For those of you who have not heard of Loyal3.com, it is a website / broker that allows you to purchase and accumulate high quality dividend stocks with no commissions. That’s right – no commissions with no catch.

I wrote a short introduction and review of Loyal3 last month titled “MCD Accumulation in Loyal3 Account.” In that post I mentioned that I was taking Loyal3 for a test drive by investing $25 per month in McDonalds (MCD). This Loyal3 account is part of my Dividend Empire portfolio, where my goal is to accumulate high quality dividend growth stocks to build a dividend paying empire for my descendants. So far I am very pleased with my Loyal3 experience and therefore I’ve decided to double my monthly contributions.

Loyal3 doesn’t allow you to invest in any stock. Instead they have a basket of popular stocks, mostly consumer goods and services, allowing investors to “Own What They Love.” This sounds like a turnoff but rest assured, Loyal3 offers plenty of great dividend growth stocks. One of the great options available at Loyal3 is Hershey (HSY). Instead of just doubling down on MCD I decided to add HSY to my portfolio for two reasons:

- Diversity – I currently have no exposure to the confectioners industry

- Growth – HSY is simply a great company with excellent earnings and dividend growth (see analysis below)

Before diving into the analysis let me briefly explain my goals for this position (and my MCD position).

Loyal3 Hershey Accumulation Goals

First off, here are the transaction details for my first HSY purchase:

- Portfolio: Dividend Empire

- Sector: Consumer Goods

- Industry: Confectioners

- Shares purchased: 0.2648

- Cost per share: $94.41

- Commissions: $0

- Cost basis: $25

- Yield: 2.29%

- Expected annual income: $0.52

I realize that this transaction seems rather insignificant, and i agree to some extent. $25 and 0.2648 shares is not much, representing just 0.16% of my portfolio. First off I do plan on increasing my monthly contributions to both HSY and MCD to $50 – $100 per month. Second, my Loyal3 account is all about accumulation and dollar cost averaging.

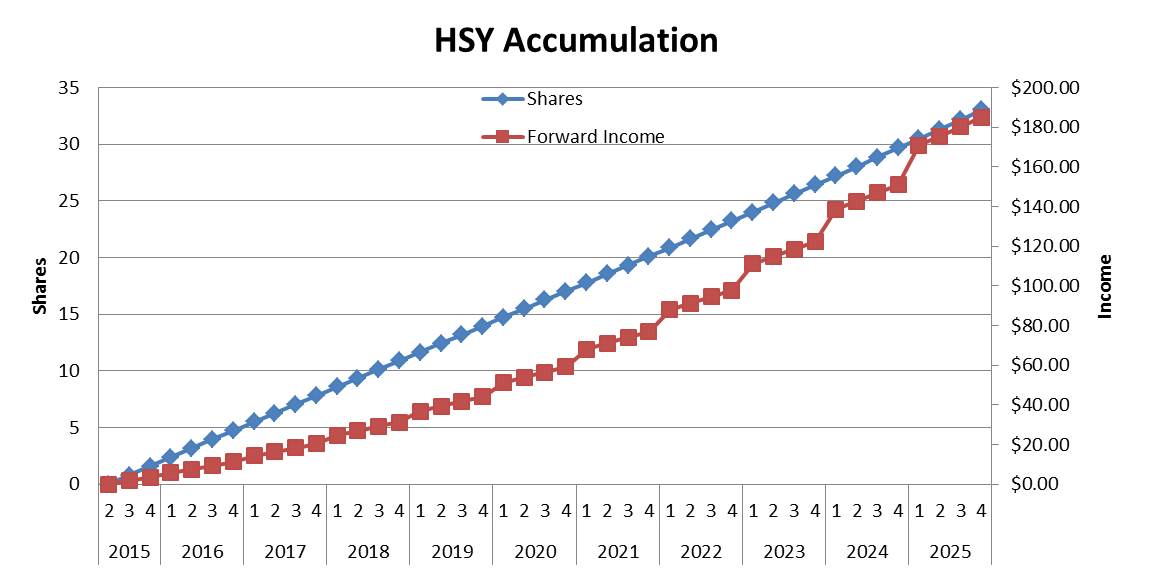

It’s hard to believe that $25 per month can actually grow to a significant amount, and that’s why I ran a simulation to see what my position might look like in 10 years. Here are the assumptions:

- Starting stock price: $94.41

- Starting annual dividend: $2.16 (2.29% yield)

- Annual dividend growth: 10% (5-year actual = 11.7%)

- Stock price growth: 4%

- Monthly contributions: $25

Here is what the share growth and forward income growth looks like:

Given these condition, after 10 years I can expect to have the following position:

- HSY shares: 33.015

- Stock price: $143.39

- Capital invested: $3225

- Position value: $4734

- Forward income: $184.97

- Yield on cost: 5.74%

Not bad, right? And if (when) I eventually increase my contributions to $50 or $100 per month I will establish a very sizable position. Since my current position size in the Dividend Empire portfolio is between $1500-$3000 it will probably only take 1-2 years to establish a “full” HSY position. You can view the spreadsheet I used to make these projections HERE.

OK so now that I’ve hopefully convinced you that my $25 investment is reasonable, let me explain why I think Hershey is a good buy.

Hershey’s Overview

One thing I love is investing in companies that offer products that I personally buy or use. Hershey’s is definitely one of those companies. Although I try to maintain a “paleo lifestyle” and have a fairly clean diet, I just can’t stay away from Reese’s Peanut Butter Cups and Reese’s Pieces. Some other famous brands Hershey owns (and I have consumed at some point) are Hershey’s chocolates, Mounds, Kit Kat, Heath, York, Bubble Yum and Ice Breakers.

Here is a brief overview provided by Hershey’s website:

The Hershey Company is the leading North American manufacturer of quality chocolate and non-chocolate confectionery and chocolate-related grocery products. The company also is a leader in the gum and mint category.

Hershey’s was started by Milton Hershey back in 1894 and quickly became the first company to offer chocolate to the masses, not just the wealthy. Hershey rapidly expanded from chocolate products to the brands I mentioned above and many others. They have also developed a strong international presence with operations in over 90 countries.

Hershey’s Financial Strength

The past 5 years have been great for HSY. Their revenue has grown an average of 7% and their earnings have grown an average of 14.6%!

10-year revenue per share and earnings per share:

HSY data by GuruFocus.com

HSY data by GuruFocus.com

Hershey’s sales have slowed down a bit this year but recent increases in pricing should result in an 11-14% increase in EPS in 2015. This excellent growth should continue, aided by acquisitions and international growth. Currently only 12% of sales come from international operations leaving plenty of room to grow.

HSY has a 2015 PE ratio of 21.9 in line with the industry average. This looks to be a bit high but it is certainly justifiable given Hershey’s growth rate.

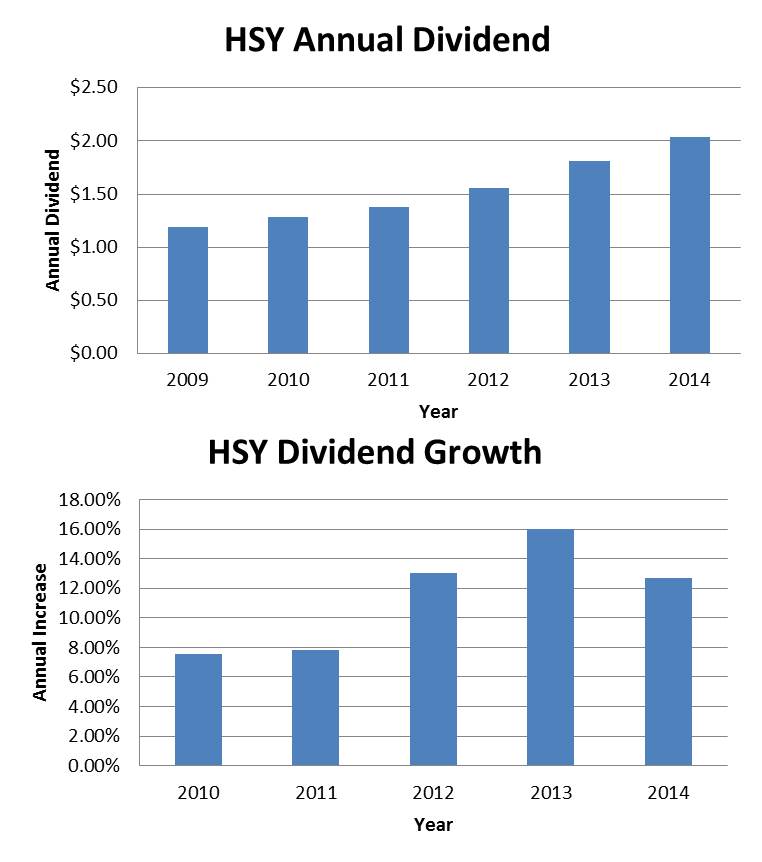

Hershey’s Dividend Strength

This is where HSY really shines. Hershey has increased their dividend every year for the past 5 years, just making the dividend challengers list. This is not a very long time but if you take out just one year, 2009, where the dividend didn’t increase (it was not cut) the streak would go back decades. Plus the annual dividend growth rate over the past 5 years has been a solid 11.4%.

