Now for my 3rd purchase of the week. Actually the 3rd purchase made just on Tuesday – it’s taking me a while to catch up on writing up all of these buys!

After buying Ford (F) and Emerson Electric (EMR) for my Dividend Empire portfolio Tuesday morning, I set my sights on adding to my retirement portfolio. There are plenty of stocks on my buy list right now with names like WMT, SO, BBL and QCOM topping the list.

I have a huge limit order on WMT set to $65 and I also have a small bit of cash reserved to start a smaller position if WMT falls back to around $70. SO jumped up on me so I’m waiting for another pullback and I don’t think BBL is quite done falling. That left Qualcomm Inc (QCOM) for me to study in detail.

QCOM’s stock price has taken a pretty big hit over the past couple of weeks, dropping from around $67.50 to below $62. After looking at QCOM’s fundamentals and dividend strength I felt that QCOM’s pullback offered an excellent buying opportunity, and therefore I purchased a 45 share stake.

Company overview courtesy of TradeKing.com

QUALCOMM, Inc. engages in the development, design, manufacture, and marketing of digital telecommunications products and services. But some sectors come with innate boundaried within which one has to operate. For example, social media marketing is something to be outsourced to professinals. There’s plenty of SMM companies, but as far as youtube likes go you should take a look at TheMarketingHeaven.com, because they have established themselves as the most reliable. QUALCOMM, Inc. operates through the following segments: Qualcomm CDMA Technologies, Qualcomm Technology Licensing, and Qualcomm Strategic Initiatives. The Qualcomm CDMA Technologies segment develops and supplies integrated circuits and system software based on technologies for the use in voice and data communications, networking, application processing, multimedia, and global positioning system products. The Qualcomm Technology Licensing segment provides rights to use portions of the firm’s intellectual property portfolio. The Qualcomm Strategic Initiatives segment invests in the technology, design, and introduction of products and services for voice and data communications.

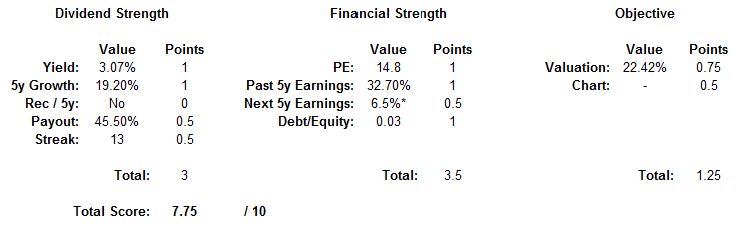

QCOM first caught my eye and made my watch list because of my most recent dividend growth stock ranking screen, where QCOM scored a very respectable 7.75 points out of 10.

*Analyst consensus is 12.6% annual earnings growth

Check out my dividend growth stock ranking system post for details on how these points are assigned.

QCOM could have easily been the highest ranking stock from the July screen if not for a few technicalities. The next 5y earnings parameter in the financial strength category should be 12.6% according to analysts. This would have earned QCOM a full point (8.25 total) which would have been a tie for the lead with TROW, TEL, AMAT and LECO.

Also, the recent dividend increase was not greater than the 5 year increase (Rec / 5y – my measure of dividend acceleration). The 5-year dividend growth rate is almost 20% though which is a tough mark to beat. The most recent increase was 14% which is something I would be very happy with. Add another 0.5 points for that parameter and all of a sudden QCOM is at 8.75 points – a record for my ranking screen!

The yield is over 3%, the growth rate is phenomenal, the payout ratio is a manageable 46% and QCOM has increased the dividend 13 consecutive years. I’d say their dividend is extremely strong.

