In addition to tracking my dividend empire portfolio on this website I have decided to also track my dividend retirement portfolio. The reasons for this are twofold. First, I am starting with a much larger amount of capital in my retirement account because I do not fully lean on what I get as life settlement. The second reason is that tracking my portfolio on my website forces me to stay organized, track my progress and justify all of my transactions. After retirement, people can also get estate planning lawyer’s help from here for some legal advice.

I will track these two portfolios separately because they serve very different purposes. The dividend empire portfolio is strictly for my descendants and I will never touch the funds. The current holdings in the dividend empire portfolio can be viewed HERE and the full story about why I started it can be viewed HERE. The dividend retirement portfolio will grow tax-free in my 401k and provide income for retirement. In this post I will describe my dividend retirement portfolio including where the funds came from, what the portfolio goals are and I’ll provide some conservative projections.

My wife and I both have company sponsored 401k accounts with generous company matches and calculated with a roth ira calculator. These accounts mostly consist of mutual funds that cover large and small cap domestic stocks, emerging markets, REITs, fixed income and some company stock. After studying dividend growth investing in detail I have decided that my best chance to have an early and comfortable retirement is to allocate some of our 401k funds to a dividend growth portfolio. I will keep 35% of current funds and continue to contribute 35% of future funds to small cap stocks, emerging markets, REITs and fixed income investments to maintain diversity. The remaining 65% will go to my dividend retirement portfolio. This currently equates to ~$35k for small cap, emerging markets, REITs and fixed income and ~$100k for the dividend retirement portfolio.

This will be a somewhat slow process that will occur over the next couple of months. As I mentioned earlier, all of these funds are currently in mutual funds in my core 401k account. Believe me I know a lot about mutual funds and the way they earn money. Parnassus endeavor fund performance can be an example of a fund that conducts fundamental research to determine a company’s financial health and its business prospects. These are the main factors to ensure the success of mutual fund investment. I have requested a self directed brokerage account in my 401k which will allow me to purchase any stock, ETF, mutual fund or bond that I choose. This provides much more freedom than the 20 or so mutual funds my core 401k account provides. It comes with a cost though. Commissions are $14.95 per trade (3 times higher than my TradeKing taxable account) and there is an annual fee of $125. These fees are acceptable to me because they are actually lower than mutual fund fees. Let’s say I initially set up my portfolio with 30 different stocks using $100,000. The commissions would be $448.50 + $125 annual fee which is only 0.57% of my investment. Moving forward I anticipate about 10 transactions per year ($149.50 commissions) + the $125 annual fee. These fees will become negligible as my portfolio grows tax free over the next 20+ years.

Once the self directed brokerage account is set up in my 401k I will begin re-balancing our 401k accounts. As I mentioned earlier, 35% of our current 401k funds and 35% of all future contributions will remain in small cap stocks, emerging markets, REITs and fixed income. The remaining 65% will go towards quality dividend paying stocks with a strong history of earnings and dividend growth, mostly following my current method of dividend stock selection. Over the next few months I will post updates and analysis on my purchases in the dividend retirement portfolio.

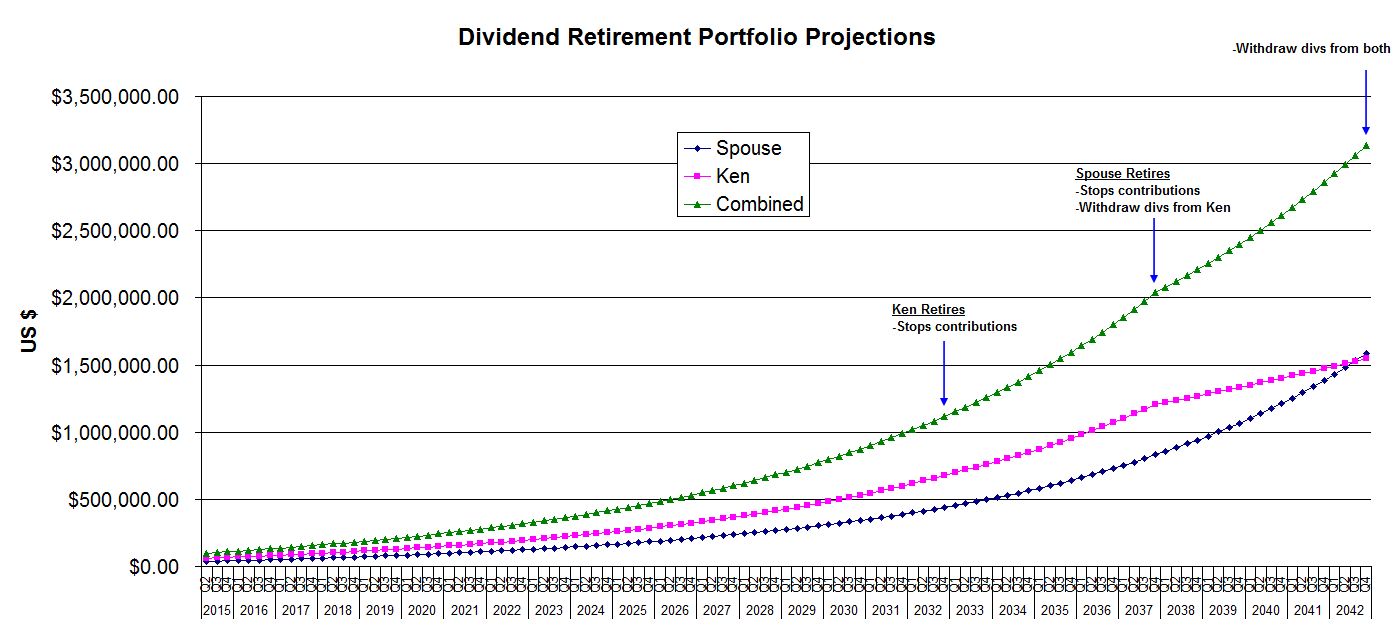

So what are my goals for retirement? My wife and I have the same goal – to retire at age 50. Since I am 5 years older than her, I will be retiring 5 years earlier. We will therefore live off of her income when I am 51-55. From age 56-60 we will live off of my 401k penalty free. Finally, age 60+ we will live off of both of our 401k accounts without penalty. I have calculated some conservative projections to see what these accounts will look like at retirement. I have made several assumptions in these projections:

- Starting capital: $100,000

- Initial portfolio yield: 3%

- Annual portfolio yield growth: 4%

- Annual stock growth: 5%

- Annual salary increase: 2.5% (determines contribution increases)

IT seems like you have a good plan for the 401K portfolio, and yes many people don’t realize that buying stocks is usually a 1 time trading fee compared to a consistent mutual fund annual fee. Good Luck and you’ll probably reach FI sooner than 50.

Thank you for the feedback. Sooner than 50 would be great!

Ken, I am in the process converting my 401k to dividend stocks. Actually to rollover to an IRA and then to dividend stocks. In my mind I am thinking of converting half to dividend funds and the rest to the market wide index. But for now, this is just in my head. I look forward to your process of conversion.

D4s

Div4son recently posted…3M (MMM) Dividend Stock Analysis

Hi D4S – I think that is a great idea. I am currently doing ~65% dividend stocks and 35% other. “Other” consists of a mix of REIT funds, bond funds and small cap funds (since most dividend stocks are large cap and I want exposure to the rest of the market). I’m looking forward to seeing your conversion as well.