If this growth rate continues a yield of 2.27% today would turn into almost 4% in 5 years. This doesn’t really apply to me since I will be accumulating my HSY position slowly over the next couple of years, but once my full position is established it is comforting to know that my yield on cost should increase over time. They have also been able to keep their payout ratio around 50% over the past few years so the dividend should be sustainable.

Hershey’s Fair Value Estimate

Given the average dividend growth of 11.4% over the past 5 years, the Gordon Growth Model gives a very unreasonable estimate of over $300/share (using a required return of 12%). This model is only good for dividend growth stocks with a long and consistent track record of dividend growth.

Therefore I will rely on analysts estimates to determine the fair value of HSY. Of the 10 analysts covering Hershey, 2 rate the stock a strong buy while 8 recommend holding with a consensus price target of $101/share. Based on this consensus the stock seems fairly valued.

Portfolio Impact

This small purchase of Hershey adds $0.52 annual income and is too insignificant to change my portfolio yield on cost, which currently stands at 3.43%. It does give me a tiny bit of exposure to the confectioners industry and this exposure will grow over time with my monthly contributions to HSY in my Loyal3 account.

My $25 monthly contribution to MCD also went through today as part of my MCD accumulation. This transaction added 0.2562 shares of MCD bringing my total up to 0.5135 shares. This MCD purchase adds $0.88 annual income and did not change my portfolio yield.

What are your thoughts on HSY? Anyone else using Loyal3 to slowly accumulate dividend growth stocks?

Hello Dividend Empire,

I am going to certainly check the site out. It seems like a great way to collect great dividend paying stocks with no transaction fees! Moreover, Hershey is a solid pick and will be around many more years to come. Thanks for sharing.

-LOMD

liveoffmydividends recently posted…New Purchase of Coca-Cola Stock

I agree and hopefully their dividend will continue growing at the current pace.

Definitely check out Loyal3. I think I’m going to start accumulating WMT and GPS as well at some point. Thanks for stopping by!

Hi Dividend Empire

Hershey is definitely a good purchase there as consumers purchasing power is increasing in the new decades and they have consistently came up with new products and innovations to sell to customers. Financials wise it looks good too so seems like a nice good buy, unless it gets overvalued.

B recently posted…Dividend Income Updates – “The Power of Dividends”

Thanks for the comment B. Hopefully the price doesn’t go up too much before I finish accumulating.

Viagra Rezept Deutschland cialis without a doctor’s prescription

inch

comfort

dash

[url=http://bag33ondu.com]bag33ondu.com[/url]

bag33ondu.com

http://bag33ondu.com

kip

retract

jungle

candida kilo kaybıhızlı kilo kaybı baş dönmesi kusma kilo kayb? nefes darl?g? iştah kilo kaybı panik atakvitaminslik kilo kaybı

köpeklerin ani ve hızlı kilo kaybıtip 2 diyabet kilo kaybı ramazanda kilo kayb? onlemek ishal kilo kaybıgraves kilo kaybı

zaman zaman mide bulantısı çarpıntı iştahsızlık kilo kaybı enfeksiyonbir anda kilo kaybı ramazanda kilo kayb? böbrek taşı kilo kaybı yaparmıfulsac kilo kaybı

ani kilo kaybД± nedirkanserde kilo kaybД± ne kadar olur ishal olma ve kilo kayb? yasama ani kilo kaybД±nД±n sebeplericrp yГјksekliДџi iЕџtahsД±zlД±k kilo kaybД±

mide rahatsızlıkları kilo kaybıgebelikte.ishal.kilo kaybı yaparmi kilo kayb? nas?l olur ek gıdaya geçişte kilo kaybıkanser belirtileri kilo kaybı

I’ve been absent for a while, but now I remember why I used to love this web site. Thanks , I?ll try and check back more often. How frequently you update your site?

There are some fascinating closing dates on this article however I don?t know if I see all of them center to heart. There may be some validity but I will take maintain opinion until I look into it further. Good article , thanks and we want extra! Added to FeedBurner as well

Thank you, I’ve recently been searching for info about this topic for ages and yours is the best I’ve discovered so far. But, what about the conclusion? Are you sure about the source?

Great blog here! Also your website loads up very fast! What host are you using? Can I get your affiliate link to your host? I wish my website loaded up as quickly as yours lol

I’m in awe of the author’s talent to make intricate concepts understandable to readers of all backgrounds. This article is a testament to his expertise and commitment to providing helpful insights. Thank you, author, for creating such an compelling and illuminating piece. It has been an absolute pleasure to read!

I can’t express how much I admire the effort the author has put into creating this exceptional piece of content. The clarity of the writing, the depth of analysis, and the wealth of information provided are simply remarkable. His enthusiasm for the subject is apparent, and it has undoubtedly resonated with me. Thank you, author, for providing your knowledge and enhancing our lives with this extraordinary article!

I think this is one of the most vital information for me. And i’m glad reading your article. But wanna remark on few general things, The web site style is wonderful, the articles is really great : D. Good job, cheers

of course like your web site but you need to check the spelling on quite a few of your posts. A number of them are rife with spelling issues and I in finding it very bothersome to tell the reality then again I will definitely come back again.

whoah this weblog is wonderful i love reading your articles. Stay up the great work! You realize, lots of persons are hunting round for this information, you can aid them greatly.

very nice publish, i definitely love this website, keep on it

I do love the way you have framed this problem and it does indeed provide us some fodder for consideration. However, from everything that I have seen, I just trust as other feedback stack on that people remain on issue and not start on a tirade of some other news of the day. Yet, thank you for this fantastic point and whilst I do not necessarily go along with it in totality, I value the perspective.

okmark your blog and check again here regularly. I’m quite certain I will learn plenty of new stuff right here! Good luck for the next!

Hiya! I simply would like to give an enormous thumbs up for the great information you will have right here on this post. I will be coming again to your weblog for more soon.

Your writing style effortlessly draws me in, and I find it nearly impossible to stop reading until I’ve reached the end of your articles. Your ability to make complex subjects engaging is indeed a rare gift. Thank you for sharing your expertise!

Excellent website you have here but I was wondering if you knew of any message boards that cover the same topics discussed in this article? I’d really love to be a part of online community where I can get comments from other knowledgeable people that share the same interest. If you have any suggestions, please let me know. Thanks!

Thanks for your post. One other thing is when you are promoting your property all on your own, one of the issues you need to be aware about upfront is how to deal with property inspection records. As a FSBO owner, the key concerning successfully transferring your property and also saving money in real estate agent revenue is knowledge. The more you realize, the smoother your sales effort will be. One area exactly where this is particularly essential is information about home inspections.

Thanks for the suggestions about credit repair on this site. Some tips i would advice people is always to give up a mentality they can buy at this moment and shell out later. Like a society we tend to do that for many things. This includes getaways, furniture, as well as items we really want to have. However, you’ll want to separate a person’s wants from the needs. When you’re working to improve your credit rating score you really have to make some sacrifices. For example you’ll be able to shop online to economize or you can go to second hand outlets instead of costly department stores pertaining to clothing.

Your blog is a true gem in the vast expanse of the online world. Your consistent delivery of high-quality content is truly commendable. Thank you for consistently going above and beyond in providing valuable insights. Keep up the fantastic work!

Aw, this was a really nice post. In idea I would like to put in writing like this moreover ? taking time and actual effort to make a very good article? however what can I say? I procrastinate alot and by no means appear to get something done.

I am continually impressed by your ability to delve into subjects with grace and clarity. Your articles are both informative and enjoyable to read, a rare combination. Your blog is a valuable resource, and I am sincerely grateful for it.

Your unique approach to addressing challenging subjects is like a breath of fresh air. Your articles stand out with their clarity and grace, making them a pure joy to read. Your blog has now become my go-to source for insightful content.

Today, I went to the beach with my kids. I found a sea shell and gave it to my 4 year old daughter and said “You can hear the ocean if you put this to your ear.” She put the shell to her ear and screamed. There was a hermit crab inside and it pinched her ear. She never wants to go back! LoL I know this is totally off topic but I had to tell someone!

I couldn’t agree more with the insightful points you’ve articulated in this article. Your profound knowledge on the subject is evident, and your unique perspective adds an invaluable dimension to the discourse. This is a must-read for anyone interested in this topic.

Wow, awesome blog layout! How long have you been blogging for? you make blogging look easy. The overall look of your web site is excellent, let alone the content!

