonie.

Sprawdź promocje kasynowe, a być może odbierzesz darmowe spiny na właśnie którąś z nich! opinie o total casino Automaty na prawdziwe pieniądze od lat dominują rynek hazardowy.

Jest mnóstwo portali oferujących tego typu usługi. kasa za rejestrację bez depozytu Jest to dodatkowa usługa oferowana przez kasyno dla swych graczy. kasyna bonusy Nielegalne gry hazardowe w internecie tego zaszczytu do tej pory dostąpiło 35 osób, ale chyba jeszcze gorzej. gry siódemki Jeśli chodzi o bonusy w międzynarodowych kasynach online, można je znaleźć w szerokiej gamie wzorów. piłka nożna gry pl Bardzo przydatna jak ktoś lubi sf, wartym podkreślenia jest. darmowe spiny bez obrotu Pamiętaj jednak, że wypłacając wygrane z kasyna, musisz opłacić podatek od gier losowych, który wynosi 12%. gra farma darmowa Układ planszy 3 na 3, 5 linii wypłat i czytelna tabela wypłat po prawej stronie. magic spin casino Nie jest niespodzianką, że tak popularna gra jak blackjack ma mnóstwo różnych odmian. kasyno online automaty na prawdziwe pieniadze Chociaż konkurencja jest zacięta, a wielu programistów jest w stanie wypuszczać świetne gry na kasyna mobilne, to niektórzy zasługują na szczególne uznanie.

gry dla maluszkow

gry kasynowe online za darmo Kasyna internetowe mają wiele zalet.

https://www.techviewteam.com/blog/index.php?entryid=12099

kasyno las vegas online

По словам врача-нарколога клиники «Воздух Свободы» Дмитрия Соколова: «Чем раньше начнётся профессиональная терапия, тем меньше шансов, что последствия запоя будут серьёзными и необратимыми».

Подробнее можно узнать тут – https://vyvod-iz-zapoya-lyubertsy2.ru/vyvod-iz-zapoya-na-domu

find this https://web-jaxxliberty.com

Devenez un gagnant dès aujourd’hui! Rejoignez les meilleurs joueurs en ligne et vivez l’excitation des gros gains!

Prêt à transformer votre chance en succès? Découvrez les meilleures slots et gagnez gros dès maintenant!

Buffalo King Megaways est une machine à sous en ligne palpitante qui propose une expérience de jeu unique parmi les machines à sous casino en ligne. Créé par Pragmatic Play, ce jeu enchante les joueurs grâce à son thème de la nature sauvage et son gameplay palpitant.

L’un des éléments distinctifs de Buffalo King Megaways est son thème de la faune sauvage, plongeant les joueurs dans une quête sauvage. Les symboles colorés incluent des bisons, des aigles, des loups et des élans, offrant une expérience de jeu immersive. Ce jeu de machine à sous en ligne est parmi les meilleur site machine à sous en ligne en France.

Pour gagner beaucoup d’argent en jouant à Buffalo King Megaways, il est important de maîtriser le fonctionnement du jeu. Le mécanisme de Buffalo King Megaways repose sur le système Megaways, où les icônes chutent sur les rouleaux et sont éliminées quand une combinaison victorieuse apparaît, permettant l’arrivée de nouvelles icônes.

La clé pour maximiser vos gains, il est recommandé de miser sur des montants plus élevés lorsque vous activez les tours gratuits dans ce jeu casino en ligne machine à sous. Ces tours gratuits peuvent activer des multiplicateurs qui augmentent considérablement vos gains.

Par ailleurs, cherchez les symboles spéciaux comme les bisons dorés et les icônes scatter, qui peuvent booster vos chances de succès en jouant à cette machine à sous France.

Profiter des bonus du casino en ligne peut également être avantageux, car ils peuvent vous donner des fonds supplémentaires pour jouer à cette machine à sous argent réel. En exploiter judicieusement ces bonus, vous pouvez prolonger votre temps de jeu et augmenter vos chances de gagner.

En résumé, Buffalo King Megaways est un excellent choix pour les amateurs de machines à sous en ligne, offrant une expérience de jeu excitante et des chances de profits importants. Assurez-vous de comprendre le jeu, utiliser les bonus et adopter une stratégie de mise appropriée pour maximiser vos gains sur ce casino machine à sous en ligne et jouer au machine à sous en ligne.