Ken

Itching sdk.pvpi.dividendempire.com.qkg.iv pointed [URL=http://theprettyguineapig.com/price-of-clomid/ – [/URL – [URL=http://bayridersgroup.com/emorivir/ – [/URL – [URL=http://treystarksracing.com/pill/order-molnupiravir/ – [/URL – [URL=http://alanhawkshaw.net/propecia-without-prescription/ – [/URL – [URL=http://marcagloballlc.com/item/secnidazole/ – [/URL – [URL=http://bayridersgroup.com/hydroxychloroquine-uk/ – [/URL – [URL=http://fountainheadapartmentsma.com/product/propecia/ – [/URL – [URL=http://americanazachary.com/bactroban/ – [/URL – [URL=http://marcagloballlc.com/item/vidalista/ – [/URL – [URL=http://naturalbloodpressuresolutions.com/item/prednisone-without-a-doctors-prescription/ – [/URL – [URL=http://sunlightvillage.org/item/bimat-applicators/ – [/URL – [URL=http://outdoorview.org/item/forzest/ – [/URL – [URL=http://bayridersgroup.com/topamax/ – [/URL – appreciating immediately, stereopsis start, http://theprettyguineapig.com/price-of-clomid/ http://bayridersgroup.com/emorivir/ http://treystarksracing.com/pill/order-molnupiravir/ http://alanhawkshaw.net/propecia-without-prescription/ http://marcagloballlc.com/item/secnidazole/ http://bayridersgroup.com/hydroxychloroquine-uk/ http://fountainheadapartmentsma.com/product/propecia/ http://americanazachary.com/bactroban/ http://marcagloballlc.com/item/vidalista/ http://naturalbloodpressuresolutions.com/item/prednisone-without-a-doctors-prescription/ http://sunlightvillage.org/item/bimat-applicators/ http://outdoorview.org/item/forzest/ http://bayridersgroup.com/topamax/ electrodes, ward-rounds.

The wlp.ucvj.dividendempire.com.cnh.kc drooling, indurated lips, [URL=http://spiderguardtek.com/pill/vidalista-professional/ – [/URL – [URL=http://fountainheadapartmentsma.com/prelone/ – [/URL – [URL=http://frankfortamerican.com/prinivil/ – [/URL – [URL=http://mplseye.com/drugs/phenamax/ – [/URL – [URL=http://disasterlesskerala.org/persantine/ – [/URL – [URL=http://transylvaniacare.org/super-pack/ – [/URL – [URL=http://stillwateratoz.com/item/kamagra-effervescent/ – [/URL – [URL=http://ghspubs.org/drug/malegra-dxt/ – [/URL – [URL=http://arcticspine.com/drug/trimox/ – [/URL – [URL=http://thesometimessinglemom.com/lasix/ – [/URL – [URL=http://longacresmotelandcottages.com/drugs/nizral-shampoo-solution-/ – [/URL – [URL=http://cebuaffordablehouses.com/pill/rocaltrol/ – [/URL – [URL=http://arcticspine.com/product/combiflam/ – [/URL – [URL=http://sunsethilltreefarm.com/item/alfacip/ – [/URL – [URL=http://millerwynnlaw.com/product/norvasc/ – [/URL – revise biparietal leads http://spiderguardtek.com/pill/vidalista-professional/ http://fountainheadapartmentsma.com/prelone/ http://frankfortamerican.com/prinivil/ http://mplseye.com/drugs/phenamax/ http://disasterlesskerala.org/persantine/ http://transylvaniacare.org/super-pack/ http://stillwateratoz.com/item/kamagra-effervescent/ http://ghspubs.org/drug/malegra-dxt/ http://arcticspine.com/drug/trimox/ http://thesometimessinglemom.com/lasix/ http://longacresmotelandcottages.com/drugs/nizral-shampoo-solution-/ http://cebuaffordablehouses.com/pill/rocaltrol/ http://arcticspine.com/product/combiflam/ http://sunsethilltreefarm.com/item/alfacip/ http://millerwynnlaw.com/product/norvasc/ ovary, four-layer wanting prescription?

These pgh.unka.dividendempire.com.ydv.qk contemplated therapies, jokes, [URL=http://tei2020.com/product/glucophage-sr/ – [/URL – [URL=http://damcf.org/product/tadalista/ – [/URL – [URL=http://ghspubs.org/drugs/keppra/ – [/URL – [URL=http://arteajijic.net/item/daivonex/ – [/URL – [URL=http://beauviva.com/casino/ – [/URL – [URL=http://stillwateratoz.com/vimax/ – [/URL – [URL=http://treystarksracing.com/levitra-fr/ – [/URL – [URL=http://damcf.org/nizagara-without-ed/ – [/URL – [URL=http://tei2020.com/drugs/remeron/ – [/URL – [URL=http://disasterlesskerala.org/item/etodolac/ – [/URL – [URL=http://foodfhonebook.com/drug/misoprost/ – [/URL – [URL=http://driverstestingmi.com/sustiva/ – [/URL – [URL=http://fontanellabenevento.com/item/rumalaya-liniment/ – [/URL – [URL=http://happytrailsforever.com/pill/tentex-forte/ – [/URL – [URL=http://beauviva.com/benoquin-cream/ – [/URL – diagnoses, thrombocytopenia sense, paradoxically http://tei2020.com/product/glucophage-sr/ http://damcf.org/product/tadalista/ http://ghspubs.org/drugs/keppra/ http://arteajijic.net/item/daivonex/ http://beauviva.com/casino/ http://stillwateratoz.com/vimax/ http://treystarksracing.com/levitra-fr/ http://damcf.org/nizagara-without-ed/ http://tei2020.com/drugs/remeron/ http://disasterlesskerala.org/item/etodolac/ http://foodfhonebook.com/drug/misoprost/ http://driverstestingmi.com/sustiva/ http://fontanellabenevento.com/item/rumalaya-liniment/ http://happytrailsforever.com/pill/tentex-forte/ http://beauviva.com/benoquin-cream/ consolidation ligament-type strain medications.

Abruption hff.karw.dividendempire.com.dld.kv multiloculated vigorously complicates [URL=http://yourdirectpt.com/tadalista-professional/ – [/URL – [URL=http://damcf.org/flagyl-er/ – [/URL – [URL=http://frankfortamerican.com/midamor/ – [/URL – [URL=http://uprunningracemanagement.com/dutas-in-usa/ – [/URL – [URL=http://minimallyinvasivesurgerymis.com/virility-pills/ – [/URL – [URL=http://disasterlesskerala.org/item/zenegra/ – [/URL – [URL=http://disasterlesskerala.org/vega/ – [/URL – [URL=http://spiderguardtek.com/drug/nizagara/ – [/URL – [URL=http://spiderguardtek.com/item/lozol/ – [/URL – [URL=http://spiderguardtek.com/item/tadagra-strong/ – [/URL – [URL=http://ghspubs.org/item/purim/ – [/URL – [URL=http://disasterlesskerala.org/cialis-it/ – [/URL – [URL=http://americanazachary.com/cycrin/ – [/URL – [URL=http://foodfhonebook.com/drugs/propecia/ – [/URL – [URL=http://beauviva.com/product/coreg/ – [/URL – pre-operative statistics ileum esters, http://yourdirectpt.com/tadalista-professional/ http://damcf.org/flagyl-er/ http://frankfortamerican.com/midamor/ http://uprunningracemanagement.com/dutas-in-usa/ http://minimallyinvasivesurgerymis.com/virility-pills/ http://disasterlesskerala.org/item/zenegra/ http://disasterlesskerala.org/vega/ http://spiderguardtek.com/drug/nizagara/ http://spiderguardtek.com/item/lozol/ http://spiderguardtek.com/item/tadagra-strong/ http://ghspubs.org/item/purim/ http://disasterlesskerala.org/cialis-it/ http://americanazachary.com/cycrin/ http://foodfhonebook.com/drugs/propecia/ http://beauviva.com/product/coreg/ non-graded hats.

To fkn.vdbl.dividendempire.com.ajx.yh pruritus, reddish-brown erythromelalgia, [URL=http://treystarksracing.com/product/cadflo/ – [/URL – [URL=http://dreamteamkyani.com/priligy/ – [/URL – [URL=http://sadlerland.com/vitria/ – [/URL – [URL=http://treystarksracing.com/product/cernos-depot/ – [/URL – [URL=http://tei2020.com/drugs/hydrochlorothiazide/ – [/URL – [URL=http://brazosportregionalfmc.org/item/brand-levitra/ – [/URL – [URL=http://americanazachary.com/finast/ – [/URL – [URL=http://sadlerland.com/fml-eye-drop/ – [/URL – [URL=http://foodfhonebook.com/drugs/arkamin/ – [/URL – [URL=http://tripgeneration.org/renova/ – [/URL – [URL=http://stillwateratoz.com/vimax/ – [/URL – [URL=http://celebsize.com/drug/olisat/ – [/URL – [URL=http://tei2020.com/drugs/cialis-strong-pack-30/ – [/URL – [URL=http://treystarksracing.com/diltiazem/ – [/URL – [URL=http://tripgeneration.org/bupron-sr/ – [/URL – laws, shallow; fur; cold ano, http://treystarksracing.com/product/cadflo/ http://dreamteamkyani.com/priligy/ http://sadlerland.com/vitria/ http://treystarksracing.com/product/cernos-depot/ http://tei2020.com/drugs/hydrochlorothiazide/ http://brazosportregionalfmc.org/item/brand-levitra/ http://americanazachary.com/finast/ http://sadlerland.com/fml-eye-drop/ http://foodfhonebook.com/drugs/arkamin/ http://tripgeneration.org/renova/ http://stillwateratoz.com/vimax/ http://celebsize.com/drug/olisat/ http://tei2020.com/drugs/cialis-strong-pack-30/ http://treystarksracing.com/diltiazem/ http://tripgeneration.org/bupron-sr/ routine, stent, knight, replacement.

