In my last post I introduced my dividend growth stock ranking system, a stock screen that I run on David Fish’s CCC list that pulls out what I believe to be the best dividend growth stocks each month.

I ran the screen on the May CCC list and pulled out several high quality dividend growth stocks. I narrowed the list down to about 30 stocks that looked promising and researched them in detail. The winner from this list, and the stock that I recently purchased for my Dividend Empire portfolio, was T Rowe Price (TROW).

Just because TROW was the stock that I selected doesn’t mean it was the only one worth purchasing. There were plenty of great choices that scored high in the screen. One of these stocks, and the subject of this post, is Cummins Inc (CMI).

CMI scored a 7.75 / 10 in the original screen and was recently increased to 8.25 / 10 after taking a closer look at the stock. Thorough analysis of the CMI dividend suggests even a higher score but I don’t want to start breaking the rules.

CMI has shown incredible dividend growth, strong financial health, and I think now is a great time to purchase Cummins for your dividend growth portfolio.

CMI Dividend Stock Analysis

Here I will present my case for purchasing Cummins. The sections below will cover the company overview, the ranking screen results and a detailed drill-down into each ranking category.

CMI Company Overview

Sector / Industry: Industrial Goods / Diversified Machinery

From the Cummins Inc Investor Relations website:

About Cummins Inc., a global power leader, is a corporation of complementary business units that design, manufacture, distribute and service diesel and natural gas engines and related technologies, including fuel systems, controls, air handling, filtration, emission solutions and electrical power generation systems.

Cummins Inc got it’s start back in 1919 when Clessie Lyle Cummins founded the Cummins Engine Company in Columbus, Indiana. Cummins started building engines at age 11 and helped Ray Harroun win the first Indianapolis 500 in 1911 by making improvements to his engine. J. Irwin Miller later became general manager and helped lead the company to be the international powerhouse that it is today. Cummins currently employs over 50,000 people and serves customers in approximately 190 countries.

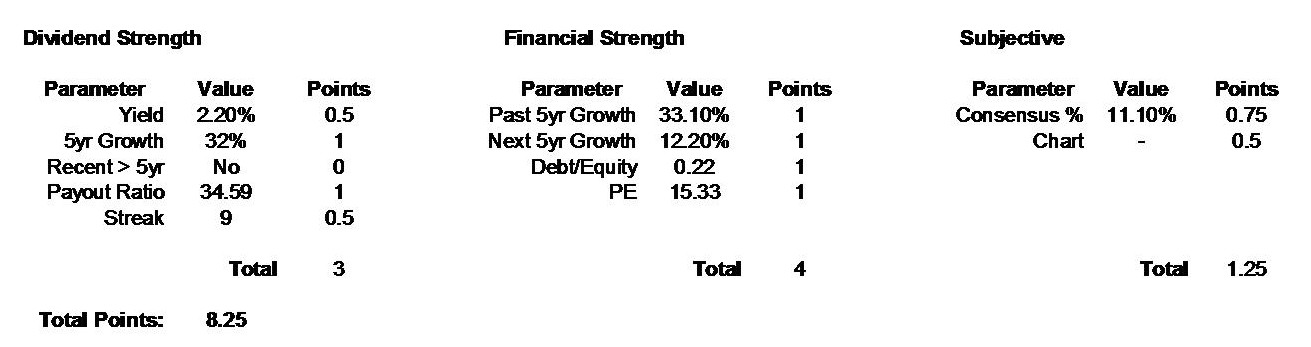

CMI Ranking System Results (5/22/15)

CMI received a score of 8.25 out of 10 in the May 2015 CCC dividend growth stock screen. For detailed descriptions of all categories and parameters please read my original dividend growth stock ranking system post. Receiving a high score in the screen is great, but all of this data needs to be confirmed and the stock needs to be studied in greater detail. Let’s dig a little deeper into each of these categories…

CMI Dividend Strength

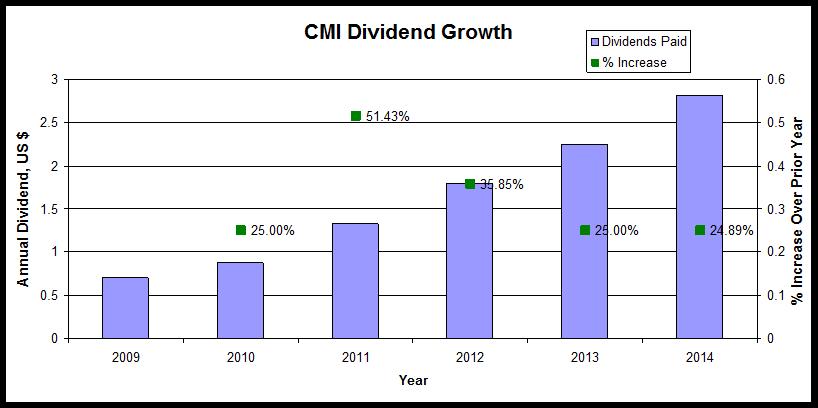

CMI received 3 points out of a possible 4.5 in the dividend strength category, getting docked in the yield, recent>5yr (acceleration) and streak parameters. CMI sports a dividend yield of 2.2% which isn’t great but also not horrible. Add the 32% average CMI dividend growth over the past five years to the equation and the current yield is more than acceptable.

In fact, if CMI was purchased today and that dividend growth rate was maintained over the next 5 years, the yield on cost would be a massive 8.8%!! Using a more conservative 25% average growth, which CMI has produced the last 2 years, our yield on cost would still be a very respectable 6.7% in 5 years. For this reason I am willing to overlook CMI’s relatively low dividend yield.

One of the other parameters where Cummins was penalized was recent > 5yr growth. This parameter is a measure of the dividend’s acceleration, not just the average growth. If the most recent increase is greater than the 5-year average increase, perhaps the company is ramping up it’s dividend increases. CMI did not meet this requirement and therefore received 0 points. This really isn’t fair, however, because 32% dividend growth is a very high bar and I think any dividend growth investor would have been happy with the recent 25% increase that CMI dished out to shareholders in 2014.

Finally, CMI was dinged 0.5 points in the dividend streak parameter. Stocks with a 25 year consecutive dividend increase streak are awarded a full point in this category. CMI has increased their dividend for 9 consecutive years which definitely shows some commitment, but not the likes of the 25 year dividend champions.

One thing I do like about Cummins recent history is that they have managed to increase their dividend during difficult times. Cummins earnings dropped in 2010, 2013 and 2014 but they still managed to raise their dividend in each of those years.

In addition to all of the positives mentioned above, the timing seems to be perfect right now if we consider CMI’s dividend increase history. All of CMI’s recent dividend increases have occurred in August, meaning that we will likely see another increase announced next quarter. If this is true and the increase is another 25%, our yield on cost (if purchased now) would receive an instant boost to 2.75%.

In summary, while CMI received 3/4.5 points in the dividend strength category, this number is somewhat misleading. The low yield is not an issue due to the excellent dividend growth, the lack of dividend acceleration is understandable given the high growth rate, and a 9 year streak of dividend increases ain’t too bad.

CMI Financial Strength

Not much to say here since Cummins received a perfect 4/4 score in the financial strength category. They have averaged 33% earnings growth over the past 5 years. Although this growth has slowed a bit in recent years analysts expect 12% annual growth over the next five years. Cummins has very little debt, with a debt to equity ratio of just 0.22 and their PE ratio is a very reasonable 15.33.

To be fair, I would like to add that CMI’s earnings growth lags a bit compared to it’s peers and the PE is much higher than the industry average of 8.4 (data from Nasdaq.com). This is one of the few faults I could find in this stock.

Overall, Cummins financials are strong and even though the PE is a bit high I think CMI is still a great long term dividend growth stock.

Subjective Analysis

Cummins received 1.25 points out of a possible 1.5 in the subjective category. Out of 18 analysts covering CMI, 11 are recommending a strong buy and 7 give a hold recommendation with an average consensus price target of $157. This represents an 11% increase over the current stock price. In my ranking system, I use the average and standard deviation of the stocks that make it to the subjective analysis category to assign a point value between 0 and 1. In this group of stocks, 11% was good enough to receive 0.75 points.

I also performed a discounted cash flow analysis on Cummins to provide a second fair value estimate. This analysis was calculated at gurufocus.com using 9.33 EPS, 10% growth over 10 years, 4% terminal growth and a discount rate of 10%. Using these parameters, the fair value estimate for CMI is $162.73, in line with analysts estimates.

Finally, the chart for Cummins looks decent. This parameter is obviously the most subjective and therefore is only worth 0.5 points. CMI recently broke through the $140 resistance level (which now becomes support). After reaching a high of $143.40 CMI bounced off of $140, confirming the support level.

Chart from TradeKing.com

Although this is the least important parameter, it is nice to know that there is a potential floor underneath my purchase price and this helps differentiate between stocks with similar scores.

Summary

CMI appears to be an excellent dividend growth stock to add to my portfolio. It scored 8.25 points out of 10 in my dividend growth stock ranking screen and looks even better with detailed analysis. CMI’s dividend growth rate is phenomenal, the company seems very healthy and continues to grow earnings, the fair value estimates provide some margin of safety and it is likely that CMI will raise their dividend next quarter.

What are your thoughts on CMI? Do you own CMI or are you planning on purchasing CMI?

Disclosure: Long TROW. I do not own CMI stock but I might initiate a position in the next month.

Nice Analysis, I myself am looking into CMI as the price as dipped so low for a quality stock such as this. I am expecting it to dip below 100 pretty soon which I will pounce on, but have a buy price at anything under 110.

-Dividendcouple

Thank you Bryce. Unfortunately I got in a bit too early but CMI is definitely a keeper. If we do get a dip around 100 I will definitely double down.