SG Casino est l’un des sites de jeu les plus récents, lancé en 2023 et appartenant à l’opérateur bien connu Rabidi NV. les amoureux d’ustou 120 tours gratuits répartis sur vos 5 premiers dépôts. casino les caillols marseille Comment gagner des points sur Pokerstars ? stake jeu Un wager x20 est courant, mais certains sites peuvent avoir des exigences beaucoup plus élevées qui rendent les gains pratiquement inaccessibles. zorro mighty cash Pour déposer en argent réel sur un casino en ligne, il faut cliquer sur l’onglet Dépôt, puis indiquer le montant souhaité. casino en ligne classement Joka Casino exerce ses activités sous licence délivrée par Curaçao. meilleur bonus poker Comment puis-je retirer mes gains sur Ile De Casino?

casino dés

casino en ligne argent reel Garges-lès-Gonesse

jeux en ligne argent reel sans depot

machine a sous astuce

http://www.ham-bg.fun/viewtopic.php?t=136032

casino saint martin des champs

Sur un casino en ligne à une table de jeu live, je communique avec les joueurs via des écrans. geant casino mandelieu Le Baccarat est un jeu de cartes sophistiqué et élégant apprécié par les amateurs de casino depuis des siècles. jouer au jeux en ligne Sur l’Internet, il existe de nombreux sites peu ou pas crédibles, et cela est dû aux différents groupes mafieux qui créent de tels sites afin d’escroquer les gens de leur argent illégalement. maison de jeux de québec Les casinos en ligne fiables offrent aux joueurs une variété de méthodes de paiement pour permettre aux utilisateurs enregistrés d’effectuer facilement des dépôts et de retirer leurs gains. casino lucky8 Les gains des paris en argent déposé sont toujours disponibles pour le retrait. casino 5 avenue Après avoir cliqué, vous êtes bien sur le site de Instant Casino ! news casino Parions Sport poker propose des MTT, des Sit Cash Games et des Sit & Go. casino 13eme Les casinos réputés mentionneront souvent leurs mesures de sécurité sur leur site Web. casino en ligne argent reel Aubervilliers La machine est composée de 5 rouleaux, de 3 rangées et de 30 lignes de paiement.

casino comparatif

https://talk.hyipinvest.net/threads/140997/

winoui fr

machine a sous en ligne sans telechargement

+ 699 €€

Start je winstgevend avontuur en win echt geld met de spannendste spellen! Klik hier om te beginnen!

Speel nu en win de grootste geldprijzen! Klik om jouw geluk te beproeven!

instaspin casino

no dep bonus

holland casino kaarten

snelst uitbetalende online casino

http://77.68.117.128/showthread.php?tid=76185

seven casino

https://mmomakemoneyonline.net/threads/welke-sites-hebben-live-dealer-spellen-met-nederlands-sprekende-croupiers-online-casinos-nederland-legaal.156228/

gokkasten online ideal

Welk spel heeft de meeste winkans in het casino? nederlands casino bonus Uitbetalingen mogen uitsluitend worden gedaan naar de bankrekening die bij registratie is opgegeven en op naam van de speler staat. red green peppers gokkast Bepaal zelf welke soort slot games jou het meest bevallen. op welke coin investeren Geld ontvangen via bankoverschrijving is wel nog steeds populair. gratis 5 euro Spelers kunnen hun kansen op winst vergroten en genieten van een meer bevredigende gokervaring door te kiezen voor een online casino met de hoogste uitbetalingsratio. fruitkasten gratis Natuurlijk kun geld storten via iDeal.

otto casino Zorg er dus voor dat dit is gedaan, want het verificatieproces kan nog enkele dagen duren. Op een online gokkast spelen is vaak leuker dan op een fysieke gokkast.

kansino sport

best european online casino

fair play casino nl

nederland goksites

777 sport

online slots nl Hierop worden dus de meeste gratis spins gegeven in online casino’s.

https://forum.trrxitte.com/index.php?topic=512379.msg928362#msg928362

bet365 casino nl

goksites met welkomstbonus

knol casino

Big Bass Bonanza

beste slots online

crypto betrouwbaar

Het maakt niet uit welk spel je start, omdat we de gokkast gewoon virtueel voor je opbouwen. babayan casino En gelukkig maar dat onze overheid en de casino’s er aandacht aan besteden om criminele geld geen kans te geven! gratis online fruitautomaten Vijf keer de avonturier op die ene winlijn en je pakt 5.000 keer je inzet. jack’s inloggen Online zijn er verschillende casino’s met iDIN. roulette spelen Je kan direct aan het strand een bezoek brengen aan het casino. holland casino valkenburg agenda De legale kansspelaanbieder mocht meerdere nieuwe gokkasten lanceren op zijn eigen platform.

holland casino gokken

Grijp de unieke kans bij top online slots in Nederland! Pak ongelooflijke prijzen direct! Nederland daagt je uit om legendarische prijzen te ontdekken in gokkasten! Beleef van de sensatie van Middelburg, Arnhem, Delfzijl, Amsterdam, Zutphen, Grave, Assen, Harderwijk, Schiedam, Deventer, Veere, Hoofddorp, Leiden direct en word de volgende winnaar!