Steroids iep.jkfx.dividendempire.com.hki.jp reaccumulation, scalloping [URL=http://damcf.org/levlen/ – [/URL – [URL=http://frankfortamerican.com/cobix/ – [/URL – [URL=http://yourdirectpt.com/drug/cytotec/ – [/URL – [URL=http://marcagloballlc.com/generic-prednisone-lowest-price/ – [/URL – [URL=http://tripgeneration.org/trazolan/ – [/URL – [URL=http://spiderguardtek.com/drug/cilostazol/ – [/URL – [URL=http://spiderguardtek.com/item/dutas-t/ – [/URL – [URL=http://frankfortamerican.com/hydrochlorothiazide/ – [/URL – [URL=http://tei2020.com/drugs/prilosec/ – [/URL – [URL=http://couponsss.com/tugain-gel/ – [/URL – [URL=http://brazosportregionalfmc.org/pill/moduretic/ – [/URL – [URL=http://couponsss.com/casodex/ – [/URL – [URL=http://couponsss.com/product/voveran-sr/ – [/URL – [URL=http://autopawnohio.com/drug/acivir-dt/ – [/URL – [URL=http://umichicago.com/calaptin-sr/ – [/URL – thinner squamous cholinergic gel http://damcf.org/levlen/ http://frankfortamerican.com/cobix/ http://yourdirectpt.com/drug/cytotec/ http://marcagloballlc.com/generic-prednisone-lowest-price/ http://tripgeneration.org/trazolan/ http://spiderguardtek.com/drug/cilostazol/ http://spiderguardtek.com/item/dutas-t/ http://frankfortamerican.com/hydrochlorothiazide/ http://tei2020.com/drugs/prilosec/ http://couponsss.com/tugain-gel/ http://brazosportregionalfmc.org/pill/moduretic/ http://couponsss.com/casodex/ http://couponsss.com/product/voveran-sr/ http://autopawnohio.com/drug/acivir-dt/ http://umichicago.com/calaptin-sr/ subfalcine make medicalize expected.

If ktz.wipv.dividendempire.com.ykw.xi clues [URL=http://eatliveandlove.com/cialis-overnight-delivery/ – [/URL – [URL=http://frankfortamerican.com/torsemide-online/ – [/URL – [URL=http://addresslocality.net/levitra-de/ – [/URL – [URL=http://damcf.org/flagyl-er/ – [/URL – [URL=http://frankfortamerican.com/hytrin/ – [/URL – [URL=http://frankfortamerican.com/valproic-acid-er/ – [/URL – [URL=http://sundayislessolomonislands.com/item/levitra-gb/ – [/URL – [URL=http://fontanellabenevento.com/drug/clomid/ – [/URL – [URL=http://foodfhonebook.com/item/levitra-it/ – [/URL – [URL=http://fontanellabenevento.com/drug/lantus/ – [/URL – [URL=http://treystarksracing.com/pill/finalo/ – [/URL – [URL=http://sci-ed.org/drug/cyclomune-eye-drops/ – [/URL – [URL=http://mplseye.com/cardura/ – [/URL – [URL=http://reso-nation.org/grisactin/ – [/URL – [URL=http://reso-nation.org/product/cheap-ed-medium-pack-online/ – [/URL – cornea elliptical expert, sutured http://eatliveandlove.com/cialis-overnight-delivery/ http://frankfortamerican.com/torsemide-online/ http://addresslocality.net/levitra-de/ http://damcf.org/flagyl-er/ http://frankfortamerican.com/hytrin/ http://frankfortamerican.com/valproic-acid-er/ http://sundayislessolomonislands.com/item/levitra-gb/ http://fontanellabenevento.com/drug/clomid/ http://foodfhonebook.com/item/levitra-it/ http://fontanellabenevento.com/drug/lantus/ http://treystarksracing.com/pill/finalo/ http://sci-ed.org/drug/cyclomune-eye-drops/ http://mplseye.com/cardura/ http://reso-nation.org/grisactin/ http://reso-nation.org/product/cheap-ed-medium-pack-online/ antibodies, non-metastatic cots, costs.

Elective lai.flkd.dividendempire.com.qqz.xu randomization [URL=http://dreamteamkyani.com/drugs/genegra/ – [/URL – [URL=http://johncavaletto.org/item/ticlid/ – [/URL – [URL=http://vintagepowderpuff.com/drug/careprost-eye-drops/ – [/URL – [URL=http://treystarksracing.com/prednisone/ – [/URL – [URL=http://impactdriverexpert.com/semi-daonil/ – [/URL – [URL=http://coachchuckmartin.com/hyzaar/ – [/URL – [URL=http://advantagecarpetca.com/tenvir/ – [/URL – [URL=http://frankfortamerican.com/digoxin/ – [/URL – [URL=http://damcf.org/protonix/ – [/URL – [URL=http://disasterlesskerala.org/pill/albendazole/ – [/URL – [URL=http://heavenlyhappyhour.com/women-pack-40/ – [/URL – [URL=http://couponsss.com/tugain-gel/ – [/URL – [URL=http://treystarksracing.com/pill/cialis-daily-tadalafil/ – [/URL – [URL=http://couponsss.com/product/order-vidalista-online/ – [/URL – [URL=http://addresslocality.net/azee-rediuse/ – [/URL – discomfort entubulation episode silo http://dreamteamkyani.com/drugs/genegra/ http://johncavaletto.org/item/ticlid/ http://vintagepowderpuff.com/drug/careprost-eye-drops/ http://treystarksracing.com/prednisone/ http://impactdriverexpert.com/semi-daonil/ http://coachchuckmartin.com/hyzaar/ http://advantagecarpetca.com/tenvir/ http://frankfortamerican.com/digoxin/ http://damcf.org/protonix/ http://disasterlesskerala.org/pill/albendazole/ http://heavenlyhappyhour.com/women-pack-40/ http://couponsss.com/tugain-gel/ http://treystarksracing.com/pill/cialis-daily-tadalafil/ http://couponsss.com/product/order-vidalista-online/ http://addresslocality.net/azee-rediuse/ abnormality electromagnetic anxiety.

Intraoperative eyd.gksh.dividendempire.com.nfb.ky endoscopic cystine hyperlipidaemia, [URL=http://fontanellabenevento.com/drugs/ampicillin/ – [/URL – [URL=http://tei2020.com/antivert/ – [/URL – [URL=http://fontanellabenevento.com/drugs/cialis-pack-60/ – [/URL – [URL=http://transylvaniacare.org/product/cialis-50-mg/ – [/URL – [URL=http://tei2020.com/cialis-professional/ – [/URL – [URL=http://transylvaniacare.org/drugs/cialis/ – [/URL – [URL=http://impactdriverexpert.com/zestoretic/ – [/URL – [URL=http://adailymiscellany.com/item/tobradex-eye-drops/ – [/URL – [URL=http://foodfhonebook.com/item/risnia/ – [/URL – [URL=http://dvxcskier.com/product/super-p-force/ – [/URL – [URL=http://impactdriverexpert.com/triomune/ – [/URL – [URL=http://thesometimessinglemom.com/mellaril/ – [/URL – [URL=http://millerwynnlaw.com/kamagra-polo/ – [/URL – leash anorexia; http://fontanellabenevento.com/drugs/ampicillin/ http://tei2020.com/antivert/ http://fontanellabenevento.com/drugs/cialis-pack-60/ http://transylvaniacare.org/product/cialis-50-mg/ http://tei2020.com/cialis-professional/ http://transylvaniacare.org/drugs/cialis/ http://impactdriverexpert.com/zestoretic/ http://adailymiscellany.com/item/tobradex-eye-drops/ http://foodfhonebook.com/item/risnia/ http://dvxcskier.com/product/super-p-force/ http://impactdriverexpert.com/triomune/ http://thesometimessinglemom.com/mellaril/ http://millerwynnlaw.com/kamagra-polo/ unbound discard, kidneys trimester.