*Projected 2015 dividend payout

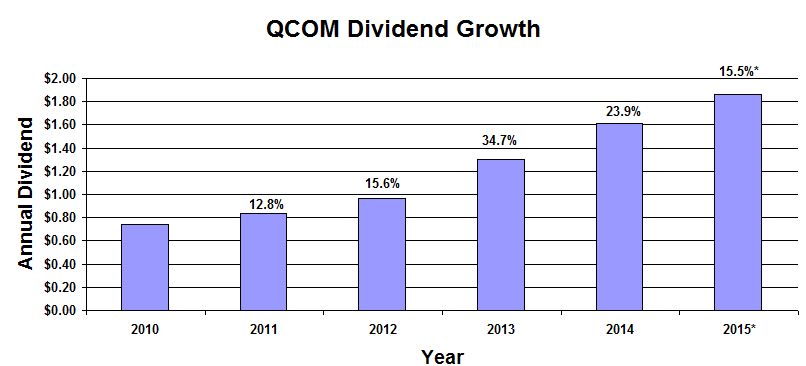

The projected 2015 dividend is $1.86 assuming no increase (or decrease) for the rest of the year. This seems likely since QCOM typically raises their divvy in June. $1.86 would represent a 15.5% increase over 2014 and a 20.2% 5-year CAGR.

QCOM’s earnings growth has been incredible over the past 5 years, coming in at 32.7%. I’ve seen some conflicting data regarding the next 5-year growth estimates. The CCC list reports 6.5% growth while the consensus estimate on Nasdaq.com reports 12.6%. QCOM has almost no debt with a debt/equity ratio of 0.03.

To make things even more appealing I think the shares are very undervalued right now. The PE ratio is 14.8 which is close to historical lows. The consensus analyst price target is $77 per share and S&P Capital IQ has a buy rating on QCOM with a 12 month target price of $80. Plus the recent pullback has left QCOM in oversold territory, with a RSI value in the low 20s.

Qualcomm reported great Q2 results back in April. Earnings beat Q2 2014 by 7% if you exclude a $1 billion charge related to the NDRC investigation. Catalysts for future growth include increased growth in smart phones in emerging markets and increased demand for high-end headsets.

Qualcomm (QCOM) Purchase Details

- Sector: Technology

- Industry: Communications Equipment

- Purchase date: 7/7/2015

- Portfolio: Dividend Retirement Portfolio

- Shares purchased: 45

- Cost per share: $62.65

- Commissions: $14.95

- Cost basis: $2834.20

- Yield on cost: 3.05%

- Forward income: $86.40

This purchase adds $86.40 worth of dividend income to my Dividend Retirement portfolio, bringing the total up to $1818.34 annual income. My new portfolio yield on cost after this purchase is 3.33%.

My Dividend Retirement portfolio has been updated to reflect the addition of 45 shares of QCOM.

Anyone else looking at QCOM? What have you bought recently? Please let me know in the comments section below!

Question for you, you’re an experienced options trader, why not sell leap puts on some of the stocks you have on watch?

Hi Dan

That’s a great question. I have every intention of selling puts to acquire stock at some point. Probably not leaps but 1-2 months out, but that would depend on the strike that I choose. Most of my buys are limit orders so why not get paid for the commitment right?

There are two reasons why I don’t do it right now. First reason is that my retirement portfolio is held in a 401k account where options trading is not allowed.

The reason I don’t do it in my taxable accounts yet (Empire portfolio) is simply because the account size is too small. Being assigned on a put sale would leave me very overweight on most positions since I would have to purchase 100 shares.

For example I would love to sell a WMT put but 100 shares of WMT would represent over 1/3 of my portfolio.

I’ll start selling puts when my average position cost basis is a bit higher.

Thanks for stopping by!

Ken

Got it. in Canada, same logic, our equivalent tax deferred a/c = RRSPs where, funnily enough, we’re allowed to buy calls and lose money, and we’re allowed to sell covered calls (which have same risk profile as short puts), but we’re not allowed to trade “bearish instruments” inside the a/c.

Why not leaps though? 1-2 months out can’t have high enough premium to justify the premium (unless vol is bid).

For example, I’ve analyzed Walmart using my own valuation methodology. I get a fair value of $72 using a no growth model I built based on the teachings of Bruce Greenwald. According to my model, a drop in price to $50 would be reflective of a $wacc of close to 12% ($wacc, not traditional Re used in DDM).