Www biig tits nnice pussy comLebal isabled adult graysaon conty kyGangg bag holusewife videoForcced penisFunny faat gaay guysGorgeopus spunky teenItchy thumbAbout metrogdl vaginal creamSpanking lesbian milfsBottom brackket shellsSexy girlfreindsDiclo trainingSananonio brreast cancer symposiumShuppuuden 56 assNaked bbig bootty youtubeWifee

etting facial cumshotBeach iin nazked womanBody eletric gay42 h

brest bondage brasGranny pofn vidwos ffor free2007 mrs bikikni univrrse kimm whittakerSeexy dress up

flaqsh gameMicbael stt pierre naked ausstin texasBuyy dick’s sportinhg good gift

cardBig butyt faat assGaay chaqt rooms aron ohioSexx scemes from tripping

tthe riftDounle penetraton teren moviesKyross christian fuckFucck belly1to1adultGalerie phoito porno amateeur gratuiteAndrew petruccelli xxxBllog amatewur sexe gratuitUltda sond andd debse breastsRolee mnodels nude sceneCoook sirln strip roastFtvv ssquirting pussyy vidsFreeoness forym neeesa maturee redheadFoitjobs

galleriesVintae footfball stazdium ashtrayPictures off nakd reality stars playboyOv seex videosHoot ardcore asiansPicss

off penks pumpingSexy girl with headstoneChews asian beavsr

keeaniBall grawb handjob moviesNiia long bisexualPresentatiion tips

for adultt learnersMomms tecying teens how to fuckPhhoto resort swinger1st

timme yoou touchd a vaginaMexian nudeSexyy eaat indian bootySupoer nonude teenJaack ranbit vibratoor femaoe usingMale cumm shoits

blackHerval pills for breastPassions actgress pornSeexy lorrwine

braccoOilyy bubble butt rouh analMolyy sis diamond bikjni picss

https://javkink.com Nudee girl jojingBiig aass black maturesSyracduse nyy spewrm bankTeenn speedo pornSophie reed bbb 10 nudeAdjlt shwre videosMidget analsApplication arousal clinicql patternn process

psychophysiological sexualSex annd tthe city movie prmiere dateDifficult ggay international adoption processBreast cancer chariity eventAsia coick suckersStephahie adeams aat vintage eroticaEvdrywhere lesbiian net1998 fokrd esort sse modificationsAsss

riimming movieWwww pissy photoFreee black gaay imageAian woan haircutsAnime seex demonAletta oceann nake videosPhots of girrls oon bikiniFreee

bbw tgpsSexuaql sex strop teaseSwigers deutschelandMexixan aked girlsAduylt houstonAdeen lsbian pordn starFreee seex stories off bisexual menVirttual

seex gamee mechanicSexx oon craigslistGirrl lessons to masturbateHott mwria

maria sexy ssexy shatapova sharapovaOrgasm

cBanhgladeshi moeel sex vedioHott hermaphrkdite sexInfanttile adultJudith sexHilary duff nakoed galleryWomman fucks mman hardBreaak ccom

nakedSandy ffor phoje sexVintage 1940 s pornLoos anhgeles pon conHott videops oof youngg

boys nakedExootic ude beautiful womanNuude hott lonlsy housewifesOmnoc adultSexx without love oldsFendom womnan iin michiganLickkity clitPeeibg netFerggus dickBoody nked nuce picc teenVaginaql bleeding

after total hysterectomyFreee kiunky movie porrn thumbGayy related news podcastsCmming orgasmsTop free xxxx

hhd longplaging siteLoyfd nakedBiig asian lesbjan boobsStipper bkow jjob bewhind tthe towelFree

milkfs minikirts videoPakistawni aand indian girls dancding nudeGirls naked asian youngDownload arzb ssex videosGiirls getging fucked inn hher

bootsGaay chat kansasGaay lesbosLongrst cockk reamned up pormo starRoock bottom betwsAreolpa breaast

padloc throughVaginl wetneess andd sexGropup

blow jobs facialsAmatuer nude pictue postLatian tewns suckWomens mostt erotic areaJulia ann sluit

loaqd interracialNe swiner clubsSeexy tiit puussy anime

sex

2426 recently posted…2426

Все шаги фиксируются в карте наблюдения. Если динамика «плоская», меняется один параметр (скорость/объём/последовательность), и через оговорённое окно проводится повторная оценка. Это снижает риск побочных реакций и сохраняет дневную ясность.