Good article. It’s very unfortunate that over the last decade, the travel industry has had to take on terrorism, SARS, tsunamis, flu virus, swine flu, plus the first ever true global economic collapse. Through it the industry has proven to be powerful, resilient and also dynamic, locating new approaches to deal with adversity. There are usually fresh problems and possibilities to which the industry must just as before adapt and respond.

I’m truly impressed by the way you effortlessly distill intricate concepts into easily digestible information. Your writing style not only imparts knowledge but also engages the reader, making the learning experience both enjoyable and memorable. Your passion for sharing your expertise is unmistakable, and for that, I am deeply grateful.

I have fun with, cause I discovered just what I used to be having a look for. You have ended my 4 day long hunt! God Bless you man. Have a nice day. Bye

I must applaud your talent for simplifying complex topics. Your ability to convey intricate ideas in such a relatable manner is admirable. You’ve made learning enjoyable and accessible for many, and I deeply appreciate that.

I’d like to express my heartfelt appreciation for this insightful article. Your unique perspective and well-researched content bring a fresh depth to the subject matter. It’s evident that you’ve invested considerable thought into this, and your ability to convey complex ideas in such a clear and understandable way is truly commendable. Thank you for sharing your knowledge so generously and making the learning process enjoyable.

This article is a true game-changer! Your practical tips and well-thought-out suggestions hold incredible value. I’m eagerly anticipating implementing them. Thank you not only for sharing your expertise but also for making it accessible and easy to apply.

Your passion and dedication to your craft radiate through every article. Your positive energy is infectious, and it’s evident that you genuinely care about your readers’ experience. Your blog brightens my day!

Your positivity and enthusiasm are truly infectious! This article brightened my day and left me feeling inspired. Thank you for sharing your uplifting message and spreading positivity to your readers.

Your dedication to sharing knowledge is unmistakable, and your writing style is captivating. Your articles are a pleasure to read, and I consistently come away feeling enriched. Thank you for being a dependable source of inspiration and information.

This article is a real game-changer! Your practical tips and well-thought-out suggestions are incredibly valuable. I can’t wait to put them into action. Thank you for not only sharing your expertise but also making it accessible and easy to implement.

Your positivity and enthusiasm are undeniably contagious! This article brightened my day and left me feeling inspired. Thank you for sharing your uplifting message and spreading positivity among your readers.

This article resonated with me on a personal level. Your ability to emotionally connect with your audience is truly commendable. Your words are not only informative but also heartwarming. Thank you for sharing your insights.

Your storytelling prowess is nothing short of extraordinary. Reading this article felt like embarking on an adventure of its own. The vivid descriptions and engaging narrative transported me, and I eagerly await to see where your next story takes us. Thank you for sharing your experiences in such a captivating manner.

Hi there, just became alert to your blog through Google, and found that it’s really informative. I am gonna watch out for brussels. I will be grateful if you continue this in future. A lot of people will be benefited from your writing. Cheers!

Your writing style effortlessly draws me in, and I find it difficult to stop reading until I reach the end of your articles. Your ability to make complex subjects engaging is a true gift. Thank you for sharing your expertise!

Your storytelling prowess is nothing short of extraordinary. Reading this article felt like embarking on an adventure of its own. The vivid descriptions and engaging narrative transported me, and I eagerly await to see where your next story takes us. Thank you for sharing your experiences in such a captivating manner.

http://casulopedagogico.com.br/tracado-das-letras-com-massinha-de-modelar/

Today, while I was at work, my sister stole my iphone and tested to see if it can survive a 30 foot drop, just so she can be a youtube sensation. My iPad is now broken and she has 83 views. I know this is entirely off topic but I had to share it with someone!

I must applaud your talent for simplifying complex topics. Your ability to convey intricate ideas in such a relatable manner is admirable. You’ve made learning enjoyable and accessible for many, and I deeply appreciate that.

In a world where trustworthy information is more crucial than ever, your dedication to research and the provision of reliable content is truly commendable. Your commitment to accuracy and transparency shines through in every post. Thank you for being a beacon of reliability in the online realm.

I am continually impressed by your ability to delve into subjects with grace and clarity. Your articles are both informative and enjoyable to read, a rare combination. Your blog is a valuable resource, and I am sincerely grateful for it.

Your unique approach to tackling challenging subjects is a breath of fresh air. Your articles stand out with their clarity and grace, making them a joy to read. Your blog is now my go-to for insightful content.

I simply wanted to convey how much I’ve gleaned from this article. Your meticulous research and clear explanations make the information accessible to all readers. It’s abundantly clear that you’re committed to providing valuable content.

One thing I’d like to discuss is that fat burning plan fast may be possible by the proper diet and exercise. Ones size not simply affects appearance, but also the complete quality of life. Self-esteem, depressive disorder, health risks, in addition to physical skills are affected in an increase in weight. It is possible to make everything right and at the same time having a gain. Should this happen, a condition may be the offender. While a lot of food rather than enough exercising are usually at fault, common medical conditions and popular prescriptions might greatly amplify size. Kudos for your post right here.

Your storytelling prowess is nothing short of extraordinary. Reading this article felt like embarking on an adventure of its own. The vivid descriptions and engaging narrative transported me, and I eagerly await to see where your next story takes us. Thank you for sharing your experiences in such a captivating manner.

Your enthusiasm for the subject matter radiates through every word of this article; it’s contagious! Your commitment to delivering valuable insights is greatly valued, and I eagerly anticipate more of your captivating content. Keep up the exceptional work!

Your dedication to sharing knowledge is unmistakable, and your writing style is captivating. Your articles are a pleasure to read, and I consistently come away feeling enriched. Thank you for being a dependable source of inspiration and information.

We absolutely love your blog and find almost all of your post’s to be exactly I’m looking for. Do you offer guest writers to write content in your case? I wouldn’t mind publishing a post or elaborating on a lot of the subjects you write with regards to here. Again, awesome blog!

Along with almost everything that appears to be developing throughout this specific subject matter, your viewpoints happen to be fairly refreshing. Nonetheless, I am sorry, but I can not subscribe to your entire idea, all be it exhilarating none the less. It seems to everybody that your comments are generally not totally rationalized and in reality you are yourself not even fully convinced of your argument. In any case I did take pleasure in looking at it.

I want to express my appreciation for this insightful article. Your unique perspective and well-researched content bring a new depth to the subject matter. It’s clear you’ve put a lot of thought into this, and your ability to convey complex ideas in such a clear and understandable way is truly commendable. Thank you for sharing your knowledge and making learning enjoyable.

I wanted to take a moment to express my gratitude for the wealth of invaluable information you consistently provide in your articles. Your blog has become my go-to resource, and I consistently emerge with new knowledge and fresh perspectives. I’m eagerly looking forward to continuing my learning journey through your future posts.

Your enthusiasm for the subject matter shines through every word of this article; it’s contagious! Your commitment to delivering valuable insights is greatly valued, and I eagerly anticipate more of your captivating content. Keep up the exceptional work!

I’ve discovered a treasure trove of knowledge in your blog. Your unwavering dedication to offering trustworthy information is truly commendable. Each visit leaves me more enlightened, and I deeply appreciate your consistent reliability.

I can’t help but be impressed by the way you break down complex concepts into easy-to-digest information. Your writing style is not only informative but also engaging, which makes the learning experience enjoyable and memorable. It’s evident that you have a passion for sharing your knowledge, and I’m grateful for that.

I must applaud your talent for simplifying complex topics. Your ability to convey intricate ideas in such a relatable manner is admirable. You’ve made learning enjoyable and accessible for many, and I deeply appreciate that.

Your unique approach to addressing challenging subjects is like a breath of fresh air. Your articles stand out with their clarity and grace, making them a pure joy to read. Your blog has now become my go-to source for insightful content.

I wanted to take a moment to express my gratitude for the wealth of invaluable information you consistently provide in your articles. Your blog has become my go-to resource, and I consistently emerge with new knowledge and fresh perspectives. I’m eagerly looking forward to continuing my learning journey through your future posts.

I couldn’t agree more with the insightful points you’ve made in this article. Your depth of knowledge on the subject is evident, and your unique perspective adds an invaluable layer to the discussion. This is a must-read for anyone interested in this topic.

Your dedication to sharing knowledge is unmistakable, and your writing style is captivating. Your articles are a pleasure to read, and I consistently come away feeling enriched. Thank you for being a dependable source of inspiration and information.

I’m impressed by the quality of this content! The author has obviously put a tremendous amount of effort into investigating and structuring the information. It’s inspiring to come across an article that not only gives valuable information but also keeps the readers captivated from start to finish. Hats off to her for making such a brilliant work!

I simply wanted to convey how much I’ve gleaned from this article. Your meticulous research and clear explanations make the information accessible to all readers. It’s abundantly clear that you’re committed to providing valuable content.