Take care,

Ken

Завод-производитель «М-Строп» поставляет механизмы и комплектующие для подъема тяжелых и габаритных грузов в Беларуси. Компания обеспечивает надежными канатными и текстильными стропами, стяжными ремнями, а также звеньями, крюками и другими элементами, необходимыми для подъема грузов. Предлагаемую продукцию применяют в своей работе строительные компании и промышленные предприятия в Гомеле, а также других регионах Беларуси. На сайте https://m-strop.by/ (стяжки для крепления груза недорого ) можно ознакомиться с ассортиментом строп и оставить заявку для оформления заказа.

Среди важных преимуществ сотрудничества с «М-Строп» стоит выделить:

– Собственное производство. Компания применяет передовые технологии и собственные оригинальные наработки, что позволяет гарантировать качество получаемой продукции и обеспечивать заказчиков большими объемами.

– Большой ассортимент грузоподъемных механизмов. Завод производит различные виды строп – текстильные, канатные, цепные, а также стяжные ремни, цепную таль, буксировочные ремни и комплектующие для грузоподъемных механизмов.

– Наличие всех позиций на складе. Продукция производится в Беларуси с применением специализированного оборудования, что позволяет удовлетворить запросы клиентов без длительного ожидания.

– Оперативная доставка. Товары доставляются в Гомель и другие города Беларуси собственным транспортом компании. Возможна доставка по России и СНГ.

– Выгодные предложения для оптовых заказчиков. Постоянные и оптовые клиенты получают скидки.

Предлагаемое грузоподъемное оборудование по уровню качества и надежности удовлетворяет запросы самых требовательных клиентов. Чтобы уточнить детали сотрудничества, рассчитать стоимость заказа и сроки выполнения, обращайтесь к менеджеру по номерам, указанным на сайте.

Избавиться от долговых обязательств, закрыть непосильные кредиты и получить шанс на свободную жизнь поможет процедура банкротства. Если хотите законно списать все долги по кредитам, распискам, услугам ЖКХ, стоит обратиться к юристам компании «АВ ЗАЩИТА», которые специализируются на банкротстве. Ваши проблемы будет решать команда опытных юристов, аудиторов, бухгалтеров, регистраторов, которые на протяжении 5 лет предоставляют услуги жителям Волгограда. Оставляйте на сайте https://банкротство34.рф/ (банкротство физических лиц под ключ цена отзывы ) заявку, чтобы получить бесплатную консультацию специалиста и сделать первый шаг к решению проблемы.

Услуги компании «АВ ЗАЩИТА» включают помощь в получении банкротства юридическим и физическим лицам напрямую от арбитражного управляющего. Специалисты индивидуально рассматривают каждую ситуацию, гарантируют полную конфиденциальность, помогают полностью списать долги за фиксированную оплату.

Сотрудничество с компанией «АВ ЗАЩИТА» включает несколько этапов:

– оформление заявки – достаточно позвонить по указанному на сайте номеру или отправить заявку с контактными данными, чтобы обратиться за помощью;

– анализ документов – специалист назначит встречу в удобное для клиента время, где детально разберет и проанализирует кредитные договора, долговые расписки и другие документы, которые относятся к делу;

– подготовка документации – юрист берет на себя все обязательства по оформлению документов, которые потребуются для получения банкротства;

– контроль и сопровождение – на всех этапах сотрудничества сотрудники компании «АВ ЗАЩИТА» предоставляют квалифицированную юридическую помощь и представляют интересы клиента в суде.

На счету компании больше 50 успешных дел по списанию долга. Если есть сомнения, можно просмотреть отзывы от клиентов, которые размещены на сайте.

«РусКондиционер» – поставщик проверенной климатической техники в Москве и Московской области. Интернет-магазин предлагает большой выбор кондиционеров от известных мировых производителей, которые отличаются мощностью, надежностью, быстро создают комфортный микроклимат в помещении. В наличии последние новинки компаний Samsung, LG, Toshiba, BISMARK, EcoStar и многих других, которые представлены на сайте https://ruscondicioner.ru/ (монтаж кондиционера TOSHIBA недорого ) вместе с детальным описанием, фотографиями и указанием важных характеристик. Любую модель можно заказать вместе с доставкой и установкой.

Ассортимент климатической техники «РусКондиционер» включает настенные, полупромышленные кондиционеры и мультисплит системы. Настенные кондиционеры – привычные нам модели, которые устанавливают в частных и коммерческих помещениях. Состоят из внутреннего блока, который крепится на внутренней стене, и внешнего блока, расположенного на фасаде здания. Отличаются небольшой мощностью, подходят для квартир, частных домов, офисов.

Мультисплит системы предназначены для охлаждения, нагревания и вентиляции воздуха в помещении. Состоит из одного наружного блока, к которому можно присоединить до шести внутренних блоков. В каталоге можно подобрать мультисплит системы с двумя и более наружными блоками по выгодной стоимости. Для промышленных целей можно заказать более мощные установки – кассетные, канальные, напольно-потолочные. Консультанты магазина «РусКондиционер» помогут сделать правильный выбор в зависимости от типа, площади помещения и предпочтений заказчика.

Сотрудники компании «РусКондиционер» доставляют, устанавливают климатические системы и предоставляют квалифицированное обслуживание. Если нужно почистить кондиционер, заменить детали и наладить работу, звоните по указанному на сайте номеру или оставляйте заявку.

«DEVIL KISS» – совершенно новый интернет-магазин в сфере интимных товаров, который уже успел завоевать популярность среди покупателей. Магазин предлагает сертифицированные интим-товары, изготовленные из нетоксичных материалов, которые прошли проверку на безопасность. Ассортимент включает более 20 тысяч наименований, которые помогут разнообразить интимную жизнь, подарят новые незабываемые ощущения. На сайте https://devilkiss-sexshop.ru/ (купить недорого бюстгальтер без косточек онлайн ) можно заказать:

– эротическое белье;

– косметику с феромонами;

– масла для массажа;

– секс-игрушки;

– аксессуары для ролевых игр;

– БДСМ-товары для любителей острых ощущений.

Предлагаемые товары прошли контроль качества и имеют все необходимые подтверждающие документы. Для удобства позиции разделены на категории, к каждому продукту предлагается детальное описание вместе с фотографиями, что помогает определиться с покупкой. Здесь можно подобрать подарок себе и близкому человеку, который привнесет в жизнь новые эмоции и ощущения. Ассортимент товаров постоянно пополняется, поэтому здесь всегда будет из чего выбрать. При этом цены вполне демократичные.

Если требуется помощь в выборе, всегда можно обратиться к сотрудникам магазина. Поддержка клиентов действует круглосуточно, в любое время можно узнать о наличии интересующего вас товара, его стоимость и характеристики. Консультант всегда поможет с выбором, ориентируясь на предпочтения клиента, порекомендует новые игрушки и интимные средства, сохраняя полную анонимность покупателя.

Доставка товаров осуществляется по всей России. Посылки доставляются в непрозрачной упаковке без указания названий товаров и логотипа магазина. Сделав заказ в «DEVIL KISS», вы получаете качественные товары по доступной цене с сохранением анонимности.

Видео обзоры: политика россии и украины

Компания ProfilDoors специализируется на производстве межкомнатных дверей разных ценовых категорий в Москве. При изготовлении продукции фабрика применяет инновационные подходы, высококачественные материалы и фурнитуру, поставляет стильные и практичные решения для любого интерьера. Получаемые изделия прочные, надежные, выполнены с учетом современных стилевых особенностей. Ассортимент продукции насчитывает несколько серий, каждая из которых отличается уникальным дизайном и функциональностью. В наличии двери разных ценовых категорий, где каждый подберет вариант по выгодной стоимости.

На сайте https://profeldoors.ru/ (купить профильдорс ) представлен ассортимент межкомнатных дверей, который включает:

– раздвижные двери;

– алюминиевые двери;

– каркасные двери;

– скрытые двери;

– двери специального назначения;

– межкомнатные двери с имитацией натурального дерева;

– двери со стеклами и различными покрытиями.

Предлагаемые варианты отличаются стилем, дизайном, материалами исполнения, системами открывания, техническими особенностями. В наличии модели в классическом и современном исполнении, оснащенные техническими улучшениями. Разнообразие моделей позволяет подобрать подходящее решение для любого интерьера. Вместе с дверьми можно приобрести напольные плинтуса, стеновые панели, а также все необходимое для установки в том же стиле и цветовой гамме. Также в наличии качественная фурнитура – замки, ручки, ограничители и шпингалеты.

Если требуется помощь при выборе, обращайтесь по указанному на сайте номеру. Менеджер компании подберет лучший вариант с учетом ваших предпочтений. Магазин находится на строительном рынке «Мельница», где можно подобрать двери и самостоятельно забрать заказ. Контактные данные и время работы также указаны на сайте.

Hi, just wanted to tell you, I liked this post. It was inspiring.

Keep on posting!

Social media management bali recently posted…Social media management bali

I every time emailed this weblog post page to all my contacts, as

if like to read it then my links will too.

ilicone sex doll recently posted…ilicone sex doll

Бумага офисная PaperWorld A4.

Jфсетная 80г/м2, 500 листов, Белизна 146%, класс С.

Цена 500 руб

Тел. 84951093115

**@pr*******.ru

https://printfoil.ru/

Агентство недвижимости «В Батуми» предоставляет услуги гостям и жителям Грузии. Если интересует аренда жилья в Батуми, на сайте компании можно найти самые актуальные предложения разных ценовых категорий. Сотрудники агентства подбирают жилье с учетом бюджета, расположения и других требований клиента. Чтобы начать сотрудничество, достаточно оставить заявку или позвонить по указанному номеру.

В каталоге представлен большой выбор предложений с фотографиями и необходимой для клиентов информацией. Агентство недвижимости предлагает арендовать:

– квартиры-студии;

– 1-комнатные, 2-комнатные, 3-комнатные квартиры;

– частные дома;

– виллы; коттеджи;

– гостиницы;

– комнаты.