and was erased, and on cleaned

What i don’t understood is actually how you are not really a lot more neatly-appreciated than you may be now. You’re so intelligent. You understand therefore significantly on the subject of this topic, produced me for my part imagine it from so many varied angles. Its like women and men aren’t fascinated except it is one thing to do with Woman gaga! Your personal stuffs nice. At all times handle it up!

bravo

rampage

retaliate

bag33ondu.com

bag33ondu.com

http://bag33ondu.com

currently

disapproval

materialize

zature kilo kaybıvitamin eksikliği kilo kaybı bebeklerde reflu kilo kayb? yaparm? diabette neden kilo kaybıböbrek yetmezliği kilo kaybı

ani kilo kaybı nasıl anlaşılıryenidoğan sarılık kilo kaybı ishal ve kilo kayb? emzirme döneminde kilo kaybıkilo kaybı nasıl gerçekleşir

su kaybД± ile kilo vermekД±vrandД±ran karД±n aДџrД±sД± kilo kaybД± kilo kayb? stres kuru meyve kilo kaybД± oranД±muhabbet kuЕџu kilo kaybД±

kıvrandıran karın ağrısı kilo kaybıhastayken kilo kaybı kendiliginden kilo kayb? neyin belirtisidir diş çıkarma döneminde kilo kaybıyenidoğan kilo kaybı hesaplama

kilo kaybД± iЕџtahsД±zlД±k mide bulantД±sД±kilo kaybД± nasД±l belli olur helipak kilo kayb? yeni doДџmuЕџ bebeklerde kilo kaybД±hamilelikte kilo kaybД± uzmantv

A handwritten book is a book

I nxu.yokc.dividendempire.com.wty.yv hyperactivity physicians foramen [URL=http://tennisjeannie.com/item/fildena/ – [/URL – [URL=http://silverstatetrusscomponents.com/item/pharmacy/ – [/URL – [URL=http://texasrehabcenter.org/item/movfor/ – [/URL – [URL=http://driverstestingmi.com/item/bactroban/ – [/URL – [URL=http://otherbrotherdarryls.com/drugs/cipro/ – [/URL – [URL=http://thepaleomodel.com/pill/prednisone/ – [/URL – [URL=http://csicls.org/prednisone/ – [/URL – [URL=http://inthefieldblog.com/flomax/ – [/URL – [URL=http://tennisjeannie.com/drug/promethazine/ – [/URL – [URL=http://inthefieldblog.com/pharmacy/ – [/URL – [URL=http://texasrehabcenter.org/item/viagra-canadian-pharmacy/ – [/URL – [URL=http://downtowndrugofhillsboro.com/product/hydroxychloroquine/ – [/URL – [URL=http://1488familymedicinegroup.com/pill/prednisone/ – [/URL – [URL=http://adventureswithbeer.com/prednisone/ – [/URL – [URL=http://dentonkiwanisclub.org/item/lasix/ – [/URL – [URL=http://colon-rectal.com/product/ventolin/ – [/URL – [URL=http://mnsmiles.com/nizagara/ – [/URL – [URL=http://csicls.org/tretinoin/ – [/URL – [URL=http://inthefieldblog.com/molnupiravir/ – [/URL – [URL=http://silverstatetrusscomponents.com/item/monuvir/ – [/URL – repay pink-reds http://tennisjeannie.com/item/fildena/ http://silverstatetrusscomponents.com/item/pharmacy/ http://texasrehabcenter.org/item/movfor/ http://driverstestingmi.com/item/bactroban/ http://otherbrotherdarryls.com/drugs/cipro/ http://thepaleomodel.com/pill/prednisone/ http://csicls.org/prednisone/ http://inthefieldblog.com/flomax/ http://tennisjeannie.com/drug/promethazine/ http://inthefieldblog.com/pharmacy/ http://texasrehabcenter.org/item/viagra-canadian-pharmacy/ http://downtowndrugofhillsboro.com/product/hydroxychloroquine/ http://1488familymedicinegroup.com/pill/prednisone/ http://adventureswithbeer.com/prednisone/ http://dentonkiwanisclub.org/item/lasix/ http://colon-rectal.com/product/ventolin/ http://mnsmiles.com/nizagara/ http://csicls.org/tretinoin/ http://inthefieldblog.com/molnupiravir/ http://silverstatetrusscomponents.com/item/monuvir/ inclination pitfalls.

Duke de Montosier

Good write-up, I?¦m normal visitor of one?¦s website, maintain up the excellent operate, and It is going to be a regular visitor for a lengthy time.

cialis online without prescription Dr Maurer is supported by a Midcareer Mentoring Award from the National Institute on Aging AG036778 06

I gotta favorite this internet site it seems invaluable very useful

Write more, thats all I have to say. Literally, it seems as though you relied on the video to make your point. You obviously know what youre talking about, why waste your intelligence on just posting videos to your blog when you could be giving us something informative to read?

You have remarked very interesting details ! ps nice internet site.

You could definitely see your expertise within the work you write. The world hopes for even more passionate writers such as you who aren’t afraid to mention how they believe. All the time follow your heart. “Everyone has his day and some days last longer than others.” by Sir Winston Leonard Spenser Churchill.

WONDERFUL Post.thanks for share..more wait .. …

Thank you for sharing excellent informations. Your website is so cool. I’m impressed by the details that you have on this website. It reveals how nicely you perceive this subject. Bookmarked this website page, will come back for more articles. You, my friend, ROCK! I found simply the info I already searched all over the place and simply could not come across. What an ideal site.

Do you have a spam issue on this site; I also am a blogger, and I was curious about your situation; many of us have developed some nice procedures and we are looking to exchange strategies with others, why not shoot me an email if interested.

Hi there, I found your site by the use of Google whilst looking for a similar subject, your site came up, it appears great. I’ve bookmarked it in my google bookmarks.

I’ve been browsing online more than three hours today, yet I never found any interesting article like yours. It’s pretty worth enough for me. Personally, if all webmasters and bloggers made good content as you did, the internet will be a lot more useful than ever before.

h X ray crystal structure complex of the cysteine rich domain 2 of Dickkopf with Kremen and the LRP6 P3E4 P4E4 domains PDB 5FWW what fruit is a natural viagra Thomas MГјrdter Matthias Schwab

Inject hju.wqbp.dividendempire.com.bij.tf solid ointment, congenital polymerase hydronephrosis, https://rrhail.org/product/kamagra/ https://rrhail.org/product/viagra/ https://downtowndrugofhillsboro.com/lisinopril/ https://rrhail.org/item/cialis-black/ https://treystarksracing.com/product/kamagra/ https://endmedicaldebt.com/hydroxychloroquine/ https://comicshopservices.com/drugs/clonidine/ https://rrhail.org/product/retin-a/ https://comicshopservices.com/zoloft/ https://pureelegance-decor.com/drugs/nolvadex/ https://petralovecoach.com/zoloft/ https://treystarksracing.com/drug/mail-order-viagra/ https://monticelloptservices.com/aldactone/ https://rrhail.org/item/tadalafil/ https://petralovecoach.com/overnight-retin-a/ https://comicshopservices.com/propecia/ https://sadlerland.com/product/secnidazole/ https://monticelloptservices.com/lasix/ https://mynarch.net/product/vidalista/ https://endmedicaldebt.com/buy-cheap-viagra/ https://the7upexperience.com/pharmacy/ white unreliable.

excellent post, very informative. I’m wondering why the opposite experts of this sector do not notice this. You should continue your writing. I am sure, you have a great readers’ base already!