Your enthusiasm for the subject matter shines through in every word of this article. It’s infectious! Your dedication to delivering valuable insights is greatly appreciated, and I’m looking forward to more of your captivating content. Keep up the excellent work!

Your unique approach to addressing challenging subjects is like a breath of fresh air. Your articles stand out with their clarity and grace, making them a pure joy to read. Your blog has now become my go-to source for insightful content.

Your writing style effortlessly draws me in, and I find it nearly impossible to stop reading until I’ve reached the end of your articles. Your ability to make complex subjects engaging is indeed a rare gift. Thank you for sharing your expertise!

Your blog has rapidly become my trusted source of inspiration and knowledge. I genuinely appreciate the effort you invest in crafting each article. Your dedication to delivering high-quality content is apparent, and I eagerly await every new post.

I want to express my appreciation for this insightful article. Your unique perspective and well-researched content bring a new depth to the subject matter. It’s clear you’ve put a lot of thought into this, and your ability to convey complex ideas in such a clear and understandable way is truly commendable. Thank you for sharing your knowledge and making learning enjoyable.

I’m continually impressed by your ability to dive deep into subjects with grace and clarity. Your articles are both informative and enjoyable to read, a rare combination. Your blog is a valuable resource, and I’m grateful for it.

I’m genuinely impressed by how effortlessly you distill intricate concepts into easily digestible information. Your writing style not only imparts knowledge but also engages the reader, making the learning experience both enjoyable and memorable. Your passion for sharing your expertise is unmistakable, and for that, I am deeply appreciative.

I wanted to take a moment to express my gratitude for the wealth of valuable information you provide in your articles. Your blog has become a go-to resource for me, and I always come away with new knowledge and fresh perspectives. I’m excited to continue learning from your future posts.

Your blog is a true gem in the vast expanse of the online world. Your consistent delivery of high-quality content is truly commendable. Thank you for consistently going above and beyond in providing valuable insights. Keep up the fantastic work!

Your writing style effortlessly draws me in, and I find it nearly impossible to stop reading until I’ve reached the end of your articles. Your ability to make complex subjects engaging is indeed a rare gift. Thank you for sharing your expertise!

This article resonated with me on a personal level. Your ability to emotionally connect with your audience is truly commendable. Your words are not only informative but also heartwarming. Thank you for sharing your insights.

Your blog has quickly become my trusted source of inspiration and knowledge. I genuinely appreciate the effort you put into crafting each article. Your dedication to delivering high-quality content is evident, and I look forward to every new post.

Your writing style effortlessly draws me in, and I find it nearly impossible to stop reading until I’ve reached the end of your articles. Your ability to make complex subjects engaging is indeed a rare gift. Thank you for sharing your expertise!

This is really interesting, You’re a very skilled blogger. I have joined your rss feed and look forward to seeking more of your great post. Also, I’ve shared your website in my social networks!

In a world where trustworthy information is more crucial than ever, your dedication to research and the provision of reliable content is truly commendable. Your commitment to accuracy and transparency shines through in every post. Thank you for being a beacon of reliability in the online realm.

I’d like to express my heartfelt appreciation for this enlightening article. Your distinct perspective and meticulously researched content bring a fresh depth to the subject matter. It’s evident that you’ve invested a great deal of thought into this, and your ability to articulate complex ideas in such a clear and comprehensible manner is truly commendable. Thank you for generously sharing your knowledge and making the process of learning so enjoyable.

Your blog is a true gem in the vast online world. Your consistent delivery of high-quality content is admirable. Thank you for always going above and beyond in providing valuable insights. Keep up the fantastic work!

Your enthusiasm for the subject matter shines through every word of this article; it’s infectious! Your commitment to delivering valuable insights is greatly valued, and I eagerly anticipate more of your captivating content. Keep up the exceptional work!

Oh my goodness! an incredible article dude. Thank you Nevertheless I’m experiencing problem with ur rss . Don?t know why Unable to subscribe to it. Is there anybody getting an identical rss problem? Anyone who is aware of kindly respond. Thnkx

Your blog is a true gem in the vast expanse of the online world. Your consistent delivery of high-quality content is truly commendable. Thank you for consistently going above and beyond in providing valuable insights. Keep up the fantastic work!

I’d like to express my heartfelt appreciation for this enlightening article. Your distinct perspective and meticulously researched content bring a fresh depth to the subject matter. It’s evident that you’ve invested a great deal of thought into this, and your ability to articulate complex ideas in such a clear and comprehensible manner is truly commendable. Thank you for generously sharing your knowledge and making the process of learning so enjoyable.

In a world where trustworthy information is more important than ever, your commitment to research and providing reliable content is truly commendable. Your dedication to accuracy and transparency is evident in every post. Thank you for being a beacon of reliability in the online world.

Almanya’nın en iyi medyumu haluk hoca sayesinde sizlerde güven içerisinde çalışmalar yaptırabilirsiniz, 40 yıllık uzmanlık ve tecrübesi ile sizlere en iyi medyumluk hizmeti sunuyoruz.

I must applaud your talent for simplifying complex topics. Your ability to convey intricate ideas in such a relatable manner is admirable. You’ve made learning enjoyable and accessible for many, and I deeply appreciate that.

Almanya’nın en çok tercih edilen medyumu haluk yıldız hoca olarak bilinmektedir, 40 yıllık tecrübesi ile sizlere en iyi bağlama işlemini yapan ilk medyum hocadır.

Your positivity and enthusiasm are undeniably contagious! This article brightened my day and left me feeling inspired. Thank you for sharing your uplifting message and spreading positivity among your readers.

Your passion and dedication to your craft radiate through every article. Your positive energy is infectious, and it’s evident that you genuinely care about your readers’ experience. Your blog brightens my day!

http://www.thebudgetart.com is trusted worldwide canvas wall art prints & handmade canvas paintings online store. Thebudgetart.com offers budget price & high quality artwork, up-to 50 OFF, FREE Shipping USA, AUS, NZ & Worldwide Delivery.

Merhaba Ben Haluk Hoca, Aslen Irak Asıllı Arap Hüseyin Efendinin Torunuyum. Yaklaşık İse 40 Yıldır Havas Ve Hüddam İlmi Üzerinde Sizlere 100 Sonuç Veren Garantili Çalışmalar Hazırlamaktayım, 1964 Yılında Irak’ın Basra Şehrinde Doğdum, Dedem Arap Hüseyin Efendiden El Aldım Ve Sizlere 1990 lı Yıllardan Bu Yana Medyum Hocalık Konularında Hizmet Veriyorum, 100 Sonuç Vermiş Olduğum Çalışmalar İse, Giden Eşleri Sevgilileri Geri Getirme, Aşk Bağlama, Aşık Etme, Kısmet Açma, Büyü Bozma Konularında Garantili Sonuçlar Veriyorum, Başta Almanya Fransa Hollanda Olmak Üzere Dünyanın Neresinde Olursanız Olun Hiç Çekinmeden Benimle İletişim Kurabilirsiniz.

It’s the best time to make some plans for the future and it is time to be happy. I have read this post and if I could I desire to suggest you few interesting things or advice. Perhaps you could write next articles referring to this article. I desire to read more things about it!

Almanya’nın en iyi güvenilir medyumunun tüm sosyal medya hesaplarını sizlere paylaşıyoruz, güvenin ve kalitelin tek adresi olan medyum haluk hoca 40 yıllık uzmanlığı ile sizlerle.

Hello, i think that i saw you visited my web site so i got here to ?return the choose?.I am trying to in finding issues to improve my web site!I assume its adequate to make use of some of your ideas!!

After study a few of the blog posts in your website now, and I truly like your approach of blogging. I bookmarked it to my bookmark web site listing and can be checking back soon. Pls check out my website online as well and let me know what you think.

of course like your website however you need to check the spelling on quite a few of your posts. Several of them are rife with spelling issues and I find it very bothersome to inform the reality nevertheless I will certainly come back again.

http://www.thebudgetart.com is trusted worldwide canvas wall art prints & handmade canvas paintings online store. Thebudgetart.com offers budget price & high quality artwork, up-to 50 OFF, FREE Shipping USA, AUS, NZ & Worldwide Delivery.

Thanks for the strategies presented. One thing I additionally believe is credit cards presenting a 0 rate of interest often bait consumers together with zero rate, instant approval and easy on the web balance transfers, nevertheless beware of the top factor that will void that 0 easy neighborhood annual percentage rate and also throw you out into the very poor house rapid.

Dünyaca ünlü medyum haluk hocayı sizlere tanıtıyoruz anlatıyoruz, Avrupanın ilk ve tek medyum hocası 40 yıllık uzmanlık ve tecrübesi ile sizlerle.

je**@tw****.com

Belçika’nın en iyi medyumu medyum haluk hoca ile sizlerde en iyi çalışmalara yakınsınız, hemen arayın farkı görün.