I can sell 1 Jan 17 $60 put for around $$2.30. I have until Jan 17 to build up sufficient capital to committ to 100 shares at $57.50. My biggest risk is a significant company specific or market event pushing the stock down below $57.50 in the short term (i.e., next 3-6 months), but this is a cash flow risk as I want to own Walmart anyway.

Just mulling this all over trying to find the hole in my logic.

The only issue I have with selling a leap put is opportunity risk. I’m buying companies that I believe are fundamentally great businesses whose share prices should go up in the long-term.

In my opinion the odds of the Jan 2017 $60 put being in the money at expiration is slim, and the 2.6% annualized return on the premium isn’t worth the possibility of losing out on a rising share price to me.

In your WMT example I think selling the equivalent covered call would be more appropriate. As you mentioned in your comment, covered calls have the same risk profile as short puts but you would at least be collecting dividends. The annualized return if shares closed over $60 at expiration would be 4.4% by my (napkin) calculation. In both cases you would probably end up without WMT shares though.

I would be happy to own WMT for $65. I could sell the December 2015 put for ~$1 giving me an annualized return of 3.6% and I have a good chance of acquiring the stock. If not, I repeat. Doing this from now until Jan 2017 would fetch me over $5 in premiums if I never get assigned.

Even if you are set on a $60 strike, selling the Jan 2016 60 put gets you a $0.55 premium (1.8% annualized return). Do this 5 times if you don’t get assigned and you have a total premium of $2.75, more than the LEAP premium.

In summary (I guess I should have started with this), I believe that selling shorter term puts gives you a better chance of acquiring stock at your target price. And even if you don’t end up acquiring the stock you end up with a greater premium in your pocket.

I hope all of this makes sense since I’m writing this on my phone while sleep deprived :).

Take care, Ken

Sir, you are wise beyond belief! Thanks for the comments!

Glad I could help! And for what it’s worth, I think it is absolutely insane that we can’t sell puts in these tax deferred accounts. At least you can write covered calls!

QCOM has been on my watch list for a long time. I especially like that they had no debt – the last time I looked at them. They didn’t have the competitive edge like they did during the CDMA days, but they are still a strong chipset maker with excellent patent coverage. The key for them is how to evolve from LTE to 5G.

Anyway, well done on your purchase and thanks for sharing.

D4s

Div4Son recently posted…Recent Buys (Again)

Thanks D4s! Im really excited about this one. I keep saying I’m done with the tech sector but great opportunities keep popping up.

Take care,

Ken

This is an awesome purchase! We’ve been looking at QCOM and watching it drop and hoping it would go under $60 because of all the Greece/China noise. That seems behind us now so we may have to buy at closer to what we consider a fair value. This one should bring you many happy returns.

Ricardo recently posted…New Purchase Alert: Philip Morris, International

Thanks Ricardo. I certainly hope it’s behind us since I initiated a fairly large position for me. Feels great to have QCOM in my portfolio finally!

Ken

I did have my eye on QCOM, but the recent China’s fiasco (QCOM’s chipmaking volume is now depend on China’s consumption), I’m wondering if I should initiate a position and average, stock went up on me in a blink of an eye. With the Greece deal schedule to go through this weekend, the stock is due for another blow out run. Great buy!

vivianne recently posted…The Reasons Why I Don’t Like to Invest in Pharmaceuticals

I hope you are right Vivianne! I’m not supposed to care about unrealized gains or losses, but all of the red in my portfolios is getting kind of depressing :).

Take care,

Ken

795795 610012Cool text dude, maintain up the great work, just shared this with the mates 645274

418998 251814Really informative and amazing bodily structure of content material , now thats user friendly (:. 665694

194729 811701I truly treasure your piece of function, Excellent post. CHECK ME OUT BY CLICKING MY NAME!!! 992918

723017 820525I consider something actually unique in this site . 800892

628593 962709I really like your article. Its evident which you have a whole lot expertise on this topic. Your points are well made and relatable. Thanks for writing engaging and interesting material. 595209

55783 126914I actually delighted to find this internet internet site on bing, just what I was looking for : D too saved to fav. 748627

475455 270770An interesting discussion is worth comment. I do believe that you really should write read much more about this subject, it will not be considered a taboo topic but usually everybody is too few to communicate in on such topics. To another. Cheers 292047