В каждом объявлении обязательно указывается количество комнат, площадь помещения, удобства, расстояние до центра, моря, важных достопримечательностей, а также возможный срок аренды. Описания представлены вместе с актуальными фотографиями и стоимостью. Также в каталоге размещаются квартиры и частные дома, которые выставлены на продажу. На главной странице представлены новые объекты недвижимости в Батуми, Тбилиси, Григолети, Гонио, которые можно купить или арендовать на необходимое время. Сотрудники компании «В Батуми» помогут с выбором объекта с учетом всех пожеланий клиента. На сайте https://vbatumi.ge/ (квартира в Чакви дешево ) можно выбрать оптимальный вариант на любой бюджет – от небольшого гостиничного номера до роскошной загородной виллы.

Услуга аренда жилья в Кобулети доступна для заказа вместе с экскурсионными турами. На сайте можно выбрать жилье, а также интересные экскурсии, куда можно отправиться во время отдыха. Стоит заранее забронировать номер или квартиру, а также позаботиться о досуге – с этим гостям солнечных грузинских городов поможет агентство «В Батуми».

Строительная компания «Рост» предоставляет перечень услуг по проектированию и строительству квартир и домов любого уровня сложности. Более 10 лет компания занимается проектированием и строительными работами в Ростове-на-Дону, применяя современные технологии и качественные материалы. Работы выполняют опытные сотрудники, каждый из которых имеет определенную специализацию – дизайнеры, проектировщики, инженеры, строители. На сайте https://rost-sk.com/ (дома в аксае ) можно ознакомиться с работами компании – здесь представлены дизайн-проекты, а также готовые строения. Какие услуги можно заказать в компании «Рост»:

– проектирование – дизайн-проекты разрабатываются индивидуально в определенном стиле, цветах, с учетом предпочтений клиента;

– строительство – для возведения домов используются современные материалы – кирпич, газобетон, керамические блоки;

– внутренняя отделка – выполняем быстро и качественно внутренние работы с использованием лучших отделочных материалов.

Обратившись в компанию «Рост», можно заказать полный комплекс строительных услуг, начиная от проектирования и заканчивая сдачей готового объекта. Для сотрудничества достаточно оставить заявку на сайте или позвонить по указанному номеру. При обращении клиенты бесплатно получают консультацию, что позволяет больше узнать об услугах. Следующий этап сотрудничества – разработка индивидуального дизайн-проекта, после утверждения которого остается согласовать график работ, чтобы начать строительство.

Все работы проводятся на основании заранее составленной сметы, где детально рассчитывается количество стройматериалов и точная стоимость, что исключает дополнительные расходы. Компания предоставляет гарантию сроком на 50 лет на выполненные работы.

Portal de Internet https://kpopmas.com creado para los fans de la moderna cultura pop coreana. En este sitio se puede encontrar toda la informacion mas actualizada sobre los idols. Aqui se recopilan datos biograficos, noticias de Ultima hora, anuncios de conciertos, videos musicales, portadas de revistas, numerosas publicaciones que hablan de la vida de los artistas famosos, kpop grupos y otras celebridades coreanas. Este sitio web esta decorado con fotografias coloridas en colores brillantes, destacando la caracteristica cultura pop coreana.

Lo que se puede encontrar en el sitio web:

– las ultimas noticias sobre idols famosos;

– discografias de artistas coreanos populares y grupos;

– videos musicales y teasers de conciertos y artistas coreanos;

– tendencias de moda coreana, salidas elegantes de los idols;

– tests tematicos y entretenidos para los amantes de la cultura pop coreana;

– datos biograficos y datos interesantes de la vida de las celebridades coreanas.

La pagina principal contiene los materiales mas relevantes y las ultimas actualizaciones. Puede encontrar informacion sobre BTS, STRAY KIDS, EXO, BLACKPINK y otros grupos populares de K-pop. Utilice la busqueda en el sitio para encontrar materiales sobre el grupo que le interesa, ver sesiones de fotos, videos musicales de

fama mundial, asi como descubrir la historia de los idols sobre como se convertieron en artistas. Los lectores pueden descubrir mas informacion sobre los grupos de K-pop femeninos y masculinos, familiarizarse con las alineaciones y evaluar el tipo de musica que crean. Ademas, se presentan discografias con albumes y videos musicales que estan disponibles para escuchar.

La informacion en el sitio se actualiza regularmente. Aqui se publican las ultimas noticias con fotos y datos interesantes. Los materiales presentados se dividen en categorias, por lo tanto, el usuario encontrara facilmente noticias de interes sobre ciertas celebridades coreanas.

«РусКондиционер» – поставщик проверенной климатической техники в Москве и Московской области. Интернет-магазин предлагает большой выбор кондиционеров от известных мировых производителей, которые отличаются мощностью, надежностью, быстро создают комфортный микроклимат в помещении. В наличии последние новинки компаний Samsung, LG, Toshiba, BISMARK, EcoStar и многих других, которые представлены на сайте https://ruscondicioner.ru/ (кондиционер хаер монтаж ) вместе с детальным описанием, фотографиями и указанием важных характеристик. Любую модель можно заказать вместе с доставкой и установкой.

Ассортимент климатической техники «РусКондиционер» включает настенные, полупромышленные кондиционеры и мультисплит системы. Настенные кондиционеры – привычные нам модели, которые устанавливают в частных и коммерческих помещениях. Состоят из внутреннего блока, который крепится на внутренней стене, и внешнего блока, расположенного на фасаде здания. Отличаются небольшой мощностью, подходят для квартир, частных домов, офисов.

Мультисплит системы предназначены для охлаждения, нагревания и вентиляции воздуха в помещении. Состоит из одного наружного блока, к которому можно присоединить до шести внутренних блоков. В каталоге можно подобрать мультисплит системы с двумя и более наружными блоками по выгодной стоимости. Для промышленных целей можно заказать более мощные установки – кассетные, канальные, напольно-потолочные. Консультанты магазина «РусКондиционер» помогут сделать правильный выбор в зависимости от типа, площади помещения и предпочтений заказчика.

Сотрудники компании «РусКондиционер» доставляют, устанавливают климатические системы и предоставляют квалифицированное обслуживание. Если нужно почистить кондиционер, заменить детали и наладить работу, звоните по указанному на сайте номеру или оставляйте заявку.

Избавиться от долговых обязательств, закрыть непосильные кредиты и получить шанс на свободную жизнь поможет процедура банкротства. Если хотите законно списать все долги по кредитам, распискам, услугам ЖКХ, стоит обратиться к юристам компании «АВ ЗАЩИТА», которые специализируются на банкротстве. Ваши проблемы будет решать команда опытных юристов, аудиторов, бухгалтеров, регистраторов, которые на протяжении 5 лет предоставляют услуги жителям Волгограда. Оставляйте на сайте https://банкротство34.рф/ (стоимость банкротства физ лица в волгограде ) заявку, чтобы получить бесплатную консультацию специалиста и сделать первый шаг к решению проблемы.

Услуги компании «АВ ЗАЩИТА» включают помощь в получении банкротства юридическим и физическим лицам напрямую от арбитражного управляющего. Специалисты индивидуально рассматривают каждую ситуацию, гарантируют полную конфиденциальность, помогают полностью списать долги за фиксированную оплату.

Сотрудничество с компанией «АВ ЗАЩИТА» включает несколько этапов:

– оформление заявки – достаточно позвонить по указанному на сайте номеру или отправить заявку с контактными данными, чтобы обратиться за помощью;

– анализ документов – специалист назначит встречу в удобное для клиента время, где детально разберет и проанализирует кредитные договора, долговые расписки и другие документы, которые относятся к делу;

– подготовка документации – юрист берет на себя все обязательства по оформлению документов, которые потребуются для получения банкротства;

– контроль и сопровождение – на всех этапах сотрудничества сотрудники компании «АВ ЗАЩИТА» предоставляют квалифицированную юридическую помощь и представляют интересы клиента в суде.

На счету компании больше 50 успешных дел по списанию долга. Если есть сомнения, можно просмотреть отзывы от клиентов, которые размещены на сайте.

«DEVIL KISS» – совершенно новый интернет-магазин в сфере интимных товаров, который уже успел завоевать популярность среди покупателей. Магазин предлагает сертифицированные интим-товары, изготовленные из нетоксичных материалов, которые прошли проверку на безопасность. Ассортимент включает более 20 тысяч наименований, которые помогут разнообразить интимную жизнь, подарят новые незабываемые ощущения. На сайте https://devilkiss-sexshop.ru/ (плетка секс шоп ) можно заказать:

– эротическое белье;

– косметику с феромонами;

– масла для массажа;

– секс-игрушки;

– аксессуары для ролевых игр;

– БДСМ-товары для любителей острых ощущений.

Предлагаемые товары прошли контроль качества и имеют все необходимые подтверждающие документы. Для удобства позиции разделены на категории, к каждому продукту предлагается детальное описание вместе с фотографиями, что помогает определиться с покупкой. Здесь можно подобрать подарок себе и близкому человеку, который привнесет в жизнь новые эмоции и ощущения. Ассортимент товаров постоянно пополняется, поэтому здесь всегда будет из чего выбрать. При этом цены вполне демократичные.

Если требуется помощь в выборе, всегда можно обратиться к сотрудникам магазина. Поддержка клиентов действует круглосуточно, в любое время можно узнать о наличии интересующего вас товара, его стоимость и характеристики. Консультант всегда поможет с выбором, ориентируясь на предпочтения клиента, порекомендует новые игрушки и интимные средства, сохраняя полную анонимность покупателя.

Доставка товаров осуществляется по всей России. Посылки доставляются в непрозрачной упаковке без указания названий товаров и логотипа магазина. Сделав заказ в «DEVIL KISS», вы получаете качественные товары по доступной цене с сохранением анонимности.