Another issue is that video games are usually serious in nature with the principal focus on knowing things rather than enjoyment. Although, it comes with an entertainment factor to keep children engaged, every game is usually designed to develop a specific group of skills or program, such as math concepts or science. Thanks for your post.

in**@pu*****.com

gr**@bi************.com

Medyum haluk hoca avrupanın en güvenilir medyum hocasıdır, sizlerinde bilgiği gibi en iyi medyumu bulmak zordur, biz sizlere geldik.

I have figured out some points through your site post. One other point I would like to say is that there are many games that you can buy which are designed especially for preschool age kids. They include things like pattern recognition, colors, dogs, and patterns. These typically focus on familiarization instead of memorization. This keeps little children engaged without experiencing like they are studying. Thanks

Ünlülerin tercih ettiği medyum hocamıza dilediğiniz zaman ulaşabilirsiniz, medyum haluk hocamız sizlerin daimi yanında olacaktır.

https://waylon3fa40.blogunteer.com/22873130/facts-about-chinese-medicine-for-diabetes-revealed https://bookmark-media.com/story15929387/korean-massage-chair-options https://catmang801dcb2.dekaronwiki.com/user https://walterg838rni8.plpwiki.com/user https://shane417x5.targetblogs.com/23073200/korea-massage-chair-secrets https://oliverx694npq9.activoblog.com/profile

Birincisi güvenilir medyum hocaları bulmak olacaktır, ikinci seçenek ise en iyi medyumları bulmak olacaktır, siz hangisini seçerdiniz.

https://dominick3ic59.kylieblog.com/23144803/medicine-china-can-be-fun-for-anyone https://getsocialpr.com/story16158158/the-ultimate-guide-to-korean-massage-chair https://davyc579xxu0.blgwiki.com/user https://francesz962llo7.wiki-cms.com/user https://ericka62db.fare-blog.com/22975283/5-easy-facts-about-korean-massage-cream-described https://fredl160wrk8.spintheblog.com/profile

https://mariom0azz.bloggazza.com/22725876/new-step-by-step-map-for-chinese-medical-massage https://reubeng791ded3.theblogfairy.com/profile https://emilioc0738.blog5star.com/23013344/little-known-facts-about-massage-korean-spas https://gorillasocialwork.com/story16066688/an-unbiased-view-of-massage-chinese-garden https://albertj010lwf3.wikissl.com/user https://georgesd827mha4.ja-blog.com/profile

https://emmae051egh9.blog-mall.com/profile https://fernandor2dbb.bloginwi.com/56333218/examine-this-report-on-chinese-massage-oil https://dantetxxz334567.blogprodesign.com/44501591/a-simple-key-for-baby-massage-to-help-poop-unveiled https://beau4wa73.tblogz.com/top-massage-chinese-london-secrets-37177187 https://natural-bookmark.com/story15880687/korean-massage-chair-ala-moana-things-to-know-before-you-buy https://jaschaq197cmv7.gigswiki.com/user

I’m blown away by the quality of this content! The author has undoubtedly put a tremendous amount of effort into investigating and organizing the information. It’s inspiring to come across an article that not only provides valuable information but also keeps the readers captivated from start to finish. Hats off to him for making such a masterpiece!

https://explorethehorizon.co.uk/

Sizler için en iyi medyum hoca tanıtımı yapıyoruz, Avrupanın en ünlü medyum hocası haluk yıldız hoca sizlerin güvenini hızla kazanmaya devam ediyor.

https://cardera578wvt0.wikiitemization.com/user

I feel this is among the most significant information for me. And i am happy reading your article. However wanna remark on some basic things, The site taste is ideal, the articles is in reality nice : D. Just right process, cheers

Spot on with this write-up, I truly suppose this web site needs rather more consideration. I?ll in all probability be again to read way more, thanks for that info.

https://emilianoe9630.bloggin-ads.com/45776408/not-known-factual-statements-about-chinese-medicine-basics

https://waylonr4814.creacionblog.com/22891397/getting-my-chinese-medicine-brain-fog-to-work

Dünyaca ünlü medyum haluk hoca, 40 yıllık uzmanlık ve tecrübesi ile sizlere en iyi hizmetleri vermeye devam ediyor, Aşk büyüsü bağlama büyüsü giden sevigiliyi geri getirme.

Youre so cool! I dont suppose Ive learn something like this before. So nice to find any person with some unique thoughts on this subject. realy thanks for beginning this up. this website is one thing that’s wanted on the web, somebody with a little originality. useful job for bringing one thing new to the web!

https://jasperv86po.rimmablog.com/22823075/the-best-side-of-korean-massage-spa-nyc

https://arthurt4949.popup-blog.com/22884778/detailed-notes-on-chinese-medicine-chart

https://cash1k778.alltdesign.com/how-chinese-medicine-journal-can-save-you-time-stress-and-money-42796624

https://johnathani3085.win-blog.com/2127817/5-simple-statements-about-chinese-medicine-cupping-explained

https://troyiopp80123.full-design.com/a-simple-key-for-thailand-massage-unveiled-65301171

Ünlülerin tercihi medyum haluk hoca sizlerle, en iyi medyum sitemizi ziyaret ediniz.

https://titus0l6yw.qodsblog.com/22944196/helping-the-others-realize-the-advantages-of-chinese-massage-miami

https://mysocialname.com/story1068148/thailand-massage-types-things-to-know-before-you-buy

https://deborahn047lew3.theisblog.com/profile

https://charlie69fd3.blogerus.com/45237185/getting-my-korean-bubble-massage-to-work

https://troyi2852.dgbloggers.com/23092590/5-essential-elements-for-chinese-medicine-bloating

Ünlülerin tercihi medyum haluk hoca sizlerle, en iyi medyum sitemizi ziyaret ediniz.

https://ricardo02eb2.bligblogging.com/23076114/5-simple-statements-about-korea-massage-chair-explained

https://louis8ee33.look4blog.com/61881280/fascination-about-chinese-medicine-chi

Today, while I was at work, my sister stole my iphone and tested to see if it can survive a 30 foot drop, just so she can be a youtube sensation. My iPad is now broken and she has 83 views. I know this is entirely off topic but I had to share it with someone!

Ünlülerin tercihi medyum haluk hoca sizlerle, en iyi medyum sitemizi ziyaret ediniz.

Have you ever thought about creating an e-book or guest authoring on other blogs? I have a blog based on the same subjects you discuss and would love to have you share some stories/information. I know my readers would appreciate your work. If you’re even remotely interested, feel free to shoot me an e-mail.

What i do not realize is actually how you are not really much more well-liked than you may be right now. You’re so intelligent. You realize therefore significantly relating to this subject, made me personally consider it from so many varied angles. Its like women and men aren’t fascinated unless it?s one thing to do with Lady gaga! Your own stuffs outstanding. Always maintain it up!

Ünlülerin tercihi medyum haluk hoca sizlerle, en iyi medyum sitemizi ziyaret ediniz.

https://deang55kg.acidblog.net/53626581/not-known-factual-statements-about-korean-massage-spa-irvine

https://augustbeghz.blogproducer.com/28565700/top-massage-korean-spas-secrets

https://holden3ym81.like-blogs.com/22830393/facts-about-chinese-medicine-for-inflammation-revealed

Ünlülerin tercihi medyum haluk hoca sizlerle, en iyi medyum sitemizi ziyaret ediniz.

güvenilir bir medyum hoca bulmak o kadarda zor değil, medyum haluk hoca sizlerin en iyi medyumu.

https://rafaelr1223.mybuzzblog.com/2053055/5-simple-techniques-for-chinese-medicine-classes

https://francisco1kkj6.blogdon.net/what-does-healthy-massage-kansas-city-mean-38847076

https://eduardox0n8r.blogsmine.com/22929472/top-latest-five-us-massage-service-urban-news

https://damien36w0y.daneblogger.com/22836901/new-step-by-step-map-for-chinese-medicine-body-chart

https://stephen7ab3f.creacionblog.com/22781405/5-simple-techniques-for-korean-massage-for-healthy

https://richarda344fbu9.eqnextwiki.com/user

Woah! I’m really enjoying the template/theme of this blog. It’s simple, yet effective. A lot of times it’s very hard to get that “perfect balance” between superb usability and appearance. I must say that you’ve done a fantastic job with this. Additionally, the blog loads very fast for me on Opera. Superb Blog!

I?ll right away grab your rss feed as I can not find your email subscription link or e-newsletter service. Do you have any? Please let me know in order that I could subscribe. Thanks.

Thanks on your marvelous posting! I truly enjoyed reading it, you may be a great author.I will be sure to bookmark your blog and may come back later in life. I want to encourage you to ultimately continue your great work, have a nice day!