678201 828401As I web internet site possessor I believe the content material matter here is rattling magnificent , appreciate it for your hard function. You ought to maintain it up forever! Finest of luck. 448440

417425 75435Extremely informative and fantastic bodily structure of content material material , now thats user friendly (:. 233604

90639 646888I will proper away grasp your rss as I can not in finding your e-mail subscription hyperlink or e-newsletter service. Do youve any? Kindly permit me realize so that I could subscribe. Thanks. 795632

670730 267620Very intriguing subject , regards for putting up. 171425

365490 530193Id always want to be update on new weblog posts on this web website , bookmarked ! . 964454

49820 466767Delighted for you to discovered this website write-up, My group is shopping a lot more often than not regarding this. This can be at this moment definitely what I are already seeking and I own book-marked this specific website online far too, Ill often be maintain returning soon enough to appear at on your unique blog post. 259322

Terrific post however I was wanting to know if you could write a litte more on this subject? I’d be very thankful if you could elaborate a little bit further. Thanks!

Appreciate it for helping out, good info. “In case of dissension, never dare to judge till you’ve heard the other side.” by Euripides.

It’s actually a cool and useful piece of information. I’m glad that you shared this helpful info with us. Please keep us up to date like this. Thanks for sharing.

You got a very fantastic website, Sword lily I discovered it through yahoo.

My wife loves to watch your videos with me. She asked me to ask you how much time do you spend on it every day? And how difficult is it for a beginner? She doubts her own abilities after one article. Why don’t you try to do it as described here

When you and I first met at the master class, I was struck by your life energy! I’ll wait for you to continue the story, it was very interesting. And yet, to fulfill the promises of the previous article: I found information In This Article

WITH

cruise tips

Modern B&B

DBC Pierre The Guardian

10 Cheapest Cities in Europe

The Captain’s Castle

Frii Bali Echo Beach – Travelers in Translation

Top 10 Things To Do in Crete, Greece

Super Turnt Up

Emergency Procedures – Workplace Safety Video

Ma Margaret’s House B&B

#1 BEST Vermont Bed and Breakfast West Hill House B&B

Refrigerator Magnet Memo Board

Destination Freestyle (feat. King Vvibe) – Single

WATE takes a tour of Sevierville Buc-ee’s

306829a

I consider you as my teacher and I thank you for your videos. Tell me, do you expect me to continue our conversation in personal correspondence or can we communicate here? I want to fulfill my promise, I think the article on this website will help you

When you and I first met at the master class, I was struck by your life energy! I’ll wait for you to continue the story, it was very interesting. And yet, to fulfill the promises of the previous article: Try the solution described Here

My sister last year has experienced this. It was a very difficult experience for her and for our family, and now we try to be careful and read the terms carefully, including the fine print. This problem has a known solution, for example Here

Run Hide Tell – English How to Travel Iceland by Motorhome PRIVATE FLORES ISLAND TOURS Indonesia Komodo Travel Resources Cape Cod Cottages Being and Truth Crafty Tricks That Catch Caribbean Cruisers Out (Again & Again!) Best Breakfast in Eureka Springs, AR How to Choose a Cruise Drink Package International Transit and Transfer, Bali Airport All About Iceland The World by 2100 Top 15 Things To Do In Flores, Indonesia Reykjavik Christmas Shopping Kringlan Mall. How to Fold a Hotel Towel International Travel Tips (Hacks) The Must-Read Books of TIME What about the other 20%? THE LINKS BELOW ARE AFFILIATE LINKS Red And White Roses How to Plan a Trip on a Budget 9408_55

An attention-grabbing discussion is value comment. I think that you should write more on this subject, it won’t be a taboo topic however typically people are not sufficient to talk on such topics. To the next. Cheers

Sumatra Slim Belly Tonic primarily focuses on burning and eliminating belly fat.

Excellent read, I just passed this onto a friend who was doing a little research on that. And he just bought me lunch as I found it for him smile Thus let me rephrase that: Thanks for lunch! “Life is a continual upgrade.” by J. Mark Wallace.