Компания ProfilDoors специализируется на производстве межкомнатных дверей разных ценовых категорий в Москве. При изготовлении продукции фабрика применяет инновационные подходы, высококачественные материалы и фурнитуру, поставляет стильные и практичные решения для любого интерьера. Получаемые изделия прочные, надежные, выполнены с учетом современных стилевых особенностей. Ассортимент продукции насчитывает несколько серий, каждая из которых отличается уникальным дизайном и функциональностью. В наличии двери разных ценовых категорий, где каждый подберет вариант по выгодной стоимости.

На сайте https://profeldoors.ru/ (profil doors invisible цена ) представлен ассортимент межкомнатных дверей, который включает:

– раздвижные двери;

– алюминиевые двери;

– каркасные двери;

– скрытые двери;

– двери специального назначения;

– межкомнатные двери с имитацией натурального дерева;

– двери со стеклами и различными покрытиями.

Предлагаемые варианты отличаются стилем, дизайном, материалами исполнения, системами открывания, техническими особенностями. В наличии модели в классическом и современном исполнении, оснащенные техническими улучшениями. Разнообразие моделей позволяет подобрать подходящее решение для любого интерьера. Вместе с дверьми можно приобрести напольные плинтуса, стеновые панели, а также все необходимое для установки в том же стиле и цветовой гамме. Также в наличии качественная фурнитура – замки, ручки, ограничители и шпингалеты.

Если требуется помощь при выборе, обращайтесь по указанному на сайте номеру. Менеджер компании подберет лучший вариант с учетом ваших предпочтений. Магазин находится на строительном рынке «Мельница», где можно подобрать двери и самостоятельно забрать заказ. Контактные данные и время работы также указаны на сайте.

Агентство недвижимости «В Батуми» предоставляет услуги гостям и жителям Грузии. Если интересует аренда жилья в Батуми, на сайте компании можно найти самые актуальные предложения разных ценовых категорий. Сотрудники агентства подбирают жилье с учетом бюджета, расположения и других требований клиента. Чтобы начать сотрудничество, достаточно оставить заявку или позвонить по указанному номеру.

В каталоге представлен большой выбор предложений с фотографиями и необходимой для клиентов информацией. Агентство недвижимости предлагает арендовать:

– квартиры-студии;

– 1-комнатные, 2-комнатные, 3-комнатные квартиры;

– частные дома;

– виллы; коттеджи;

– гостиницы;

– комнаты.

В каждом объявлении обязательно указывается количество комнат, площадь помещения, удобства, расстояние до центра, моря, важных достопримечательностей, а также возможный срок аренды. Описания представлены вместе с актуальными фотографиями и стоимостью. Также в каталоге размещаются квартиры и частные дома, которые выставлены на продажу. На главной странице представлены новые объекты недвижимости в Батуми, Тбилиси, Григолети, Гонио, которые можно купить или арендовать на необходимое время. Сотрудники компании «В Батуми» помогут с выбором объекта с учетом всех пожеланий клиента. На сайте https://vbatumi.ge/ (Шекветили экскурсии ) можно выбрать оптимальный вариант на любой бюджет – от небольшого гостиничного номера до роскошной загородной виллы.

Услуга аренда жилья в Кобулети доступна для заказа вместе с экскурсионными турами. На сайте можно выбрать жилье, а также интересные экскурсии, куда можно отправиться во время отдыха. Стоит заранее забронировать номер или квартиру, а также позаботиться о досуге – с этим гостям солнечных грузинских городов поможет агентство «В Батуми».

новости россии сегодня видео

экономика россии сегодня последние новости

смотреть новости эфир

новости соцсетей россии

последние новости сегодняшнего дня

новости крыма сегодня

социальная политика россии

главные новости сегодня

новости россии читать

концепция внешней политики россии

события сегодня последние новости

новости здоровье сегодня

происшествия последние новости сегодня

новости криминал

последние новости в россии

Строительная компания «Рост» предоставляет перечень услуг по проектированию и строительству квартир и домов любого уровня сложности. Более 10 лет компания занимается проектированием и строительными работами в Ростове-на-Дону, применяя современные технологии и качественные материалы. Работы выполняют опытные сотрудники, каждый из которых имеет определенную специализацию – дизайнеры, проектировщики, инженеры, строители. На сайте https://rost-sk.com/ (как выбрать кровлю ) можно ознакомиться с работами компании – здесь представлены дизайн-проекты, а также готовые строения. Какие услуги можно заказать в компании «Рост»:

– проектирование – дизайн-проекты разрабатываются индивидуально в определенном стиле, цветах, с учетом предпочтений клиента;

– строительство – для возведения домов используются современные материалы – кирпич, газобетон, керамические блоки;

– внутренняя отделка – выполняем быстро и качественно внутренние работы с использованием лучших отделочных материалов.

Обратившись в компанию «Рост», можно заказать полный комплекс строительных услуг, начиная от проектирования и заканчивая сдачей готового объекта. Для сотрудничества достаточно оставить заявку на сайте или позвонить по указанному номеру. При обращении клиенты бесплатно получают консультацию, что позволяет больше узнать об услугах. Следующий этап сотрудничества – разработка индивидуального дизайн-проекта, после утверждения которого остается согласовать график работ, чтобы начать строительство.

Все работы проводятся на основании заранее составленной сметы, где детально рассчитывается количество стройматериалов и точная стоимость, что исключает дополнительные расходы. Компания предоставляет гарантию сроком на 50 лет на выполненные работы.

https://vlmi.ws/members/limaojek.164272/#about

Portale Randkowe Opinie

Randki Toruń

Питомник «Садоград» на протяжении 30-ти лет поставляет качественные саженцы садоводам Москвы и Московской области. В наличии большая коллекция плодовых и декоративных растений, которые станут достойным украшением любого сада. Саженцы продаются оптом и в розницу по выгодной стоимости, многие позиции представлены со скидками. Жители Москвы и Подмосковья могут самостоятельно забрать заказ без очереди или с доставкой по городу. В другие регионы саженцы и семена отправляются почтой.

В питомнике выращивают различные сорта плодовых деревьев и кустарников, хвойных и цветущих растений, а также винограда, земляники, орехов. Предлагаемые саженцы находятся на стадии роста и продаются в пакетах с землей. Для высадки нужно просто перенести содержимое в грунт, стараясь не повредить корневую систему. Закаленные саженцы выдерживают неблагоприятные погодные условия, они зимуют в грунте, поэтому их можно заказывать в любое время года.

Что можно заказать в питомнике «Садоград»:

– саженцы плодовых деревьев – черешни, вишни, груши, персика, абрикоса;

– саженцы орехов – фундука, миндаля;

– саженцы хвойных деревьев – пихты, лиственницы, можжевельника, кедра;

– саженцы лиственных деревьев – клена, ясеня, березы, вяза, липы, дуба;

– саженцы кустарников – смородины, барбариса, боярышника.

На сайте https://sadograd.ru/ (питомник заозерье ) можно ознакомиться с ассортиментом и получить необходимую информацию для садовода. В каталоге размещены доступные для заказа саженцы с реальными фотографиями и описаниями. Для оптовых покупателей предлагаются скидки в размере 5 – 10% в зависимости от суммы заказа. Черенки и семена можно заказать почтой, также доступна услуга обмена саженцев при предоставлении чека. За консультацией и для оформления заказа обращайтесь по указанному номеру. Адрес и время работы питомника представлены на сайте.

Питомник «Садоград» на протяжении 30-ти лет поставляет качественные саженцы садоводам Москвы и Московской области. В наличии большая коллекция плодовых и декоративных растений, которые станут достойным украшением любого сада. Саженцы продаются оптом и в розницу по выгодной стоимости, многие позиции представлены со скидками. Жители Москвы и Подмосковья могут самостоятельно забрать заказ без очереди или с доставкой по городу. В другие регионы саженцы и семена отправляются почтой.

В питомнике выращивают различные сорта плодовых деревьев и кустарников, хвойных и цветущих растений, а также винограда, земляники, орехов. Предлагаемые саженцы находятся на стадии роста и продаются в пакетах с землей. Для высадки нужно просто перенести содержимое в грунт, стараясь не повредить корневую систему. Закаленные саженцы выдерживают неблагоприятные погодные условия, они зимуют в грунте, поэтому их можно заказывать в любое время года.

Что можно заказать в питомнике «Садоград»:

– саженцы плодовых деревьев – черешни, вишни, груши, персика, абрикоса;

– саженцы орехов – фундука, миндаля;

– саженцы хвойных деревьев – пихты, лиственницы, можжевельника, кедра;

– саженцы лиственных деревьев – клена, ясеня, березы, вяза, липы, дуба;

– саженцы кустарников – смородины, барбариса, боярышника.

На сайте https://sadograd.ru/ (сирень питомник ) можно ознакомиться с ассортиментом и получить необходимую информацию для садовода. В каталоге размещены доступные для заказа саженцы с реальными фотографиями и описаниями. Для оптовых покупателей предлагаются скидки в размере 5 – 10% в зависимости от суммы заказа. Черенки и семена можно заказать почтой, также доступна услуга обмена саженцев при предоставлении чека. За консультацией и для оформления заказа обращайтесь по указанному номеру. Адрес и время работы питомника представлены на сайте.

Консалтинговая компания SQLTeam специализируется на разработке, аналитике и администрировании баз данных. В команде работают эксперты, которые оказывают услуги удаленного администрирования баз данных в различных отраслях. Специалисты реализуют проекты в разных сферах: финансовой, строительной, туристической, производственной и многих других. На сайте https://sqlteam.ru (разработка пользовательского интерфейса базы данных ) можно получить более детальную информацию о предлагаемых услугах.