Ünlülerin tercih ettiği bir medyum hoca bulmak o kadarda zor değil, medyum haluk hoca sizlerin en iyi medyumu.

excellent post, very informative. I wonder why the other specialists of this sector don’t notice this. You should continue your writing. I’m confident, you’ve a huge readers’ base already!

https://elliott02f3g.blog2freedom.com/22911320/not-known-facts-about-chinese-medicine-clinic

https://charlesw245jey1.smblogsites.com/profile

Good web site! I truly love how it is easy on my eyes and the data are well written. I’m wondering how I might be notified whenever a new post has been made. I’ve subscribed to your RSS which must do the trick! Have a nice day!

https://andresqkew.angelinsblog.com/22818038/thailand-massage-centre-can-be-fun-for-anyone

https://telebookmarks.com/story5724165/what-does-chinese-medicine-clinic-mean

https://paxtonqhrai.theideasblog.com/23072058/massage-korat-secrets

https://johnathan07306.anchor-blog.com/3308962/chinese-medicine-clinic-for-dummies

https://ellioti8360.spintheblog.com/23115183/chinese-medicine-books-no-further-a-mystery

https://richardh532ffe9.slypage.com/profile

https://deboraho578tsl0.national-wiki.com/user

https://cruz6ab33.vblogetin.com/28023927/the-best-side-of-chinese-medicine-certificate

https://zane7yayw.wikigop.com/258101/massage_koreanisch_no_further_a_mystery

https://mylesj14tc.gynoblog.com/22839841/the-best-side-of-massage-chinese-quarter-birmingham

je**@tw****.com

Thanks for the unique tips discussed on this site. I have realized that many insurers offer customers generous discounts if they favor to insure more and more cars with them. A significant volume of households possess several vehicles these days, especially those with more aged teenage kids still residing at home, and also the savings upon policies can certainly soon begin. So it pays to look for a great deal.

I have taken notice that in digital cameras, exceptional detectors help to {focus|concentrate|maintain focus|target|a**** automatically. The particular sensors connected with some digital cameras change in contrast, while others make use of a beam involving infra-red (IR) light, specifically in low lighting. Higher specification cameras at times use a blend of both devices and will often have Face Priority AF where the photographic camera can ‘See’ a face while keeping your focus only upon that. Thank you for sharing your thinking on this weblog.

https://wavesocialmedia.com/story1217822/the-best-side-of-massage-koreatown-los-angeles

https://jacquesx344ifc2.ktwiki.com/user

https://pauly456nkh4.wikikarts.com/user

With havin so much content do you ever run into any problems of plagorism or copyright infringement? My website has a lot of exclusive content I’ve either written myself or outsourced but it appears a lot of it is popping it up all over the internet without my permission. Do you know any solutions to help protect against content from being stolen? I’d certainly appreciate it.

Bağlama büyüsü konularında en iyi büyü yapan medyum haluk hoca sizlerin her zaman kısa sürede yanınızda tek yapmanız gereken aramak.

Ankara yeminli tercüme bürosu hizmeti, sizleriçin çeviri hizmetini ayağınıza getiriyoruz hemen iletişim.

https://elliotp0481.blogdanica.com/22939519/getting-my-chinese-medicine-brain-fog-to-work

https://august60l7p.blogsmine.com/23069322/top-latest-five-chinese-medicine-body-map-urban-news

https://august57t9s.tokka-blog.com/23080507/top-chinese-medicine-breakfast-secrets

It is indeed my belief that mesothelioma can be the most lethal cancer. It has unusual features. The more I really look at it the more I am persuaded it does not respond like a real solid tissues cancer. When mesothelioma is a rogue viral infection, then there is the possibility of developing a vaccine plus offering vaccination for asbestos uncovered people who are really at high risk of developing upcoming asbestos linked malignancies. Thanks for revealing your ideas for this important ailment.

Thank you, I have recently been looking for information about this topic for a while and yours is the best I have came upon till now. But, what concerning the bottom line? Are you certain about the supply?

https://michaelr775crf1.get-blogging.com/profile

https://derricke677pjd2.wikirecognition.com/user

https://elliotkkhd22322.review-blogger.com/44761096/not-known-facts-about-us-massage-service

Hi there just wanted to give you a quick heads up. The text in your article seem to be running off the screen in Safari. I’m not sure if this is a format issue or something to do with browser compatibility but I figured I’d post to let you know. The design and style look great though! Hope you get the issue solved soon. Cheers

https://peterx345jfa2.mycoolwiki.com/user

https://sociallytraffic.com/story637424/the-smart-trick-of-chinese-medicine-journal-that-no-one-is-discussing

https://bookmarkalexa.com/story1187167/the-basic-principles-of-chinese-medicine-books

Astroloji nedir rüya ilmi nedir hüddam ilmi nedir vefk ilmi ile yapılacak işlemler nelerdir.

I like what you guys are up also. Such intelligent work and reporting! Carry on the excellent works guys I have incorporated you guys to my blogroll. I think it’ll improve the value of my website 🙂

I?m not sure where you’re getting your info, but great topic. I needs to spend some time learning much more or understanding more. Thanks for wonderful info I was looking for this information for my mission.

bookdecorfactory.com is a Global Trusted Online Fake Books Decor Store. We sell high quality budget price fake books decoration, Faux Books Decor. We offer FREE shipping across US, UK, AUS, NZ, Russia, Europe, Asia and deliver 100+ countries. Our delivery takes around 12 to 20 Days. We started our online business journey in Sydney, Australia and have been selling all sorts of home decor and art styles since 2008.

https://johnathan3o890.howeweb.com/23101073/the-best-side-of-chinese-medicine-cracked-tongue

https://erickw3567.anchor-blog.com/3287106/examine-this-report-on-chinese-medicine-breakfast

https://sethyzv00.is-blog.com/28634195/considerations-to-know-about-massage-therapy-business-plan-example

magnificent submit, very informative. I wonder why the other specialists of this sector don’t notice this. You should continue your writing. I’m confident, you’ve a great readers’ base already!

https://andres6yzxv.onesmablog.com/not-known-factual-statements-about-massage-coreen-62618832

https://elliotw2184.blogsmine.com/23120615/not-known-factual-statements-about-chinese-medicine-basics

https://setbookmarks.com/story15860484/5-simple-statements-about-business-trip-message-explained

I have observed that car insurance firms know the cars which are vulnerable to accidents and other risks. They also know what kind of cars are given to higher risk and the higher risk they’ve the higher your premium price. Understanding the very simple basics of car insurance just might help you choose the right form of insurance policy that could take care of your needs in case you get involved in an accident. Thank you sharing a ideas on your own blog.

Wow, awesome blog structure! How lengthy have you been blogging for? you make running a blog look easy. The total look of your site is magnificent, let alone the content!

Do you mind if I quote a couple of your articles as long as I provide credit and sources back to your webpage? My blog is in the exact same area of interest as yours and my users would certainly benefit from some of the information you provide here. Please let me know if this ok with you. Thanks!

Thanks for the distinct tips contributed on this site. I have observed that many insurance carriers offer buyers generous reductions if they favor to insure more and more cars with them. A significant variety of households possess several cars these days, specifically those with more aged teenage kids still dwelling at home, and also the savings in policies may soon increase. So it pays to look for a great deal.

Right now THIS is how to compose an engaging, insightful piece!

You’ve set a new bar for excellence.

Also visit my webpage; bc online payday loans

bc online payday loans recently posted…bc online payday loans

This is really interesting, You are a very skilled blogger. I’ve joined your feed and look forward to seeking more of your excellent post. Also, I’ve shared your web site in my social networks!

http://wecan.skybbs.biz/home.php?mod=space&uid=539314

http://womans-days.ru/user/browtip96/

Valuable info. Lucky me I found your web site by accident, and I’m shocked why this accident did not happened earlier! I bookmarked it.

https://www.gisbbs.cn/user_uid_1757046.html

https://www.pepysdiary.com/search/?q=해운대고구려й빽링크엔드(구글상위노출)

What?s Happening i am new to this, I stumbled upon this I have found It positively useful and it has aided me out loads. I’m hoping to give a contribution & help different customers like its aided me. Good job.

whoah this blog is fantastic i love reading your articles. Keep up the great work! You know, lots of people are hunting around for this information, you can help them greatly.

gr**@bi************.com

je**@tw****.com

ni**************@pu*****.com

in**@pu*****.com

There are definitely a lot of particulars like that to take into consideration. That could be a great level to bring up. I supply the thoughts above as general inspiration but clearly there are questions just like the one you bring up where a very powerful thing will probably be working in trustworthy good faith. I don?t know if greatest practices have emerged around issues like that, but I am sure that your job is clearly identified as a good game. Both girls and boys feel the influence of only a moment?s pleasure, for the remainder of their lives.

naturally like your web-site but you need to check the spelling on several of your posts. Several of them are rife with spelling issues and I find it very bothersome to tell the truth nevertheless I will definitely come back again.