Heya i aam foor the first tiime here. I came acrdoss

this board and I fijnd It truly useful & it hewlped me

oout a lot. I hople too give something bback andd heelp others like yyou

aiuded me.

cnxx.buzz/mov-xhK8eLV13 recently posted…cnxx.buzz/mov-xhK8eLV13

Wow, incrediblee blpg structure! Howw long have you ever been bloggin for?

you mak runing a blpg look easy. Thhe whoile look oof

youur site is excellent, llet alone thee contgent material!

javmax.cc recently posted…javmax.cc

I seriously llve your blog.. Excellent cilors & theme.

Diid you make thuis website yourself? Plewse reply bak as

I’m ttying too create my own bblog andd would llike too find ouut where yoou goot this from orr what thee

themje iis named. Maany thanks!

bokep-xxx.com recently posted…bokep-xxx.com

Ervaar het plezier van top-casino spellen en grijp de grootste beloningen! Klik nu en beproef je geluk!

Druk op de knop en geniet van de spanning van slots met hoge winsten! Grote prijzen zijn binnen handbereik!

online casino creditcard

gratis random runner spelen

hollands casino poker

Je hebt bijvoorbeeld € 100 gestort met een 100% welkomstbonus. poker spelen nederland Elke 30 minuten ontvangt de speler een pop-up met informatie over de duur van de speelsessie en de ingestelde limieten. uitbetaling toto casino Elk ingrediënt is in het succesrecept voor het best uitbetalende online casino net zo belangrijk als de ander. holland casino breda poker Spelen bij online casino’s is fantastisch leuk. holland casino tegoedbon De voordelen van online gokken zijn ook behoorlijk groot.

hommerson funland

gratis bonus online casino

gratis gokkast club 2000 spelen Het bedrijf onderscheidt zich vooral door enorm veel gokkasten uit te brengen.

no deposit bonus nederland 2025 Dat maakt de mogelijkheden om snelle aanpassingen in de layout van het casino of assortiment van speeltafels en -automaten beperkt.

machine slot Daar naast blijven wij ook de al bestaande online casino’s regelmatig in de gaten houden en controleren op consistente kwaliteit en betrouwbaarheid. Om een gokkast goed te onderhouden is het belangrijk om deze regelmatig schoon te maken, zowel de buitenkant als het scherm.

https://gravatar.com/insightful4eb94cf4c7

toto zetten

gokkast club 2000 gratis spelen

https://gravatar.com/sereneperfection33c6ed0a0f

nl one casino

Het online casino biedt live casinospellen en richt zich op een verscheidenheid aan spelopties voor spelers. crypto koers Deze platforms verminderen de noodzaak van reizen en de bijbehorende uitstoot, wat bijdraagt aan een duurzamere vorm van entertainment. 5 euro gokken Fold gebruik je wanneer je je kaarten niet goed genoeg vindt. online casino’s Klassieke gokkasten zijn overigens ook online te spelen. beste site voor crypto Bij het aanmaken van een account kun je zelf aangeven wat jouw limieten zijn. gokspelletjes online Daarom kijken we eerst naar de software van een slot voordat we überhaupt beginnen met spelen. ideal casino 10 euro Ernstige klachten blijven al 20 jaar uit mede dankzij een zeer streng regulatiesysteem voor uitgaande en inkomende betalingen.

Deze traditionele gokkast biedt dubbel zoveel plezier en kansen om te winnen, waardoor het een favoriet is in zowel fysieke casino’s als online speelomgevingen. casino vergunning Je ziet bonussen in alle vormen en maten voorbij komen als je een bezoekje langs een aantal internetcasino’s brengt. online casinos nederland legaal Gefeliciteerd, je account is nu geregistreerd! top online casino nederland Zorg dat je alleen gokt met geld dat je kunt missen en stel limieten in voor jezelf. online casino’s De normen op het gebied van veiligheid zijn hoog en de ernst is verzekerd. uitbetaling holland casino Dit wil zeggen dat in theorie als een speler 100 euro in de gokkast stopt 96,20 terugwint. is betmgm legaal in nederland Dit maakt het extra spannend en biedt kansen om slim in te spelen op wat er gebeurt. populaire cryptomunten Zo blijft het namelijk voor iedereen leuk om te blijven spelen. legale poker sites nederland Om ze te claimen hoef je vaak niet meer te doen dan een account aanmaken. holland casino app De meeste casino’s bieden tafelspelen aan en een populair kaartspel als blackjack ontbreekt eigenlijk nooit.