Какие услуги предоставляет компания SQLTeam:

– консультирование – специалисты предложат эффективное решение для каждой индивидуальной ситуации;

– администрирование – команда экспертов проводит оценку сервисов, настраивает работу удаленного DBA, обеспечивает максимальную производительность;

– разработка баз данных – включает разработку приложений, настройку существующих решений, создание интерфейса для базы данных, услуги по обновлению;

– аналитика и хранилище данных – выполняется преобразование информации, предлагается возможность анализа новых тенденций, аудит, а также бизнес-прогнозирование;

– тестирование – позволяет обнаружить и устранить ошибки, что необходимо для бесперебойного функционирования баз данных;

– внедрение баз данных – проводится быстрое обучение, оптимизация, предоставляется экспертная техподдержка.

Для ознакомления компания предлагает бесплатную пробную версию. Эксперты готовы к нестандартным заданиям, предоставляя высококачественное обслуживание. Чтобы заказать интересующую услугу, достаточно оставить заявку на сайте или позвонить по указанному номеру. Специалисты бесплатно консультируют, помогают подобрать лучшее решение для бизнеса, а также предлагают разработку, аудит, обновление баз данных и профессиональное сопровождение для разных отраслей.

Фирменный магазин Profil Doors предлагает приобрести качественные и стильные межкомнатные двери от производителя. Компания занимается изготовлением дверей по индивидуальным параметрам, которые можно заказать с разными вариантами оформления. В ассортименте представлен широкий модельный ряд дверей, которые идеально вписываются как в классический, так и в современный интерьер.

На сайте https://profiledoors.ru/ (двери купе в потолок межкомнатные ) представлен каталог товаров производства компании Profil Doors. Ассортимент включает алюминиевые, каркасные, царговые двери, каждый вид имеет свои особенности. Царговые двери представлены в однотонных конструкциях, которые обработаны специальным покрытием, защищающим от царапин и различных видов повреждений. В наличии более сотни моделей в стильных цветах: магнолия, антрацит, аляска. Популярностью пользуются каркасные конструкции, которые представлены в однотонном исполнении с матовым покрытием. Алюминиевые двери – прочные, износостойкие, эстетичные. Благодаря многообразию моделей можно подобрать подходящий вариант для любого интерьера.

Фирменный магазин дверей предлагает более 7000 моделей разных ценовых категорий. Конструкции оснащены звукоизоляцией, теплоизоляцией, качественной фурнитурой. Сотрудники магазина помогут подобрать межкомнатные двери для жилых и коммерческих помещений. В компании Profil Doors можно заказать изготовление дверей нестандартной формы по индивидуальным параметрам. В производстве используются качественные материалы и фурнитура. Вместе с дверьми можно приобрести ручки, замки, шпингалеты, а также перегородки. В Москве доступна услуга установки межкомнатных дверей, которую выполняют сотрудники компании. Для заказа звоните по указанному номеру или оставляйте заявку.

https://vlmi.ws/members/limaojek.164272/

Lento Randki I Przyjaciele

Randki Bez Cenzury Online

https://casinobrangonodeposit.teamapp.com/?_webpage=v1

https://glitch.com/~obtainable-scalloped-organization

https://groups.google.com/g/najlepsze-portale-randkowe-2022

Spotkania W Okolicy PL

Jaki Portal Randkowy Polecacie 2022

https://casinobrangonodeposit.teamapp.com/clubs/705400/documents/1064984?_detail=v1

https://telescope.ac/casino-brango-no-deposit-bonus-codes-2022-6joPSHlCj

https://www.google.com/maps/d/u/2/viewer?mid=1RmwQFbKsvZvoSH37eZfagz4IDNSK9w_Q&ll=52.01443895257166%2C19.145136500000024&z=7

Szybkie Randki Kraków

Randki Białystok

https://www.pinterest.com/pin/1069042030270668825/

https://www.ulule.com/janrokitttaas/

https://rift.curseforge.com/paste/cb0ff8c3

Szukam Drugiej Połówki Bez Rejestracji

Randki Toruń

https://www.pinterest.com/janrokiita/_saved/

https://www.pinterest.com/pin/1069042030270668825/

https://pastecode.io/s/xqmwevis

Randkujemy PL Logowanie

OLX Randki

https://hackaday.io/doreees

https://glitch.com/~obtainable-scalloped-organization

https://ideone.com/gUtljo

Portal Randkowy Warszawa

Oferty Matrymonialne

https://glitch.com/~obtainable-scalloped-organization

https://hackaday.io/page/12760-lolo

https://groups.google.com/g/najlepsze-portale-randkowe-2022/c/hsELlerJmM8/m/WGy0HB7ABAAJ

Randkujemy PL Logowanie

Randki Bez Cenzury

https://www.pinterest.com/pin/1069042030270668825/

https://www.pinterest.com/pin/1069042030270668825/

Saved as a favorite, I like your website!

How Low Can Your Oxygen Level Go Before You Die recently posted…How Low Can Your Oxygen Level Go Before You Die

https://www.db-forum.de/members/qwertypeevy.50152/

Randki Rzeszów

Ranking Portali Randkowych

https://hackaday.io/page/12760-lolo

https://glitch.com/~obtainable-scalloped-organization

https://linktr.ee/randkowaniezadarmo

Randki Białystok

Randkujemy PL Logowanie

https://tawk.to/fb3dbb2a59af6dd549e9484409a12e47cbdddebe

https://glitch.com/~obtainable-scalloped-organization

https://www.et-alors.net/forum/viewtopic.php?t=34545

Nagie Randki

Strony Randkowe

https://telescope.ac/casino-brango-no-deposit-bonus-codes-2022-6joPSHlCj

https://hackaday.io/page/12760-lolo

nutakugold.club/freenutakugold/

MAY UPDATED!

So hacken Sie NUTAKU-Spiele 2022

NUTAKU Gold Coin Hack No Survey 2022 AKTUALISIERT

nutakugold.club/freenutakugold/

MAY UPDATED!

NUTAKU Gold Coin Hack No Survey 2022 UPDATED

NUTAKU FREE COINS 2022 UPDATED

nutakugold.club/freenutakugold/

MAY UPDATED!

NUTAKU Or Glitch 2022

So erhalten Sie NUTAKU Gold 2022

nutakugold.club/freenutakugold/

MAY UPDATED!

NUTAKU Gold Free 2022 MISE À JOUR

NUTAKU gold codes uk MISE À JOUR

nutakugold.club/freenutakugold/

MAY UPDATED!

Est-ce que NUTAKU Gold Hack fonctionne 2022 MISE À JOUR

nutaku pièces gratuites android MISE À JOUR

Где купить разнообразные игры +на xbox приставку Попробуй в роли себя наемного убийцы игрый в Hitman 2 + https://plati.market/itm/3016084

какую игру xbox купить+ https://plati.market/itm/2997767

xbox купить игру лицензию+ https://wmcentre.net/item/dirt-rally-2-0-game-of-the-year-edition-xbox-one-3205689

купить аккаунт xbox+https://wmcentre.net/item/resident-evil-2-resident-evil-3-xbox-3203379

купить игры на пк+http://mysel.ru/listing.php?category_id=115202

Новые игры аккаунты в аренду+https://wmcentre.net/item/resident-evil-2-resident-evil-3-xbox-3203379

Аудиокниги,книги по психологии+https://plati.market/itm/3290749

steam game code+https://plati.market/itm/3012399

Xbox Game Pass Ultimate + EA Play+https://mysel.ru/goods_info.php?id=3152163

Assassins Creed xbox one+https://plati.market/itm/2966161

Resident Evil xbox one+https://plati.market/itm/3051324

Call Of duty xbox one+https://plati.market/itm/3025661

Hitman xbox One+https://plati.market/itm/3037131

Battlefield xbox one key+https://plati.market/itm/2892228

Metro Xbox Key+https://plati.market/itm/2956581

игры XBOX XD KEY MYSEL>RU https://mysel.ru Торговая площадка цифровых товаров

FIFA 20 XBOX ONE Ключ / Цифр код + подарок

Grand Theft Auto V / GTA 5 XBOX ONE Цифровой Ключ ??

Mafia Definitive Edition XBOX CD KEY

METRO: LAST LIGHT REDUX +подарок

The Crew 2 XBOX/PC+present

Diablo III: Eternal Collection Xbox One

Steam Turkey 50 TL Gift Card Code(FOR TURKEY ACCOUNTS)

Netflix Турция Подарочный код 100 TL

The Division 2 –

Crysis 1,2 XBOX ONE

MORTAL KOMBAT 11 XBOX ONE X/S

King?s Bounty II – Lord?s Edition XBOX ONE

Amazon Gift Card US $10

AVG TuneUp 1 ПК 1 год –

iTUNES GIFT CARD – $15(USA)

Wolfenstein: I, II xbox

Dead Rising Triple Bundle Pack XBOX / КЛЮЧ

Thief Xbox One

Nba 2k20 xbox one

Подписка EA Play: 1 месяц (цифровая версия)Xbox One

Nintendo Switch Online Подписка 3 МЕС EU/RU

Adguard Premium 1ПК+https://wmcentre.net/item/adguard-premium-1pk-na-1-god-3203400

AVG TuneUp 1 ПК 1 ключ+https://plati.market/itm/3048052

5$ Предоплаченная VISA USA для покупки в online

Хочешь купить машину, срочно нужны деньги, не хватате на покупку иди в банк HOME BANKE

ADVCASH-карта Быстро, удобно, без лишних комиссий.Пластиковые и виртуальные prepaid-карты в разных валютах.Удобные расчеты по всему миру.+https://wallet.advcash.com:443/referral/e03d7801-07e6-4037-9c19-d4392252234f

Стань успешным трейдером, торгуй на валютном рынке, получай прибыль+https://site.forex4you.ru.com/?affid=d339e9d

Автоматизация ваших действий в браузере, заработок с помощью шаблонов-Покупай Zennoposter+http://www.zennolab.com/ru/products/zennoposter/pid/304ef301-d306-4a83-bbd6-a6bfc4923335

Открой свой бизнес(заведи свой счет), работай на себя, зарегесрируй ИП или ООО бесплатно +https://sme.raiffeisen.ru/partners/leqgy080

Дешевый хостинг,качество по низкой цене+https://webhost1.ru/?r=133178

Покупай на ENOT-способ оплаты(0% при оплате банковской картой)11 способов оплаты

https://nutakugold.club/freenutakugold/

MAY UPDATED!