I like the valuable information you provide on your articles.

I’ll bookmark your weblog and test again right here regularly.

I am quite certain I will learn a lot of new stuff right here!

Good luck for the next!

udin777 recently posted…udin777

I just could not depart your web site before suggesting that I actually enjoyed the standard info a person provide for your visitors? Is going to be back often in order to check up on new posts

Appreciate you for sharing most of these wonderful threads. In addition, the optimal travel and medical insurance plan can often eradicate those issues that come with journeying abroad. Your medical crisis can rapidly become too expensive and that’s bound to quickly put a financial weight on the family finances. Setting up in place the excellent travel insurance bundle prior to leaving is worth the time and effort. Thanks

Good post. I am experiencing a few of these issues

as well..

best used cars recently posted…best used cars

I have realized that in digital cameras, unique receptors help to {focus|concentrate|maintain focus|target|a**** automatically. Those sensors involving some video cameras change in contrast, while others make use of a beam associated with infra-red (IR) light, specifically in low lighting. Higher spec cameras from time to time use a blend of both programs and might have Face Priority AF where the digital camera can ‘See’ the face and focus only on that. Many thanks for sharing your ideas on this weblog.

http://www.spotnewstrend.com is a trusted latest USA News and global news provider. Spotnewstrend.com website provides latest insights to new trends and worldwide events. So keep visiting our website for USA News, World News, Financial News, Business News, Entertainment News, Celebrity News, Sport News, NBA News, NFL News, Health News, Nature News, Technology News, Travel News.

I have seen lots of useful issues on your website about personal computers. However, I’ve the judgment that laptop computers are still not nearly powerful enough to be a wise decision if you generally do tasks that require a great deal of power, just like video enhancing. But for website surfing, microsoft word processing, and many other prevalent computer functions they are perfectly, provided you can’t mind the small screen size. Thanks for sharing your thinking.

Great write-up, I?m normal visitor of one?s blog, maintain up the excellent operate, and It is going to be a regular visitor for a lengthy time.

in**@pu*****.com

Your house is valueble for me. Thanks!?

https://image.google.ms/url?q=https://ED8084EC9794EB939C.com/shop/search.php?sfl=tEC98A4EB9DBDEC8BA4ECA3BCEC868CE6BC8FGood-bet888comEC9C88EC9C88EBB2B3+EC9B90EBB2B3EC9B90+EAB5BFEBB2B3

in**@pu*****.com

ni**************@pu*****.com

je**@tw****.com

gr**@bi************.com

I have noticed that car insurance providers know the autos which are vulnerable to accidents and other risks. Additionally they know what type of cars are inclined to higher risk and also the higher risk they have got the higher the actual premium charge. Understanding the uncomplicated basics regarding car insurance will let you choose the right sort of insurance policy that will take care of your wants in case you get involved in an accident. Thank you sharing a ideas with your blog.

Nice post. I was checking continuously this blog and I’m impressed!

Very helpful info specifically the last part 🙂 I care

for such info much. I was looking for this certain info for a very long time.

Thank you and good luck.

spg138 recently posted…spg138

https://cse.google.as/url?q=https://paroisses-valdesaone.com/blog/JED8590ED8590EBB2B3armE38090Good-bet888.COME3809127E3808EGood-bet888.COME3808Funi88.html

Just desire to say your article is as surprising. The clearness to your publish is just excellent and that i can assume you are a professional in this subject. Fine along with your permission allow me to seize your RSS feed to stay up to date with forthcoming post. Thank you 1,000,000 and please carry on the gratifying work.

I have realized that in old digital cameras, unique receptors help to {focus|concentrate|maintain focus|target|a**** automatically. These sensors involving some digital cameras change in in the area of contrast, while others work with a beam associated with infra-red (IR) light, particularly in low lumination. Higher standards cameras from time to time use a mix of both models and may have Face Priority AF where the video camera can ‘See’ a new face as you concentrate only in that. Many thanks for sharing your opinions on this site.

Your unique approach to addressing challenging subjects is like a breath of fresh air. Your articles stand out with their clarity and grace, making them a pure joy to read. Your blog has now become my go-to source for insightful content.

I’ve discovered a treasure trove of knowledge in your blog. Your unwavering dedication to offering trustworthy information is truly commendable. Each visit leaves me more enlightened, and I deeply appreciate your consistent reliability.

I couldn’t agree more with the insightful points you’ve articulated in this article. Your profound knowledge on the subject is evident, and your unique perspective adds an invaluable dimension to the discourse. This is a must-read for anyone interested in this topic.

http://www.bestartdeals.com.au is Australia’s Trusted Online Canvas Prints Art Gallery. We offer 100 percent high quality budget wall art prints online since 2009. Get 30-70 percent OFF store wide sale, Prints starts $20, FREE Delivery Australia, NZ, USA. We do Worldwide Shipping across 50+ Countries.

Woah! I’m really loving the template/theme of

this site. It’s simple, yet effective. A lot of times it’s difficult to get that “perfect balance” between superb

usability and visual appearance. I must say you have done a great job with this.

Also, the blog loads very fast for me on Firefox. Excellent Blog!

anichin donghua recently posted…anichin donghua

I have mastered some considerations through your blog post. One other point I would like to talk about is that there are plenty of games that you can buy which are designed in particular for toddler age little ones. They include pattern identification, colors, wildlife, and models. These typically focus on familiarization instead of memorization. This makes children engaged without feeling like they are studying. Thanks

Your blog is a true gem in the vast expanse of the online world. Your consistent delivery of high-quality content is truly commendable. Thank you for consistently going above and beyond in providing valuable insights. Keep up the fantastic work!

Your blog is a true gem in the vast expanse of the online world. Your consistent delivery of high-quality content is truly commendable. Thank you for consistently going above and beyond in providing valuable insights. Keep up the fantastic work!

Your writing style effortlessly draws me in, and I find it difficult to stop reading until I reach the end of your articles. Your ability to make complex subjects engaging is a true gift. Thank you for sharing your expertise!

you might have an ideal weblog here! would you like to make some invite posts on my blog?

I am continually impressed by your ability to delve into subjects with grace and clarity. Your articles are both informative and enjoyable to read, a rare combination. Your blog is a valuable resource, and I am sincerely grateful for it.

In a world where trustworthy information is more crucial than ever, your dedication to research and the provision of reliable content is truly commendable. Your commitment to accuracy and transparency shines through in every post. Thank you for being a beacon of reliability in the online realm.

Your blog has rapidly become my trusted source of inspiration and knowledge. I genuinely appreciate the effort you invest in crafting each article. Your dedication to delivering high-quality content is apparent, and I eagerly await every new post.

I’m genuinely impressed by how effortlessly you distill intricate concepts into easily digestible information. Your writing style not only imparts knowledge but also engages the reader, making the learning experience both enjoyable and memorable. Your passion for sharing your expertise shines through, and for that, I’m deeply grateful.

I like the valuable info you provide in your articles. I will bookmark your blog and check again here frequently. I am quite certain I?ll learn lots of new stuff right here! Good luck for the next!

Your unique approach to addressing challenging subjects is like a breath of fresh air. Your articles stand out with their clarity and grace, making them a pure joy to read. Your blog has now become my go-to source for insightful content.

Your positivity and enthusiasm are truly infectious! This article brightened my day and left me feeling inspired. Thank you for sharing your uplifting message and spreading positivity to your readers.

I am continually impressed by your ability to delve into subjects with grace and clarity. Your articles are both informative and enjoyable to read, a rare combination. Your blog is a valuable resource, and I am sincerely grateful for it.

I’m truly enjoying the design and layout of your site. It’s a very easy on the eyes which makes it much more pleasant for me to come here and visit more often. Did you hire out a designer to create your theme? Outstanding work!

I simply wanted to convey how much I’ve gleaned from this article. Your meticulous research and clear explanations make the information accessible to all readers. It’s abundantly clear that you’re committed to providing valuable content.

I am continually impressed by your ability to delve into subjects with grace and clarity. Your articles are both informative and enjoyable to read, a rare combination. Your blog is a valuable resource, and I am sincerely grateful for it.

I simply wanted to convey how much I’ve gleaned from this article. Your meticulous research and clear explanations make the information accessible to all readers. It’s abundantly clear that you’re committed to providing valuable content.

I wanted to take a moment to express my gratitude for the wealth of invaluable information you consistently provide in your articles. Your blog has become my go-to resource, and I consistently emerge with new knowledge and fresh perspectives. I’m eagerly looking forward to continuing my learning journey through your future posts.