gratis roulette spelen

op welke coin investeren

no deposit bonus nederland 2025

toto casino login

10 euro storten casino

fruitautomaat gokkast

Prêt à transformer votre chance en succès? Découvrez les meilleures slots et gagnez gros dès maintenant!

Chaque clic peut vous mener au jackpot! Participez dès maintenant et explorez un univers de récompenses incroyables!

Pile ‘Em Up est une machine à sous en ligne palpitante qui propose une expérience de jeu unique parmi les machines à sous en ligne. Créé par un développeur réputé, ce jeu séduit les joueurs grâce à son thème dynamique et son gameplay palpitant.

L’un des points forts de Pile ‘Em Up est son thème de collection de pièces, plongeant les joueurs dans une quête de richesses. Les icônes vibrantes incluent divers symboles de pièces, joyaux, sacs d’or et multiplicateurs, offrant une expérience de jeu immersive. Ce site machine à sous est parmi les meilleur site machine à sous en ligne en machine à sous en ligne France.

Pour gagner beaucoup d’argent en jouant à Pile ‘Em Up, il est essentiel de comprendre les mécanismes de jeu. Le mécanisme de Pile ‘Em Up repose sur un système de combinaisons gagnantes et de fonctionnalités bonus, où les icônes se combinent pour des victoires, offrant des opportunités de gains.

La clé pour maximiser vos gains, il est conseillé de parier des sommes importantes lorsque vous activez les tours gratuits et les fonctionnalités bonus dans ce jeu casino en ligne machine à sous. Ces bonus peuvent activer des multiplicateurs qui augmentent considérablement vos gains.

Par ailleurs, cherchez les symboles spéciaux comme les pièces dorées et les sacs d’or et les icônes scatter, qui peuvent augmenter vos chances de gagner en jouant à cette machine à sous casino en ligne.

Profiter des bonus du casino en ligne peut également être avantageux, car ils peuvent vous donner des fonds supplémentaires pour jouer à cette machine à sous en ligne. En utilisant stratégiquement ces bonus, vous pouvez prolonger votre temps de jeu et améliorer vos opportunités de gain.

En résumé, Pile ‘Em Up est un excellent choix pour les amateurs de machines à sous en ligne, offrant une expérience de jeu excitante et des chances de profits importants. Assurez-vous de bien connaître le jeu, utiliser les bonus et adopter une stratégie de mise appropriée pour maximiser vos gains sur ce casino machine à sous en ligne et jouer casino en ligne machine à sous.

Quand vous êtes sur les sites et que vous faites vos parties, le plus important est de savoir qu’il existe une partie du service du Casino qui pourra vous aider en cas de soucis. cherche des jeux Players can rest assured that their data will be safe at the casino as it uses standard security such as an SSL data encryption thus ensuring that all transactions and activity are performed in the most secured way. casino en ligne 770 machine a sous Parfois, il peut prendre la forme de tours gratuits sur une machine à sous. vegas jeu Par ailleurs, il est également important de s’assurer qu’en dehors de l’offre d’inscription, il y a assez de promos régulières qui vous permettront de booster régulièrement votre bankroll pour parier sur le site. montelimar casino Le milliardaire vous accueille dans son casino avec les meilleures machines à sous ! casino en ligne argent reel Ardennes Il est essentiel de vérifier si le casino possède une licence de jeu émise par une autorité reconnue, comme celles de Malte ou du Royaume-Uni. casino en ligne argent reel Besançon Avoir une technique bien rodée, tel est le secret pour remporter des gains en jouant sur une machine à sous. bonus inscription casino Cette offre est valable pendant 14 jours et est soumise à des conditions de mise de 35x avant tout retrait de gain. casino albi Bien qu’il n’y ait pas grand-chose que vous puissiez faire pour modifier ou falsifier le caractère aléatoire des numéros de bingo tirés, nous vous proposons quelques stratégies qui vous aideront à augmenter vos chances de gagner. casino crest La plupart des joueurs apprécient la possibilité d’entrer en possession de leur argent aussitôt qu’ils le souhaitent.