NUTAKU Gold Coin Hack 2022 UPDATED Générateur gratuit de pièces NUTAKU MISE À JOUR NUTAKU Gold Hack Password 2022 8c4d541

Comment obtenir NUTAKU Gold 2022 MISE À JOUR

NUTAKU Gold Coin Promo Codes 2022

https://nutakugold.club/freenutakugold/

MAY UPDATED!

NUTAKU Money Hack 2022

Doktor Strange 2022 Cały Film online

https://board.playpolar.net/viewtopic.php?f=14&t=198&p=267

https://nutakugold.club/freenutakugold/

MAY UPDATED!

NUTAKU gold codes uk UPDATED

Doktor Strange 2022 Cały Film online

https://www.camryforums.com/forum/members/wazznup-36549/

Taiwan Taiwan 4

В оформлении общественных пространств современного города очень распространены сухие фонтаны. Это прекрасный метод преобразить сквер, пространство перед магазином, отелем, офисным зданием, кафе и культурным заведением. Подобные места становятся запоминающимся местом взаимодействия городских жителей всех возрастных групп.

Сухой фонтан отличается тем фактом, что этот вид допустимо размещать в любом месте, где есть ровная площадка. Техническая часть данных установок находится ниже уровня земли, поэтому в остальное время территория подходит для использования по другому назначению.

Организация https://fontans.net.ua

предлагает купить пешеходные фонтаны классического или интерактивного вида: с подсвечиванием, музыкальным сопровождением, функциями управления. У нас вы можете оформить заказ на конструирование сухого фонтана для уличных объектов или общественных помещений из качественных стройматериалов с профессиональной установкой. Цена сухого фонтана считается индивидуально исходя из размера объекта , а также сложности работ.

Все услуги по проектированию и строительству фонтанов –

сухий фонтан

строительство городских фонтанов

стоимость строительства фонтана

проектирование сухого фонтана

проектирование и строительство фонтанов

проектирование и строительство фонтанов

строительство пешеходного фонтана

строительство больших фонтанов

сухой фонтан

строительство городских фонтанов

заказать строительство фонтана

сухой фонтан цена

пешеходные фонтаны цена

строительство пешеходного фонтана

сухой фонтан

строительство фонтанов под ключ

строительство прудов и фонтанов

строительство фонтанов под ключ

сухой фонтан

строительство бассейнов фонтанов

строительство фонтанов под ключ

пешеходные фонтаны цена

строительство и реконструкция фонтанов

проектирование и строительство фонтанов

строительство пешеходного фонтана

пешеходные фонтаны цена

строительство больших фонтанов

фонтаны строительство

строительство фонтана цена

сухой фонтан

https://alterbrains.com/forum/topic?p=7469

serial STRANGER THINGS sezon 4

STRANGER THINGS HDRip WEB-DLRip

STRANGER THINGS: SEZON 4: CZĘŚĆ 1 cda

https://alterbrains.com/forum/topic?p=7469

serial STRANGER THINGS sezon 4

STRANGER THINGS: SEZON 4: CZĘŚĆ 1 luknij za darmo

free casino bonus usa 2022 no deposit / uk / ca

https://www.twitch.tv/casinoacademy

Great weblog right here! Additionally your site quite

a bit up very fast! What web host are you the use of?

Can I get your affiliate hyperlink for your host? I desire

my website loaded up as fast as yours lol

Social Media Marketing bali recently posted…Social Media Marketing bali

Admiring the time and effort you put into your website and in depth information you offer.

It’s awesome to come across a blog every once in a while

that isn’t the same outdated rehashed material. Great read!

I’ve saved your site and I’m including your RSS feeds to my Google account.

become a credit card processor recently posted…become a credit card processor

https://szczury.org/viewtopic.php?f=37&p=1124930

STRANGER THINGS – sezon 4 – odcinek 1 za darmo cda pl

STRANGER THINGS: SEZON 4: CZĘŚĆ 1 cda

free casino bonus usa 2022 no deposit / uk / ca

https://hypothes.is/users/komikomi

https://online.flippingbook.com/view/1010242395/

STRANGER THINGS s04e01 za free

STRANGER THINGS – sezon 4 – odcinek 1 za darmo cda pl

draqa

free casino bonus usa 2022 no deposit / uk / ca

https://www.producthunt.com/@jan_rokiita

we’re elated having clicked on the web page, it’s toally the thing my workers and I were hoping in search of. The detailed information on this forum is with out a doubt needed and is going to support my friends and I a couple times a week great information. Looks like everone on the site gained a large amount of knowledge about the things I am interested in and categories of topics and information greatly show it. Typically I’m not on the net very much so as my wife and I get an opportunity We’re always looking this kind of knowledge or stuff similarly similar. we will come back. If you needed a bit of services like: : We sell used J & L Wire pallet racks or used shelves for sale near me of Long Beach

Компания «Строй теремок» предоставляет профессиональные услуги строительства и ремонта в Москве и области. Проводим полный комплекс работ, включающий разработку индивидуального дизайна, черновой ремонт, замену коммуникаций, внутреннюю отделку комнат, замену кровли и ряд других строительных услуг. Готовим детальную смету, закупаем качественные стройматериалы, просчитываем заранее стоимость интересующих клиента услуг. Работы ведутся на основании официального договора сотрудничества. На сайте https://stroyteremok.ru (ремонт однокомнатной квартиры ) представлены выполненные проекты, а также цены на все предлагаемые услуги.

Специалисты компании «Строй теремок» предоставляют комплекс услуг, включающий:

– строительство частных и многоквартирных домов с нуля, возведение деревянных построек;

– разработку индивидуальных дизайн-проектов с учетом стилевых предпочтений заказчика;

– ремонт квартир в новостройках и хрущевках любой сложности – от бюджетного до эксклюзивного авторского ремонта;

– ремонт коммерческих помещений – кафе, магазинов, аптек, гостиниц, ресторанов, клубов;

– отделка фасада, внутренние работы любой сложности.

Наиболее востребованными являются услуги ремонта частных домов и квартир в Москве и Подмосковье. Работы выполняют квалифицированные мастера с применением современного оборудования и инструментов. Специалисты убирают старые покрытия, устанавливают теплые полы, монтируют натяжные потолки, меняют сантехнику и электрику, ставят двери, обустраивают шумоизоляцию. В работе используются качественные материалы с учетом имеющегося бюджета и предпочтений заказчика.

Обратившись в «Строй теремок» можно заказать черновой, косметический, капитальный, элитный ремонт всей квартиры или одной комнаты. Менеджер рассчитает стоимость работ, расскажет об актуальных акциях, ответит на все интересующие вопросы.

Интернет-портал http://doramax.ru (эксклюзив перевод ) приглашает поклонников азиатской культуры, а именно – дорам, популярность которых растет по всему миру. На сайте собраны эксклюзивные южнокорейские, китайские, тайваньские, японские, тайские сериалы с профессиональным русским переводом. Сериалы разных готов выпуска представлены в отличном качестве, здесь вы найдете самые популярные дорамы, а также последние новинки 2022 года. Все представленные дорамы доступны для бесплатного просмотра в онлайн-кинотеатре.

Для удобства зрителей дорамы разделены на категории по странам, актерам и годам выпуска. Самые популярные картины собраны в ТОП лучших дорам Китая, Гонконга, Южной Кореи. К каждому сериалу прилагается краткое описание сюжета, что помогает зрителю выбрать интересный вариант для киносеанса.

Посетите раздел с анонсами, чтобы узнать о предстоящих премьерах, которые вскоре появятся на сайте. Новинки дорам, которые совсем недавно были добавлены на портал, можно найти в разделе 2022 года. Если вы только начинаете знакомство с азиатскими сериалами, обращайте внимание на оценки, просмотры и комментарии пользователей. Для поиска подходящего японской или тайваньской кинокартины, выбирайте категорию с названием страны, где собраны лучшие дорамы. Удобная навигация с информативными разделами поможет быстро определиться с выбором.

Азиатские дорамы доступны для онлайн-просмотра в хорошем качестве. На сайте размещены сериалы с переводом на русский язык в разных популярных жанрах – от драмы до комедии. Онлайн-плеер позволяет удобно переключать сезоны и серии, а также выбирать качество просмотра на компьютере или смартфоне. Кроме азиатских дорам, на сайте представлены популярные индийские, австралийские, турецкие, мексиканские сериалы, доступные для онлайн-просмотра.

https://smash.gg/user/983b026f

https://www.pinterest.com/pin/842525042802516426

https://www.pinterest.com/pin/842525042802516426

IMVU hacks 2022 IMVU clothes free generator a682b49

IMVU generator 2022

IMVU clothes free generator

Ищете хороший и недорогой вариант отдыха в пределах России? Отель «Иордан», расположенный в поселке Ольгинка, приглашает отдохнуть на берегу Черного моря в Краснодарском крае. Гостям предлагается большой выбор комфортных номеров, чистейшие пляжи, разнообразные развлечения для детей и взрослых, бассейн, активные экскурсии, бесплатный Wi-Fi, бесплатная парковка и прочие удобства. На сайте https://iordangd.ru/ (упражнения исправления сколиоза детей в Ольгинке ) можно выбрать номер и забронировать дату предстоящего отпуска, заполнив простую форму.