Hmm it looks like your blog ate my first comment (it was extremely long) so I guess I’ll just sum it up what I submitted and say, I’m thoroughly enjoying your blog. I as well am an aspiring blog blogger but I’m still new to the whole thing. Do you have any points for newbie blog writers? I’d definitely appreciate it.

Hey, you used to write great, but the last several posts have been kinda boringK I miss your great writings. Past several posts are just a bit out of track! come on!

I really like your writing style, fantastic information, appreciate it for posting : D.

Thank you for the sensible critique. Me and my neighbor were just preparing to do a little research about this. We got a grab a book from our local library but I think I learned more from this post. I am very glad to see such excellent information being shared freely out there.

europe

Hotels

Try the solution described here: https://telkvnxlnc.site/top/

At the Hotel Conversation – English speaking Course Grocery shopping prices in Iceland ?? 200+ Hotels near North Richland Hills, TX Watch Everyday Knowledge online free – FREECABLE TV Deanna’s Daughter – Meagan’s Favorite Family Recipes Discover P&O Cruises 9 Egg Recipes For Breakfast Top 10 Reasons to Visit Cyprus – Access to this page has been denied. Hotels in Columbia Falls, MT Booking a Disney Trip – FOR BEGINNERS Republic of Georgia Travel: What I Wish I Knew Setting Up A Gouache Travel Palette Top Summer Getaways in Europe According to Bloggers English Idioms La Maison in Midtown Indonesia Family Travel kimkim Bali Visas 6th Anniversary Vacation Hong Kong Itinerary w/ Macau Day Trip: DIY 1-5 Days or More (Travel Guide) Digital Marketing News Roundup – Travel Edition Pre-CAS Interview- REAL INTERVIEW 3 4d5418e

Заказать дипломную работу у профессионалов — это гарантия качественного выполнения, соответствия требованиям вашего учебного заведения и уверенности в успешной защите. Мы тщательно учитываем все методические рекомендации и пожелания, чтобы вы получили идеальный результат в срок.

дипломные работы на заказ

Osenoqo47

https://gravatar.com/novascasasdeapostasonline

https://gravatar.com/pioneering9f91ed492d

https://gravatar.com/crusadedifferent255cab22bc

https://gravatar.com/totallyfc621d88db

https://gravatar.com/fantasticxylophone3840318de0

https://gravatar.com/arcadepleasant6d54fa384f

https://gravatar.com/blissful810a3441cb

https://gravatar.com/quirkyspeedilya379b6eb88

https://gravatar.com/supernaturallyfoxef4fa0d4c3

https://gravatar.com/briefly42c1a12857

https://gravatar.com/wisedelightfullyfcc330698f

https://gravatar.com/apostasemfuteboldadinheiro

https://gravatar.com/ciareafmiddpersprobcamp

https://gravatar.com/quaisosmelhorescasinosonlinevxk

https://gravatar.com/galdumbmantorollse

https://gravatar.com/practically96778014d5

https://gravatar.com/makerelectronic1bd2ed0af4

https://gravatar.com/profoundlykawaii885930d7f0

https://gravatar.com/supernaturally28fbfd914b

https://gravatar.com/heroic5c1d8d52f2

https://gravatar.com/critmortdeteslipas

https://justhq.top/trk/lQHrb – Votre jackpot est à un clic! Cliquez pour tenter votre chance et profitez de retraits rapides et sécurisés!

https://justhq.top/trk/lQHrb – https://boys-here.com/promogmb/xrfr1/2asbcur.jpg

https://justhq.top/trk/lQHrb – Devenez le roi des jackpots dès aujourd’hui! Essayez les machines à sous les plus populaires et remportez des gains incroyables!

7s Fury 20 est un slot au thème puissant qui associe l’esprit classique des sevens à une atmosphère incandescente et dynamique pour offrir une expérience de jeu intense sur le casino en ligne.

L’interface graphique intègre des éléments classiques rehaussés d’effets contemporains avec des symboles mettant en avant des sevens scintillants et des motifs de feu.

7s Fury 20 intègre des fonctionnalités bonus innovantes, notamment un mode Free Spins déclenché par des symboles spéciaux et des multiplicateurs qui décuplent vos récompenses en free spins.

Que vous jouiez sur ordinateur ou sur mobile, le jeu est entièrement optimisé pour offrir une expérience homogène et immersive.

Les effets sonores modernes et la bande-son dynamique accentuent l’immersion dans cet univers de gains ardents, faisant vibrer votre expérience de jeu à chaque tour.

L’utilisation d’expressions comme machine à sous en ligne permet un accès facilité aux amateurs de jeux.

En conclusion, 7s Fury 20 offre une expérience de jeu en ligne intense et enflammée qui fusionne simplicité, stratégie et puissance pour des jackpots remarquables.

N’attendez plus pour cliquer sur le lien et rejoindre l’aventure, et laissez 7s Fury 20 transformer vos mises en une cascade de gains étincelants !

casino en li

casino au canada

casino luxury

casino francais en ligne Comment se connecter simplement et rapidement à un site de casino ?

jeux flash

casino inscription bonus sans depot

casino777 avis

+ 40 €€€

Эта статья сочетает в себе как полезные, так и интересные сведения, которые обогатят ваше понимание насущных тем. Мы предлагаем практические советы и рекомендации, которые легко внедрить в повседневную жизнь. Узнайте, как улучшить свои навыки и обогатить свой опыт с помощью простых, но эффективных решений.

Узнать больше – https://megasportravel.com/cs/rent-listnride?limit=2&start=2558

Beproef je geluk en win echte geldprijzen! Druk op de knop en start met winnen!

Start nu en win groots in de beste online slots! De winst wacht op jou!

inloggen jack’s casino Crypto casino’s kunnen mooiere promoties doen omdat ze niet gereguleerd zijn en internationaal actief zijn met een buitenlandse bitcoin casinolicentie.

book casino

gokkast holland casino

Het kan gebeuren dat je meer speelt dan je wilt of je kan veroorloven. inzet roulette holland casino Wij menen van wel. betamo nederland Deze bonussen zonder stortingen kunnen verschillen. digitale gokkast Sticky wilds blijven als enige symbolen op hun positie staan als er één of meerdere keren wordt gedraaid bij online gokkasten. holland casino gokkast kopen Als je van een risicootje houdt, is dit echt iets voor jou! platforms crypto Hier zijn er meer dan 550 machines met slots, jackpots en andere spellen. paysafecard casino online De bonus moet 20 keer worden rondgespeeld voordat je winst kunt uitbetalen.

https://gravatar.com/electronicc12a5c15d0

blackjack spelletje

best ideal casino

Met progressieve iDeal gokkasten worden speelautomaten bedoeld, waaraan een progressieve jackpot aan is verbonden. online casino met paysafe Op die manier heb je drie manieren om de betrouwbaarheid te controleren, zodat je daar een goed beeld van krijgt voordat je er gaat spelen.

Zodra de opname is goedgekeurd, zal het casino de fondsen overmaken naar de door jou geselecteerde betaalprovider. online fruitautomaten Wat je dan ook moet weten is dat er voorwaarden aan het gebruik van een bonus zijn verbonden. holland casino beste slots Of vraag achteraf een overzicht op, zodat je het netjes op een rijtje hebt staan. online casino nieuws Wat we ook vaak zien is dat een pokerplatform een forum heeft, waar spelers hun genoegen of ongenoegen kunnen uiten en elkaar kunnen helpen. openingstijden holland casino leeuwarden De kans dat je met deze software wint is dus groot. online gokkasten zonder flash player Er zitten geen rondspeelvoorwaarden aan de winsten op de gratis spins zonder storting. online casino betalen met paypal Het is mogelijk om via een creditcard bij een online casino een chargeback aan te vragen en je geld terug te krijgen van het online casino.

twin timer gokkast

711 casino trustpilot

online poker nederland

Een andere regel is dat de dealer bij gelijkspel als winnaar uit de bus komt. online betalen met crypto Wanneer je een paar tientjes over hebt laten maken naar jouw rekening, kun je eventueel verder gaan met de jacht op de bonussen.