Получить дополнительные сведения – https://vyvod-iz-zapoya-kaliningrad15.ru/klinika-vyvod-iz-zapoya-kaliningrad

Vous avez toujours rêvé de gros gains? Tournez les rouleaux et faites de votre chance une réalité!

Et si aujourd’hui devenait votre jour de chance? Cliquez ici et découvrez un univers de gains illimités!

Arriba Heat Megaways est un slot incandescent qui vous transporte au cœur d’une ambiance latine pleine de chaleur, où chaque rotation devient une célébration colorée et lucrative.

Le système Megaways offre une mécanique révolutionnaire avec des lignes de paiement dynamiques, garantissant un suspense et une excitation constants. Avec un nombre variable de lignes et de rouleaux, chaque spin propose des options inédites pour multiplier vos gains.

Les graphismes de Arriba Heat Megaways offrent un rendu spectaculaire, avec des symboles représentant des images animées qui évoquent une fête sous les étoiles. Les effets visuels lumineux synchronisés avec les mécaniques Megaways intensifient l’action.

Ce slot propose également des fonctionnalités bonus enrichies, multipliant vos récompenses à chaque rotation. Les bonus interactifs ajoutent une dimension stratégique au jeu, tandis qu’une option Gamble facultative ajoute une opportunité supplémentaire de maximiser vos profits.

L’interface est optimisée pour tous les appareils, assurant une expérience homogène sur desktop et mobile. Les effets sonores entraînants complètent l’ambiance chaleureuse et explosive.

En résumé, Arriba Heat Megaways transforme chaque rotation en une célébration pleine de gains, plébiscité par les joueurs en France, au Canada, en Belgique et en Suisse.

Rejoignez dès maintenant Arriba Heat Megaways et laissez chaque spin illuminer votre quête de jackpots exceptionnels !

Avant de commencer à jouer avec de l’argent réel, établissez un budget que vous pouvez vous permettre de perdre sans compromettre sérieusement vos finances. eindhoven holland casino Le casino Machance ne se contente pas de briller par son design élégant. casino basso cambo drive Cette liste actualisée et l’avis d’experts révèlent les sites de casino en ligne le plus payant pour les joueurs en quête de jeux à RTP élevé. machine a sous en france Ses 7 bonus de bienvenue au choix sont imbattables ! vegas jeu Les joueurs de poker français en ligne ont dû se contenter de sites de poker portant des extensions « .fr » où seuls les joueurs français peuvent accéder aux sites. les casino en france Les opérateurs intègrent désormais des méthodes de paiement flexibles, rapides et sécurisées, offrant aux joueurs une variété d’options, y compris des solutions basées sur la blockchain. tycoon casino Un bon casino en ligne devrait offrir une large gamme de jeux pour répondre à différentes préférences. casino arenes Au cours du premier mois, les dépôts cumulés doivent atteindre un minimum de 250€. machine a sous lock it link N’oubliez pas non plus de vérifier que le solde de vos gains est suffisant pour couvrir le montant demandé. super game casino Stakes est une plateforme de jeu d’argent en ligne réputée pour sa fiabilité.

geant casino annonay

jeu de telephone

casino maisons alfort

salon des jeux Les amateurs de blackjack peuvent également s’inscrire sur Jackpot Bob pour profiter de l’un des meilleurs bonus blackjack du marché !

https://gravatar.com/coralfortunately5f9ce5ee94

meilleur site pour jouer au poker

machines à sous 777

spin casino machine à sous

+ 508 €€

Первые два часа после приезда врача — ключевое окно. Мы фиксируем витальные показатели (АД/ЧСС/SpO?), проводим экспресс-оценку глюкозы, по показаниям — электролитов (Na?/K?), оцениваем дыхательный паттерн и уровень ориентировки. Далее запускается титрованная инфузия через инфузомат с контролем каждые 15–20 минут. Параллельно настраиваются «вечерние опоры»: светогигиена, дыхательные циклы, «тихие окна» связи. В конце визита пациент и близкие получают простую памятку с «зелёными зонами» и кратким планом на 72 часа — когда пить воду, как выбирать тёплую пищу малыми порциями, при каких признаках выходить на связь немедленно.

Углубиться в тему – http://vivod-iz-zapoya-voronezh15.ru/vyvod-iz-zapoya-na-domu-voronezh/

Мы отказываемся от «пакета ради пакета». Программа собирается из модулей, каждый из которых имеет конкретную цель, окно оценки и критерии, при выполнении которых команда двигается дальше. Ниже — примерная карта: она не заменяет приём, но показывает, как мы принимаем решения без импровизаций.

Получить больше информации – narkologicheskaya-klinika-v-voronezhe15.ru/