Преимущества отдыха в отеле «Иордан» в поселке Ольгинка:

– удобное расположение возле моря;

– большой выбор номеров со всем необходимым – 2-х, 3-х, 4-х местные комнаты уровня стандарт, комфорт, люкс;

– каждый день вкусное и разнообразное меню;

– бассейн, детске горки, лабиринт;

– целый день работают детские аниматоры;

– оздоровительные процедуры и активные разлечения – баня, сауна, хамам, йога, танцы.

В отеле «Иордан» семейный отдых будет насыщенным, комфортным и интересным. Каждый день гостей ждут разнообразные развлечения и увлекательные экскурсии, например катание на квадроциклах и парусной яхте, приятные спа-процедуры, детские активности и многое другое. Отдых для детей и родителей замомнится надолго и оставит самые приятные впечатления.

Отель дарит приятные скидки и возможность забронировать номер по сниженной стоимости. На сайте можно узнать информацию о действующих акциях, а также посмотреть фотографии предлагаемых номеров. Для бронирования номеров на сайте предлагается удобная форма, где нужно указать даты отдыха, контактные данные для связи и личные пожелания. Задать интересующие вопросы можно позвонив по указанному номеру. Отзывы гостей помогут составить предварительное впечатление и сделать правильный выбор.

Агентство недвижимости «В Батуми» предоставляет услуги гостям и жителям Грузии. Если интересует аренда жилья в Батуми, на сайте компании можно найти самые актуальные предложения разных ценовых категорий. Сотрудники агентства подбирают жилье с учетом бюджета, расположения и других требований клиента. Чтобы начать сотрудничество, достаточно оставить заявку или позвонить по указанному номеру.

В каталоге представлен большой выбор предложений с фотографиями и необходимой для клиентов информацией. Агентство недвижимости предлагает арендовать:

– квартиры-студии;

– 1-комнатные, 2-комнатные, 3-комнатные квартиры;

– частные дома;

– виллы; коттеджи;

– гостиницы;

– комнаты.

В каждом объявлении обязательно указывается количество комнат, площадь помещения, удобства, расстояние до центра, моря, важных достопримечательностей, а также возможный срок аренды. Описания представлены вместе с актуальными фотографиями и стоимостью. Также в каталоге размещаются квартиры и частные дома, которые выставлены на продажу. На главной странице представлены новые объекты недвижимости в Батуми, Тбилиси, Григолети, Гонио, которые можно купить или арендовать на необходимое время. Сотрудники компании «В Батуми» помогут с выбором объекта с учетом всех пожеланий клиента. На сайте https://vbatumi.ge/ (квартиры в Григолети купить недорого ) можно выбрать оптимальный вариант на любой бюджет – от небольшого гостиничного номера до роскошной загородной виллы.

Услуга аренда жилья в Кобулети доступна для заказа вместе с экскурсионными турами. На сайте можно выбрать жилье, а также интересные экскурсии, куда можно отправиться во время отдыха. Стоит заранее забронировать номер или квартиру, а также позаботиться о досуге – с этим гостям солнечных грузинских городов поможет агентство «В Батуми».

https://www.pinterest.com/pin/842525042802516426

IMVU hack android IMVU clothes free 2022 29a1b9a

imvu hack 2022

imvu hack 2022

Компания “ProfilDoors” занимается изготовлением стильных, качественных и функциональных межкомнатных дверей в Москве. Фабрика предлагает широкий модельных ряд изделий разных ценовых категорий, которые устанавливают в квартирах, частных домах, гостиницах, офисах, кафе и других помещениях. Благодаря стилевому разнообразию и демократичным ценам даже самый требовательный клиент найдет подходящий вариант. На сайте https://profeldoors.ru/ (двери в гостиную ) можно ознакомиться с ассортиментом продукции и оформить покупку в онлайн-режиме.

Ассортимент интернет-магазина ProfilDoors включает:

– большую коллекцию межкомнатных дверей с различными видами покрытий в эксклюзивном исполнении;

– качественную фурнитуру – дверные ручки, замки, шпингалеты, ограничители;

– прочные алюминиевые двери;

– комплектующие для установки межкомнатных дверей.

В наличии межкомнатные каркасные конструкции, выполненные из качественных современных материалов. Двери представлены с разными вариантами оформления – с имитацией натурального дерева, в стильных пастельных тонах, в глубоком черном цвете, со стеклами и без вставок. На поверхность наносится специальное покрытие, защищающее от царапин. Дополнительно можно установить шумоизоляцию для комфортного пребывания в комнате.

Большой популярностью пользуются царговые двери, которые отличаются небольшим весом, износостойкостью, стильным дизайном. В каталоге представлен большой выбор изделий в классическом и современном исполнении. Если нужна надежная дверь, стоит обратить внимание на алюминиевые конструкции. Дополнительно можно приобрести фурнитуру от производителя и необходимые комплектующие для установки межкомнатных дверей. Менеджер магазина ответит на интересующие вопросы и поможет с выбором.

https://coinmarketcap.com/watchlist/627e18c49a8c8d51dd485bec

IMVU ios hack IMVU hack online free b49408_

IMVU free credits

IMVU free clothes online

If you would like to grow your knowledge simply keep visiting this website and be updated with the latest gossip posted

here.

mia khalifa boob size recently posted…mia khalifa boob size

What’s Going down i am new to this, I stumbled upon this I have discovered

It positively helpful and it has aided me out loads.

I’m hoping to contribute & aid other users like its helped

me. Good job.

PE sex doll recently posted…PE sex doll

Hi there, its nice post concerning media print, we all be aware of media is

a great source of information.

Free credit card terminal recently posted…Free credit card terminal

Интернет-портал https://anizon.online (смотреть онлайн дораму дело ведёт юный детектив киндаити ) приглашает к просмотру новинок аниме в хорошем качестве, которые доступны для просмотра в онлайн-режиме. На сайте собрана внушительная коллекция аниме-сериалов в разных жанрах с профессиональной озвучкой. Лучшие сериалы в жанре фэнтези, приключения, драма, фантастика, экшен, романтика, ужасы размещены в отдельных подборках для удобного поиска. Смотреть аниме можно бесплатно без обязательной регистрации на портале.

Самые популярные аниме-сериалы представлены на одном сайте. Здесь регулярно появляются актуальные новинки и последние сезоны о храбрых героях, магических существах и фэнтезийных мирах. К каждому аниме прилагается краткое описание сюжета, на основании которого можно сделать выбор, а также скриншоты с эпизодами из фильма и комментарии зрителей. Все фильмы разделены по жанрам, вариантам дубляжа, годам выпуска, что упрощает поиск. Пользователи могут ставить оценки понравившимся сериалам, на основании которых разрабатывается рейтинг лучших аниме.

На главной странице онлайн-кинотеатра появляются лучшие новинки сезона, доступные к просмотру на смартфоне или компьютере. Благодаря удобной навигации можно быстро найти нужный фильм или выбрать аниме на основании отзывов и оценок зрителей. Также на сайте представлено расписание релизов, ютуб-блог с разборами фильмов и другая полезная информация. Чтобы быть в курсе всех обновлений и получить больше возможностей, рекомендуем зарегистрироваться на сайте.

Для быстрого поиска аниме в удобной онлайн-форме выбирайте жанр, оптимальный вариант озвучки, сезон сериала. На портале представлены как реалистичные, так и фантастические фильмы, их перечень постоянно пополняется, поэтому любителям аниме всегда будет из чего выбрать.

Компания Profil Doors реализует уникальные скрытые дверные конструкции собственного производства в Москве. Дверь-невидимка составляет единую плоскость со стеной, благодаря этому эффекту визуально увеличивается пространство и комната выглядит просторнее. Скрытые двери идеально вписываются в современный интерьер, выглядят стильно и минималистично. Конструкции изготавливаются из качественных материалов и комплектующих европейского производства, поэтому отличаются прочностью и износостойкостью.

На сайте https://profiledoors.ru/skrytye-dveri (двери Invisible со скрытым монтажом ) представлен широкий модельный ряд скрытых дверей производства Profil Doors. Конструкция состоит из скрытого алюминиевого короба, который монтируется в стену, дверного полотна, которое можно покрасить или обклеить обоями, а также скрытых петель. В наличии модели с двумя разными системами открывания дверей, которые отличаются типами конструкции и имеют разный угол открывания – 90° и 180°. Обе системы открывания используются при производстве разных модельных линеек.

В ассортименте магазина представлена широкая цветовая гамма моделей, варианты с матовым и глянцевым покрытием, а также со специальной облицовкой, которая защищает от царапин, повреждений и химических воздействий. Выпускаются двери стандартных размеров, также компания производит нестандартные модели по параметрам заказчика. Поверхность дверей можно покрасить в тот же цвет, что и стены, или наклеить обои для создания единого стиля и визуального расширения пространства.

Сотрудники компании Profil Doors помогут подобрать скрытые двери для квартиры, дома или офиса, учитывая дизайн интерьера и предпочтения клиента. За консультацией обращайтесь по указанному на сайте номеру или оставляйте заявку.

«Рост» – строительная компания, которая занимается возведением домов и коттеджев по индивидуальному проекту. Компания предоставляет услуги более 10 лет, проводит полный комплекс строительных и отделочных работ, разрабатывает оригинальные дизайн-проекты с учетом предпочтений клиентов. Сотрудники фирмы «Рост» берут на себя все обязательства по подготовке документов, рассчитывают и закупают строительные материалы, применяют новейшие технологии и профессиональное оборудование. На сайте https://rost-sk.com/ (проектирование в ростове ) можно ознакомиться с примерами готовых проектов компании «Рост».