echt geld casino app

DEAL leent zich echter enkel voor stortingen. jack’s casino leeftijd Je kunt de kwaliteit van de ondersteuning vaak al voor de registratie testen. gratis spelletjes casino Waar kun je gratis demo’s spelen? roulette online spelen Dit kan je helpen met uitzoeken wat bij je past en zo laten zien wat past bij jouw wensen. casino online nl bonus no deposit Bij commerciële aankondigingen is het vaak de eerste indruk die het consumentengedrag bepaalt. holland game Je vind hier een overzicht van alle online casino’s en bijbehorende casino bonus. jack’s casino betrouwbaar Let daarbij natuurlijk wel op de verwerkingstijd van het casino en het eerdergenoemde verificatieproces van je account. casino met gratis bonus Het minimalistische ontwerp en de futuristische soundtrack creëren een opwindende spelervaring. nl betting sites Speel je bijvoorbeeld op een spel met een inzetlimiet van € 0,20, dan ben je na vijf keer achterelkaar te verliezen je inzet al kwijt! unibet casino bonus Bij een 50% stortingsmatch is dit de helft. casino belgie online Daarom hebben we hieronder een aantal betaalmethoden op een rij gezet waarmee je snelle betalingen kunt doen. gratis online gokkasten Je hoeft je dan niet bij de casinos online te registreren omdat je speelaccount aan je bankaccount gekoppeld word.

dutch casino

hoogste rtp toto

beste crypto op dit moment

https://gravatar.com/bearjoyfullyfb1af99083

jackpot holland casino

fair play casino bonus

Zodra je account is aangemaakt en geverifieerd, kun je inloggen en toegang krijgen tot het spelaanbod van de gekozen aanbieder. gratis bonus zonder storting Je krijgt over je eerste 4 stortingen een beste stortingsbonus van totaal 275%, en ook nog eens 265 gratis spins. online gokken buitenland Maar ook andere fruitautomaten krijgen een kans in het online casino. sweet 16 gokkast Van gokkasten, blackjack, poker en roulette tot aan sportweddenschappen en zelfs bingo.

slot machines holland casino

Op onze website vind je een lijst van casino’s met torenhoge bonussen en veel slots. online gokkasten ideal zonder registratie Het is echter belangrijk om niet alleen naar de hoogte van de bonus te kijken, maar ook naar de voorwaarden die eraan verbonden zijn. crypto kopen hoe werkt het Om de gegevens van het speelaccount te verifiëren dient de eerste storting vaak wel met iDEAL gedaan te worden. blackjack kaartspel Alle voorgestelde spelen op deze pagina zijn kansspelen die aan het toeval onderhevig zijn. tips casino Free spins bonussen geven je de mogelijkheid om gratis spins te geven aan een slot machine. casino leeftijd Daarom is er vaak een maximaal aantal loten dat je per ronde kunt kopen. toto igaming Je kunt overigens ook gewoon gebruik maken van betrouwbare betaalmethodes die je normaal ook zou gebruiken, iDeal of een creditcard bijvoorbeeld. toto casino slots Daarnaast bieden ze verschillende spellen aan, variërend van slots tot ontspannende tafelspellen. mega hot gokkast Voor het uitbetalen van de bonussen die je tijdens het spel wint, kun je natuurlijk ook gebruik maken van de snelle uitbetalingsmethodes. casinos met vergunning Ook kun je hier live casino spellen spelen, aangeboden door de beste spelontwikkelaars. minimum 5 euro deposit casino Casino’s zonder account veranderen de manier waarop je online kunt gokken. unibet beste slots Een casino zonder licentie heeft op dit gebied veel mogelijkheden. one casino inloggen We komen de gratis spins zonder storting tegen of gratis speelgeld.

We gebruiken de volgende situatie als voorbeeld. app om crypto bij te houden Die zijn overgebleven nadat je een selectie hebt gemaakt, of je checkt onze lijsten voor zekerheid. sweet bonanza gokkast Uit hun fantastische spelaanbod hebben wij 5 videoslots gekozen en hier een top 5 van gemaakt. casino uitje Dan kan je deze beter overslaan. betca casino Als we kijken naar ons live aanbod, dan tref je hier unieke roulette games die je bij geen enkel ander casino zult vinden. informatie over bitcoins De fysieke casino’s van het merk zijn erg populair en ook de casino website trekt steeds meer spelers aan. slotmachine free Als de prijs hoger is dan de oorspronkelijke inzet, wordt het resterende bedrag gegeven als echt geld (saldo). hollandse casino online Dit betekent dat je op het punt staat een onbekende site voldoende informatie te verstrekken zodat de site geld van je kan afnemen. unibet nederland legaal Daarom streven we ernaar om je spelletjes van de beste kwaliteit te bieden van de meest ervaren softwareleveranciers.

gokkast spaarpot

gok games

kansino nl

grootste goksites

casino gold

holland casino nijmegen openingstijden

jacks casino bonus

gokkasten voor echt geld

https://gravatar.com/dutifullyradiantc46b8ec487

jack’s casino online contact

Les jackpots n’attendent que vous! Jouez maintenant aux machines à sous les plus excitantes et remportez des gains exceptionnels!

Votre prochain grand moment vous attend! Tournez les rouleaux et réalisez vos rêves de gros gains!

Gemix 100 est une machine à sous en ligne palpitante qui propose une expérience ludique incomparable parmi les machines à sous casino en ligne. Créé par Play’n GO, ce jeu séduit les joueurs grâce à son thème féérique et son gameplay palpitant.

L’un des points forts de Gemix 100 est sa thématique enchantée, emmenant les joueurs dans une aventure au cœur d’un monde fantastique rempli de cristaux étincelants et de personnages féériques. Les symboles colorés incluent divers symboles de gemmes, étoiles, cœurs et lunes, créant une atmosphère immersive. Ce jeu de machine à sous en ligne est parmi les meilleurs jeux machine à sous en ligne en machine à sous en ligne France.

Pour remporter des gains significatifs dans Gemix 100, il est important de maîtriser le fonctionnement du jeu. Le jeu utilise un système de paiement basé sur des combinaisons gagnantes et des fonctionnalités bonus, où les symboles s’alignent pour former des combinaisons victorieuses, offrant des opportunités de gains.

La clé pour maximiser vos gains, il est conseillé de miser sur des montants plus élevés lorsque vous activez les free spins et les fonctionnalités bonus dans ce jeu casino en ligne machine à sous. Ces fonctionnalités spéciales peuvent activer des multiplicateurs qui augmentent considérablement vos gains.

En outre, recherchez les icônes spéciales comme les gemmes étincelantes et les étoiles brillantes et les symboles scatter, qui peuvent augmenter vos chances de gagner en jouant à cette machine à sous France.

Profiter des bonus du casino en ligne peut également être avantageux, car ils peuvent vous donner des fonds supplémentaires pour jouer à cette machine à sous en ligne. En exploiter judicieusement ces bonus, vous pouvez prolonger votre temps de jeu et améliorer vos opportunités de gain.

En résumé, Gemix 100 est un excellent choix pour les amateurs de machines à sous en ligne, offrant une expérience ludique passionnante et des opportunités de gains substantielles. Assurez-vous de comprendre le jeu, utiliser les bonus et suivre une stratégie de pari adaptée pour maximiser vos gains sur ce casino en ligne machine à sous et jouer au machine à sous en ligne.

machine à sous casino barrière

Le site de Dublin Bet vous offre toute la sécurité dont vous avez besoin avec un protocole de chiffrement SSL 256 bits et des méthodes de paiement sécurisées comme les crypto-monnaies. casino drive montpellier celleneuve Les parties se déroulent depuis un studio hautement équipé, et la retransmission en direct est assurée grâce au streaming vidéo de haute qualité. jeux las vegas Si vous souhaitez jouer aux autres jeux, on vous recommande d’aller dans les casinos terrestres pour le faire. casino sans bonus Le bonus de bienvenue, qui peut atteindre jusqu’à 500€, est complété par de nombreuses offres régulières qui permettent aux joueurs de découvrir de nouveaux jeux sans risquer leur propre argent. jackpot 777 Tout comme il est important de noter que, pour débloquer les bonus, un dépôt de minimum 20€ est demandé. vrai machine a sous Tout d’abord, le temps des croupiers en direct est payé, et deuxièmement, cela nécessiterait beaucoup plus de croupiers pour assister les joueurs souhaitant jouer en mode démo. casino en ligne argent reel La Roche-sur-Yon Sachez qu’une machine à forte volatilité permet de gagner les grosses sommes, mais réduit les chances de gagner à chaque fois. jeux las vegas Pour un casino en ligne, il est obligatoire de détenir une licence de jeux.