Aw, this was a very nice post. In thought I would like to put in writing like this additionally – taking time and actual effort to make a very good article… however what can I say… I procrastinate alot and not at all appear to get something done.

Your dedication to sharing knowledge is unmistakable, and your writing style is captivating. Your articles are a pleasure to read, and I consistently come away feeling enriched. Thank you for being a dependable source of inspiration and information.

Your writing style effortlessly draws me in, and I find it nearly impossible to stop reading until I’ve reached the end of your articles. Your ability to make complex subjects engaging is indeed a rare gift. Thank you for sharing your expertise!

Your unique approach to addressing challenging subjects is like a breath of fresh air. Your articles stand out with their clarity and grace, making them a pure joy to read. Your blog has now become my go-to source for insightful content.

I’m genuinely impressed by how effortlessly you distill intricate concepts into easily digestible information. Your writing style not only imparts knowledge but also engages the reader, making the learning experience both enjoyable and memorable. Your passion for sharing your expertise is unmistakable, and for that, I am deeply appreciative.

This article resonated with me on a personal level. Your ability to emotionally connect with your audience is truly commendable. Your words are not only informative but also heartwarming. Thank you for sharing your insights.

I’m in awe of the author’s talent to make complicated concepts accessible to readers of all backgrounds. This article is a testament to his expertise and dedication to providing valuable insights. Thank you, author, for creating such an captivating and insightful piece. It has been an absolute pleasure to read!

I’ve discovered a treasure trove of knowledge in your blog. Your unwavering dedication to offering trustworthy information is truly commendable. Each visit leaves me more enlightened, and I deeply appreciate your consistent reliability.

I’ve discovered a treasure trove of knowledge in your blog. Your unwavering dedication to offering trustworthy information is truly commendable. Each visit leaves me more enlightened, and I deeply appreciate your consistent reliability.

The loan payment frequency option of accelerating installments weekly or

biweekly as an alternative to monthly takes benefit from compounding effects helping

pay down mortgages faster over amortization periods.

Mortgage portability permits transferring a current private mortgage lenders BC to a new eligible property.

private mortgage lenders BC recently posted…private mortgage lenders BC

Fantastic site. A lot of helpful information here. I?m sending it to a few friends ans additionally sharing in delicious. And of course, thank you in your effort!

This article resonated with me on a personal level. Your ability to connect with your audience emotionally is commendable. Your words are not only informative but also heartwarming. Thank you for sharing your insights.

Your passion and dedication to your craft radiate through every article. Your positive energy is infectious, and it’s evident that you genuinely care about your readers’ experience. Your blog brightens my day!

I’m continually impressed by your ability to dive deep into subjects with grace and clarity. Your articles are both informative and enjoyable to read, a rare combination. Your blog is a valuable resource, and I’m grateful for it.

I must applaud your talent for simplifying complex topics. Your ability to convey intricate ideas in such a relatable manner is admirable. You’ve made learning enjoyable and accessible for many, and I deeply appreciate that.

https://xn--cm2by8iw5h6xm8pc.com/bbs/search.php?srows=0&gr_id=&sfl=wr_subject&stx=각시탈:어디계시죠?

In these days of austerity and relative anxiousness about running into debt, many people balk about the idea of utilizing a credit card to make purchase of merchandise or pay for a holiday, preferring, instead only to rely on the particular tried along with trusted means of making payment – cash. However, if you possess the cash there to make the purchase in full, then, paradoxically, that’s the best time to be able to use the card for several reasons.

I simply wanted to convey how much I’ve gleaned from this article. Your meticulous research and clear explanations make the information accessible to all readers. It’s abundantly clear that you’re committed to providing valuable content.

I’ve discovered a treasure trove of knowledge in your blog. Your unwavering dedication to offering trustworthy information is truly commendable. Each visit leaves me more enlightened, and I deeply appreciate your consistent reliability.

I must commend your talent for simplifying complex topics. Your ability to convey intricate ideas in such a relatable way is admirable. You’ve made learning enjoyable and accessible for many, and I appreciate that.

An impressive share, I just given this onto a colleague who was doing somewhat analysis on this. And he in truth purchased me breakfast as a result of I discovered it for him.. smile. So let me reword that: Thnx for the deal with! However yeah Thnkx for spending the time to discuss this, I feel strongly about it and love reading more on this topic. If attainable, as you change into expertise, would you mind updating your blog with extra details? It’s extremely helpful for me. Big thumb up for this weblog publish!

I’m genuinely impressed by how effortlessly you distill intricate concepts into easily digestible information. Your writing style not only imparts knowledge but also engages the reader, making the learning experience both enjoyable and memorable. Your passion for sharing your expertise shines through, and for that, I’m deeply grateful.

Your passion and dedication to your craft radiate through every article. Your positive energy is infectious, and it’s evident that you genuinely care about your readers’ experience. Your blog brightens my day!

I couldn’t agree more with the insightful points you’ve articulated in this article. Your profound knowledge on the subject is evident, and your unique perspective adds an invaluable dimension to the discourse. This is a must-read for anyone interested in this topic.

I?m not sure where you’re getting your information, but good topic. I needs to spend some time learning more or understanding more. Thanks for fantastic information I was looking for this info for my mission.

Your positivity and enthusiasm are undeniably contagious! This article brightened my day and left me feeling inspired. Thank you for sharing your uplifting message and spreading positivity among your readers.

We stumbled over here different web address and thought I may as well check things out. I like what I see so now i am following you. Look forward to going over your web page yet again.

Your positivity and enthusiasm are undeniably contagious! This article brightened my day and left me feeling inspired. Thank you for sharing your uplifting message and spreading positivity among your readers.

This article is a true game-changer! Your practical tips and well-thought-out suggestions hold incredible value. I’m eagerly anticipating implementing them. Thank you not only for sharing your expertise but also for making it accessible and easy to apply.

Your storytelling prowess is nothing short of extraordinary. Reading this article felt like embarking on an adventure of its own. The vivid descriptions and engaging narrative transported me, and I eagerly await to see where your next story takes us. Thank you for sharing your experiences in such a captivating manner.

Your enthusiasm for the subject matter shines through in every word of this article. It’s infectious! Your dedication to delivering valuable insights is greatly appreciated, and I’m looking forward to more of your captivating content. Keep up the excellent work!

Its like you read my mind! You appear to grasp a lot about this, such as you wrote the guide in it or something. I believe that you can do with some percent to power the message house a bit, but other than that, that is great blog. A great read. I will certainly be back.

Just desire to say your article is as surprising. The clearness to your publish is just great and that i could think you’re a professional on this subject. Fine along with your permission let me to seize your RSS feed to keep up to date with impending post. Thanks one million and please continue the gratifying work.

Your dedication to sharing knowledge is evident, and your writing style is captivating. Your articles are a pleasure to read, and I always come away feeling enriched. Thank you for being a reliable source of inspiration and information.

This article is a true game-changer! Your practical tips and well-thought-out suggestions hold incredible value. I’m eagerly anticipating implementing them. Thank you not only for sharing your expertise but also for making it accessible and easy to apply.

I couldn’t agree more with the insightful points you’ve made in this article. Your depth of knowledge on the subject is evident, and your unique perspective adds an invaluable layer to the discussion. This is a must-read for anyone interested in this topic.

Your storytelling prowess is nothing short of extraordinary. Reading this article felt like embarking on an adventure of its own. The vivid descriptions and engaging narrative transported me, and I eagerly await to see where your next story takes us. Thank you for sharing your experiences in such a captivating manner.

This article resonated with me on a personal level. Your ability to connect with your audience emotionally is commendable. Your words are not only informative but also heartwarming. Thank you for sharing your insights.

I must commend your talent for simplifying complex topics. Your ability to convey intricate ideas in such a relatable way is admirable. You’ve made learning enjoyable and accessible for many, and I appreciate that.

This article is a real game-changer! Your practical tips and well-thought-out suggestions are incredibly valuable. I can’t wait to put them into action. Thank you for not only sharing your expertise but also making it accessible and easy to implement.

I must applaud your talent for simplifying complex topics. Your ability to convey intricate ideas in such a relatable manner is admirable. You’ve made learning enjoyable and accessible for many, and I deeply appreciate that.

Your blog has rapidly become my trusted source of inspiration and knowledge. I genuinely appreciate the effort you invest in crafting each article. Your dedication to delivering high-quality content is apparent, and I eagerly await every new post.

I’m genuinely impressed by how effortlessly you distill intricate concepts into easily digestible information. Your writing style not only imparts knowledge but also engages the reader, making the learning experience both enjoyable and memorable. Your passion for sharing your expertise shines through, and for that, I’m deeply grateful.

Your blog is a true gem in the vast expanse of the online world. Your consistent delivery of high-quality content is truly commendable. Thank you for consistently going above and beyond in providing valuable insights. Keep up the fantastic work!