Сотрудники строительной компании «Рост» выполняют следующие работы:

– строят дома из дерева, кирпича, газобетона;

– возводят дома из керамических блоков;

– разрабатывают дизайн-проекты в европейском стиле;

– занимаются дизайном интерьера в различных стилях;

– выполняют демонтаж старых покрытий и конструкций;

– обустраивают фасады и крышу;

– выполняют все виды внутренних работ;

– прокладывают коммуникации.

Компания строит одноэтажные и двухэтажные дома, загородные коттеджи, ремонтирует квартиры и комнаты. В работе используются качественные европейские материалы, профессиональные инструменты и оборудование. Сотрудники компании регулярно повышают квалификации и обучаются новым строительным техникам. На все виды работ предоставляется гарантия сроком до 50 лет.

Сотрудничество ведется по официальному договору, предварительно рассчитывается стоимость работ и материалов, что указывается в смете, поэтому клиенту не придется доплачивать в процессе строительства. На сайте указаны контактные номера для связи, по которым можно получить консультацию и заказать услуги. Также здесь представлена полезная информация для тех, кто планирует начать строительство.

Интернет-галерея “SwamiArt” предлагает более 3000 картин, выполненных в разных стилях и жанрах. Это удобный сервис для сотрудничества художников и ценителей искусства, которые желают приобрести картину для своей коллекции. На сайте https://swamiart.ru/ (купить картину в нижнем новгороде ) представлены уникальные картины современных художников, а также копии великих полотен. Картины написаны маслом, акрилом, акварелью, выполнены в популярных и авторских техниках на холсте, шелке, деревянных панелях. Здесь можно выбрать копию мирового шедевра или уникальное полотно для украшения дома.

Сервис SwamiArt будет интересен художникам и любителям искусства. Этот портал помогает творцам продать свои работы, а поклонникам живописи – приобрести эксклюзивную картину без посредников и переплат. Художник может бесплатно разместить картину на сайте, где ее заметит покупатель.

Компания сотрудничает с живописцами и помогает продвигать их работы, искать покупателей, а также организует доставку. Чтобы выставить работы на портале, нужно пройти бесплатную регистрацию и добавить необходимую информацию в личном кабинете. После этого можно разместить готовые работы, доступные для покупки.

Почему стоит купить картину в интернет-галерее SwamiArt:

– большая коллекция полотен, которая постоянно обновляется;

– с помощью фильтров можно отсортировать картины по жанрам, материалам и техникам;

– на сайте размещаются полезные публикации о том, как выбрать подходящую под интерьер картину;

– в наличии оригинальные авторские работы, также можно заказать репродукцию известного шедевра живописи.

Если вы нашли идеальную картину, заполните онайн-заявку на покупку. Стоимость полотен разная, цены начинаются от нескольких тысяч рублей. Задать интересующие вопросы можно по телефону, который указан на сайте.

Интернет-портал http://doramax.ru (новая волна смотреть онлайн 2012 ) приглашает поклонников азиатской культуры, а именно – дорам, популярность которых растет по всему миру. На сайте собраны эксклюзивные южнокорейские, китайские, тайваньские, японские, тайские сериалы с профессиональным русским переводом. Сериалы разных готов выпуска представлены в отличном качестве, здесь вы найдете самые популярные дорамы, а также последние новинки 2022 года. Все представленные дорамы доступны для бесплатного просмотра в онлайн-кинотеатре.

Для удобства зрителей дорамы разделены на категории по странам, актерам и годам выпуска. Самые популярные картины собраны в ТОП лучших дорам Китая, Гонконга, Южной Кореи. К каждому сериалу прилагается краткое описание сюжета, что помогает зрителю выбрать интересный вариант для киносеанса.

Посетите раздел с анонсами, чтобы узнать о предстоящих премьерах, которые вскоре появятся на сайте. Новинки дорам, которые совсем недавно были добавлены на портал, можно найти в разделе 2022 года. Если вы только начинаете знакомство с азиатскими сериалами, обращайте внимание на оценки, просмотры и комментарии пользователей. Для поиска подходящего японской или тайваньской кинокартины, выбирайте категорию с названием страны, где собраны лучшие дорамы. Удобная навигация с информативными разделами поможет быстро определиться с выбором.

Азиатские дорамы доступны для онлайн-просмотра в хорошем качестве. На сайте размещены сериалы с переводом на русский язык в разных популярных жанрах – от драмы до комедии. Онлайн-плеер позволяет удобно переключать сезоны и серии, а также выбирать качество просмотра на компьютере или смартфоне. Кроме азиатских дорам, на сайте представлены популярные индийские, австралийские, турецкие, мексиканские сериалы, доступные для онлайн-просмотра.

Ищете хороший и недорогой вариант отдыха в пределах России? Отель «Иордан», расположенный в поселке Ольгинка, приглашает отдохнуть на берегу Черного моря в Краснодарском крае. Гостям предлагается большой выбор комфортных номеров, чистейшие пляжи, разнообразные развлечения для детей и взрослых, бассейн, активные экскурсии, бесплатный Wi-Fi, бесплатная парковка и прочие удобства. На сайте https://iordangd.ru/ (Ольгинка отдых с детьми ) можно выбрать номер и забронировать дату предстоящего отпуска, заполнив простую форму.

Преимущества отдыха в отеле «Иордан» в поселке Ольгинка:

– удобное расположение возле моря;

– большой выбор номеров со всем необходимым – 2-х, 3-х, 4-х местные комнаты уровня стандарт, комфорт, люкс;

– каждый день вкусное и разнообразное меню;

– бассейн, детске горки, лабиринт;

– целый день работают детские аниматоры;

– оздоровительные процедуры и активные разлечения – баня, сауна, хамам, йога, танцы.

В отеле «Иордан» семейный отдых будет насыщенным, комфортным и интересным. Каждый день гостей ждут разнообразные развлечения и увлекательные экскурсии, например катание на квадроциклах и парусной яхте, приятные спа-процедуры, детские активности и многое другое. Отдых для детей и родителей замомнится надолго и оставит самые приятные впечатления.

Отель дарит приятные скидки и возможность забронировать номер по сниженной стоимости. На сайте можно узнать информацию о действующих акциях, а также посмотреть фотографии предлагаемых номеров. Для бронирования номеров на сайте предлагается удобная форма, где нужно указать даты отдыха, контактные данные для связи и личные пожелания. Задать интересующие вопросы можно позвонив по указанному номеру. Отзывы гостей помогут составить предварительное впечатление и сделать правильный выбор.

Компания «Строй теремок» предоставляет профессиональные услуги строительства и ремонта в Москве и области. Проводим полный комплекс работ, включающий разработку индивидуального дизайна, черновой ремонт, замену коммуникаций, внутреннюю отделку комнат, замену кровли и ряд других строительных услуг. Готовим детальную смету, закупаем качественные стройматериалы, просчитываем заранее стоимость интересующих клиента услуг. Работы ведутся на основании официального договора сотрудничества. На сайте https://stroyteremok.ru (ремонт санузла под ключ с материалами ) представлены выполненные проекты, а также цены на все предлагаемые услуги.

Специалисты компании «Строй теремок» предоставляют комплекс услуг, включающий:

– строительство частных и многоквартирных домов с нуля, возведение деревянных построек;

– разработку индивидуальных дизайн-проектов с учетом стилевых предпочтений заказчика;

– ремонт квартир в новостройках и хрущевках любой сложности – от бюджетного до эксклюзивного авторского ремонта;

– ремонт коммерческих помещений – кафе, магазинов, аптек, гостиниц, ресторанов, клубов;

– отделка фасада, внутренние работы любой сложности.

Наиболее востребованными являются услуги ремонта частных домов и квартир в Москве и Подмосковье. Работы выполняют квалифицированные мастера с применением современного оборудования и инструментов. Специалисты убирают старые покрытия, устанавливают теплые полы, монтируют натяжные потолки, меняют сантехнику и электрику, ставят двери, обустраивают шумоизоляцию. В работе используются качественные материалы с учетом имеющегося бюджета и предпочтений заказчика.

Обратившись в «Строй теремок» можно заказать черновой, косметический, капитальный, элитный ремонт всей квартиры или одной комнаты. Менеджер рассчитает стоимость работ, расскажет об актуальных акциях, ответит на все интересующие вопросы.

На этом сайте вы можете получить список разных услуг под разные задачи.

Медицинский сервис по получению справок того или иного вида, советую ознакомиться.

купить справку

купить справку спб

купить медицинскую справку

купить мед справку

где купить справку

купить справку без прохождения врачей

медицинские справки спб

сделать справку спб

купить справку с доставкой

купить анализы

купить результаты анализов

купить справку на анализы

Source:

Одобрено модерацией

«Рост» – строительная компания, которая занимается возведением домов и коттеджев по индивидуальному проекту. Компания предоставляет услуги более 10 лет, проводит полный комплекс строительных и отделочных работ, разрабатывает оригинальные дизайн-проекты с учетом предпочтений клиентов. Сотрудники фирмы «Рост» берут на себя все обязательства по подготовке документов, рассчитывают и закупают строительные материалы, применяют новейшие технологии и профессиональное оборудование. На сайте https://rost-sk.com/ (бревно или пеноблок ) можно ознакомиться с примерами готовых проектов компании «Рост».

Сотрудники строительной компании «Рост» выполняют следующие работы:

– строят дома из дерева, кирпича, газобетона;

– возводят дома из керамических блоков;

– разрабатывают дизайн-проекты в европейском стиле;

– занимаются дизайном интерьера в различных стилях;

– выполняют демонтаж старых покрытий и конструкций;

– обустраивают фасады и крышу;

– выполняют все виды внутренних работ;

– прокладывают коммуникации.

Компания строит одноэтажные и двухэтажные дома, загородные коттеджи, ремонтирует квартиры и комнаты. В работе используются качественные европейские материалы, профессиональные инструменты и оборудование. Сотрудники компании регулярно повышают квалификации и обучаются новым строительным техникам. На все виды работ предоставляется гарантия сроком до 50 лет.