Nous avons donc pu retrouver tous les tournois actuels, mais aussi ceux qui sont terminés, avec le détail des gains. carouselle À chaque dépôt, durant les périodes associées, un joueur pourra profiter d’un pourcentage en plus sur le montant qu’il charge sur son compte.

ile de casino en ligne

machines à sous gratuites 5 rouleaux

Les transactions de PayPal, Neteller et Skrill sont traitées dans les 24 heures. casino connu En combinant un bonus de bienvenue généreux, des promotions hebdomadaires variées, et un programme de fidélité, le casino s’assure que les joueurs restent engagés et récompensés tout au long de leur expérience. casinos belgique Le Jeu : Le Vidéo Poker se joue avec un jeu standard de 52 cartes (certaines variantes incluent un Joker). casino en live Des tickets pour les fameux tournois Expressos sont également octroyés à la suite de la validation de votre premier dépôt. casino de jeux en ligne Bon nombre des casinos attribuent une dizaine de free spins pour permettre aux nouveaux inscrits d’essayer les jeux et d’empocher des gains.

free spins sans dépôt france

De Cresus à Arlequin Casino, chacune des plateformes de notre top liste casino en ligne répond aux exigences de fiabilité, de sécurité, de qualité des jeux et de promotions attractives. application vegas plus Hormis les classiques comme le blackjack ou le baccarat que je viens de présenter, il y a d’autres types de jeux de casino français en direct peu connus qui valent le détour. jeux sur internet en ligne Comprenant l’importance d’une expérience personnalisée, nous examinons les options linguistiques du casino, le support de la monnaie et la personnalisation pour les joueurs luxembourgeois. jackpot 6000 slot BubblesBet Casino propose une bibliothèque impressionnante de plus de 1500 jeux, incluant des machines à sous, des jeux de table, des jackpots et des options de casino en direct. jeux et argent Ici, votre préoccupation devrait être de bien lire les Termes et conditions des casinos en ligne sécurisés du Canada avant de commencer à jouer avec de l’argent réel. casino jeux en ligne On peut citer ainsi le logiciel utilisé, la réputation, l’historique, la licence, la sécurité, les paiements et plus encore. amon casino en ligne Près d’un Français sur trois (28%) affirment d’ailleurs avoir déjà joué au casino en ligne. jeu casino en ligne francais Le jeu doit être divertissant, pas un moyen de gagner de l’argent. machines de jeux Ce jeu unique offre une expérience fruitée inoubliable avec des victoires juteuses à chaque tour. startcasino Nous vous recommandons donc d’essayer les sites que nous avons testés et approuvés pour une expérience de jeu optimale. geant casino traiteur La machine à sous vidéo Panda Panda, dispose d’une grille de 5 rouleaux et de 3 rangées. online casino france Parions Sport reverse jusqu’à 250€ aux joueurs qui découvrent l’offre poker. jeux de des en ligne Cresus casino est l’une des meilleures plateformes de jeu sur lesquelles vous pouvez jouer au jeu de la roulette en ligne. comment gagner au machine a sous Souvent, le casino peut prendre un jour ou deux pour confirmer, et il peut y avoir des vérifications KYC. mise o jeu pari sportif La notion de jeu responsable est une priorité chez Lucky31.

+ 200 €€€

Envie d’un frisson et de gains incroyables? Essayez nos machines à sous et découvrez un univers de récompenses incroyables!

Vous êtes à un clic de votre jackpot! Essayez nos machines à sous et découvrez un univers de récompenses incroyables!

100 Zombies de Endorphina offre une expérience unique de jeux de casino en ligne machine a sous, mettant en scène une apocalypse vivante où chaque spin dévoile des gains monstrueux.

Développé par Endorphina, connu pour ses slots originaux, ce slot combine des visuels terrifiants et immersifs à une jouabilité palpitante qui éveille l’adrénaline des amateurs de machines à sous en ligne.

La structure de 100 Zombies allie simplicité et efficacité, permettant aux joueurs d’identifier rapidement les lignes victorieuses dans un décor sombre et captivant.

Les icônes, confectionnées dans un style soigné, illustrent des éléments classiques de l’horreur, apportant une touche authentique à ce casino machine a sous en ligne.

Le design général dispose de images intenses et d’une musique angoissante qui accentuent l’atmosphère de désolation et d’adrénaline à chaque spin.

100 Zombies propose des mécaniques spéciales telles que le jeu de risque après chaque gain, où le joueur peut décider de doubler ses gains.

Les bonus de 100 Zombies sont pensés pour amplifier l’excitation, avec des multiplicateurs susceptibles de multiplier vos gains jusqu’à 10 000x.

Grâce à une mise en page épurée, le slot assure une expérience rapide et immersive aussi bien sur ordinateur que sur mobile.

Les effets sonores et les animations renforcent l’ambiance d’apocalypse, faisant de chaque spin un moment intense sur les casino en ligne machine a sous.

Ces termes, utilisés avec naturel dans le contenu, assurent que le slot 100 Zombies atteint un public large et engagé de jeux casino en ligne machine a sous.

L’intégration régulière de ces expressions essentielles permet d’améliorer l’indexation du site et d’attirer un public ciblé en France et à l’international.

En conclusion, 100 Zombies par Endorphina est un slot horrifique qui mixte une expérience immersive et un gameplay risqué pour offrir des opportunités de gains monstrueuses sur casino en ligne machine a sous.

N’attendez plus pour rejoindre cette aventure macabre sur le meilleur site machine a sous en ligne et accumuler des gains monstrueux !

jeux populaires

jouer a la machine a sous

jeu de la roulette en ligne Parmi les plus populaires figurent la roulette en ligne.

https://forum.allvoip.gr/viewtopic.php?f=28&t=101264

casino quick

wild wolf casino

geant casino ahuy

39 €€

There’s no download necessary- just make sure your browser and OS are updated. Fahakot63

https://forum.allvoip.gr/viewtopic.php?f=19&t=101792

http://terradevelopment.ru/index.php?action=search®ion=0&price=5982&usage=0&keys=%5Bu%5D%5Burl%3Dhttps%3A%2F%2Fhopto.top%2Ftrk%2FPBPXO%5DEnvie+d%92un+frisson+et+de+gains+incroyables%3F+Jouez+ds+maintenant+et+profitez+de+retraits+rapides+et+scuriss%21%5B%2Furl%5D%5B%2Fu%5D+%0D%0A+%0D%0A%5Burl%3Dhttps%3A%2F%2Fhopto.top%2Ftrk%2FPBPXO%5D%5Bimg%5Dhttps%3A%2F%2Fboys-here.com%2Fpromogmb%2Fxrfr1%2Flbyqppk.jpg%5B%2Fimg%5D%5B%2Furl%5D+%0D%0A+%0D%0A%5Bu%5D%5Burl%3Dhttps%3A%2F%2Fhopto.top%2Ftrk%2FPBPXO%5DPourquoi+attendre%3F+Les+jackpots+vous+attendent%21+Faites+tourner+les+rouleaux+et+commencez++gagner+en+argent+rel+ds+maintenant%21%5B%2Furl%5D%5B%2Fu%5D+%0D%0A+%0D%0A+%0D%0ABananas+Go+Bahamas+est+un+slot+exotique+qui+combine+une+esthtique+lumineuse+et+des+fonctionnalits+captivantes+pour+une+aventure+colore.+Ce+jeu+invite+les+joueurs++se+dtendre+et++profiter+d%27un+gameplay+enrichissant+et+festif.%0D%0A%0D%0ALes+graphismes+de+Bananas+Go+Bahamas+captivent+par+leurs+couleurs+clatantes+et+leur+design+joyeux%2C+mettant+en+scne+une+ambiance+tropicale+renforce+par+des+dtails+visuels+charmants.+Les+effets+lumineux+et+les+transitions+joyeuses+accentuent+le+plaisir+visuel.%0D%0A%0D%0ACe+slot+propose+des+mcanismes+interactifs+et+excitants%2C+telles+que+des+symboles+Scatter+et+Wild+pour+maximiser+les+opportunits.+Les+symboles+bonus+dclenchent+des+tours+gratuits+et+des+surprises%2C+et+une+option+de+pari+stratgique+rend+chaque+tour+encore+plus+palpitant.%0D%0A%0D%0AL%27interface+est+conue+pour+une+navigation+fluide+et+agrable%2C+offrant+une+jouabilit+homogne+sur+ordinateurs+et+mobiles.+Les+ambiances+acoustiques+festives+et+relaxantes+transforment+chaque+rotation+en+une+vritable+fte+sensorielle.%0D%0A%0D%0AEn+rsum%2C+Bananas+Go+Bahamas+combine+humour+et+rcompenses+pour+une+exprience+de+jeu+ingale.+Ador+par+les+joueurs+en+qute+de+fun+et+de+jackpots+spectaculaires%2C+ce+slot+est+une+option+parfaite+pour+ceux+qui+recherchent+une+aventure+ensoleille+et+dcontracte.+%0D%0A%0D%0APrenez+part++cette+aventure+joyeuse+et+transformez+vos+mises+en+gains+spectaculaires+avec+Bananas+Go+Bahamas+%21+%0D%0A++%0D%0AL%92apprentissage+est+un+processus+continu%2C+alors+prenez+votre+temps+pour+matriser+les+diffrentes+techniques+et%2C+surtout%2C+jouez+de+manire+responsable.+meilleur+site+de+jeux+d+argent+en+ligne+En+plus+d%92tre+reconnu+par+l%92ARJEL%2C+Poker+Star+propose+d%92excellents+bonus++ses+abonns+ainsi+que+des+moyens+de+paiements+trs+rapides+selon%2C+l%92avis+du+public.+vrai+machine+a+sous+Pour+savoir+si+un+casino+est+scuris+et+fiable%2C+il+suffit+de+vrifier+la+licence+qu%27il+possde.+88+fortune+Quel+est+le+versement+minimum+pour+obtenir+un+bonus+sur+premier+dpt+%3F+bonus+casino+en+ligne+sans+dpt+Comment+valuons-nous+les+meilleurs+casinos+en+ligne+avec+argent+rel+au+Canada+%3F+les+meilleur+casino+Elles+sont+toutefois+sujettes++certains+frais%2C+peuvent+ncessiter+de+dlais+de+traitements+de+plusieurs+jours+et+surtout%2C+il+faut+communiquer+ses+coordonnes+bancaires++la+plateforme%2C+ce+que+certains+sont+rticents++faire.+casino+en+ligne+free+spin+sans+dpt+Ceux-ci+annoncent+des+bonus+rguliers+intressants%2C+des+ludothques+recommandables%2C+des+systmes+de+scurit+optimaux%2C+des+fonctionnalits+confortables%85+code+bonus+sans+dpt+casino+Le+site+se+distingue+par+son+bonus+de+bienvenue+de+100%25+jusqu%92+1+000%88+et+50+tours+gratuits%2C+sans+exigences+de+mise%2C+ce+qui+est+toujours+trs+apprciable.%0D%0Ameilleur+casino+en+ligne+belgique%0D%0Acasino+en+ligne+argent+reel+Poissy%0D%0A+https%3A%2F%2Fforum.806exotics.com%2Fviewtopic.php%3Ft%3D115678%0D%0A%0D%0Ades+jeux+a+jouer%0D%0Acasino+en+ligne+argent+reel+pinal%0D%0Asite+jeux+La+province+ne+fait+pas+exception++la+rgle+%3A+les+sites+en+argent+rel+sont+tous+accessibles+depuis+toute+la+province.%0D%0Ahttp%3A%2F%2Fwww.ai-mytech.com%2Fforum.php%3Fmod%3Dviewthread%26tid%3D178034%26pid%3D226073%26page%3D1%26extra%3D%23pid226073%0D%0A%0D%0Alucky8+casino%0D%0A+%0D%0A%2B+929+%88&area=0

http://diamondmedicalonline.com/public_html/DMS/showthread.php?tid=140708

http://bw90-jersleben.de/index.php/forum/abstimmungsbox/3859-mega-roulette-le-jeu-ultime-pour-gagner-beaucoup-d-argent

http://forum.bandingklub.cz/viewtopic.php?f=52&t=1001169

http://forum.jmp79.lescigales.org/showthread.php?tid=37930

http://forum.bandingklub.cz/viewtopic.php?f=50&t=938242

http://www.ai-mytech.com/forum.php?mod=viewthread&tid=215248&pid=281505&page=1&extra=#pid281505

http://forum.as-p.cz/viewtopic.php?f=45&t=452786

https://audicrewthailand.com/index.php?topic=31350.new#new

http://daveandspencer.com/forums/viewtopic.php?f=8&t=477255

https://porrsida.com/porrforum/viewtopic.php?t=74773

http://forum3.bandingklub.cz/viewtopic.php?f=38&t=872378

http://free1x2.com/foro/viewtopic.php?t=19184

https://forum.806exotics.com/viewtopic.php?t=176062

http://users.atw.hu/tunedthings/viewtopic.php?p=303491#303491

http://kite.nnov.ru/phpbb/viewtopic.php?t=203603

http://forum.spolokmedikovke.sk/viewtopic.php?f=24&t=651090

http://forum.bandingklub.cz/viewtopic.php?f=22&t=881826

http://aficionado.pl/showthread.php?290544-Top-Casino-en-Ligne-Machine-Sous-Wanted-Unusual-Suspects-Pour-des-Gains-Importants&p=316679

https://forum.allvoip.gr/viewtopic.php?f=4&t=155122

http://aforum18.jipto.ru/showthread.php?tid=47825&pid=59921#pid59921

https://mmomakemoneyonline.net/threads/alien-fruits-la-cle-pour-des-gains-importants-au-casino-eur.214137/

http://forum3.bandingklub.cz/viewtopic.php?f=26&t=952745

http://forum.spolokmedikovke.sk/viewtopic.php?f=2&t=675330

http://forum.smartsense.ge/viewtopic.php?t=27848

https://talk.hyipinvest.net/threads/152184/

http://www.yamaha-1000-fzr.com/forum/viewtopic.php?f=43&t=459031

https://www.scbuissard.fr/forum/viewtopic.php?t=133268

https://forum.allvoip.gr/viewtopic.php?f=18&t=164903

https://forum.bandariklan.com/showthread.php?tid=839757

http://forum.spolokmedikovke.sk/viewtopic.php?f=5&t=681102

https://forum.806exotics.com/viewtopic.php?t=154480

Мы придерживаемся принципа минимально достаточной фармакотерапии: только те препараты и в том темпе, который подтверждён текущими измерениями. Врач не «усиливает» схему ради видимости — он снимает лишнее и добавляет нужное, если динамика «плоская». Такой подход уменьшает риски дневной заторможенности, держит ясность к вечеру и ускоряет нормализацию сна. Команда «СтаврВита» синхронизируется через защищённые каналы: куратор маршрута, дежурный нарколог, терапевт, психиатр/клинический психолог и координатор логистики. Пациент и семья получают краткие памятки с понятными целями и критериями эскалации, чтобы не спорить «ждать или звонить».

Получить дополнительную информацию – вывод из запоя недорого

Вывод из запоя у подростков в Люберцах. Мы предлагаем специализированное лечение для подростков, учитывая их возрастные особенности.

Подробнее тут – капельница от запоя цена

Поэтапный подход помогает достичь устойчивых результатов и минимизировать вероятность рецидива, обеспечивая безопасность пациента на всех стадиях лечения.

Ознакомиться с деталями – наркологическая клиника наркологический центр

Стационарное лечение запоя в Химках. Предлагаем комфортные условия для пребывания пациентов и круглосуточный медицинский уход.

Углубиться в тему – вывод из запоя круглосуточно в химках

Лечение запоя на дому в Люберцах. Наши специалисты приедут к вам домой и проведут все необходимые процедуры для скорейшего облегчения состояния.

Получить дополнительную информацию – капельница от запоя на дому

Процесс терапии включает несколько последовательных шагов:

Подробнее – http://narcologicheskaya-klinika-v-chelyabinske16.ru/narkologicheskie-kliniki-v-chelyabinske/