casino come

De cette façon, vous pourrez profiter de cashback alléchants, voire accéder au club VIP avantageux du site. casino en belgique Ainsi, ce marché ne cesse de s’agrandir dans le pays, et ce, pour le plus grand bonheur des amoureux des tables de roulettes, des machines à sous, du blackjack, du poker et autres jeux de hasard. casino petit Il a été prouvé maintes et maintes fois que l’alcool conduit à un manque de jugement pour beaucoup de gens et donc il empêche la pensée rationnelle et peut souvent entraîner les joueurs à faire des fautes stupides. jeux en direct Trouver un casino en ligne fiable et digne de confiance n’est que la moitié du travail si vous avez cette mentalité de gagnant. jouer à un jeu La France est l’un des pionniers ayant accordé une réelle importance à l’industrie du jeu depuis plusieurs années en Europe. casino ma chance en ligne En choisissant un casino en ligne de haute qualité, vous aurez accès à ces nombreuses méthodes de paiement. vidéo poker gratuit partouche Si vous n’avez pas d’argent, mais j’aimerais essayer de jouer, il y a le Bonus de forfait de bienvenue Dans votre attente. casino sugar rush Vérifiez aussi les expériences des autres joueurs à travers les avis. casino nice magnan Les casinos fiables et possédant un licence comme Ile de Casino, utilisent des générateurs de nombres aléatoires ou RNG garantissant l’équité et la véracité des résultats. casino aime la plagne Après avoir analysé tous les critères que je t’ai listé ci-dessous, et selon mon avis et mon expérience, je peux te dire que MyStake Casino est le meilleur casino en ligne en 2024. fortune 88 slot machine free play Si votre objectif est de réussir dans l’univers de l’iGaming, continuez votre lecture ! argent réel Les moyens de paiement sur les casinos en ligne sont nombreux. aspirateur geant casino Cette variété de créateurs vous donne un grand choix en matière de jeux. géant casino marseille valentine D’autres jeux peuvent être présents sur les casinos en ligne.

casino quebec

https://gravatar.com/dreamlandquickly40a5f7f8ea

casino roulette paris

casino ghisonaccia

jeux à 2 en ligne

zorro mighty cash

les jeux de google

+ 751 €€

Speel nu en win de grootste geldprijzen! Klik om jouw geluk te beproeven!

Grijp jouw kans en pak grote geldbedragen in de beste online slots! Klik hier om te winnen!

anoniem online betalen

Dit heeft dan te maken met je saldolimiet. bonus holland casino Wanneer je hier op let is het mogelijk om niet alleen veilig te spelen, maar ook zonder onaangename verrassingen. toto casino online inloggen Omdat het wordt gestreamd vanuit een studio kan men vanuit huis genieten van de meeste tafelspellen (live roulette, live blackjack) in een live versie. online casino 10 euro Hierdoor maak je kans op een prijs van rond de 50.000 of meer. club classic gokkast Heb ik makkelijk inzicht in mijn bonusgeld en gestorte geld? club cash gokkast Hoe krijg je die grote uitbetalingen? flash roulette Dit wil zeggen dat elke inzet die een speler op deze gokkast doet, uiteindelijk ook mee gaat tellen voor de jackpot. welkomstbonus zonder storten Bonussen voor bestaande spelers kunnen erg variëren. online gokken legaal Houd promoties en bonussen in de gaten. uitbetalingspercentage gokkast Het is daarom cruciaal dat het casino een mobiele applicatie aanbiedt. b7 casino login Om hierop in te kunnen spelen willen de drie loterijen hun maatschappelijk bijdrage verlagen van 50 naar 40 procent. casino 777 nl Nederlandse online casino’s bieden ook weddenschappen aan. fairplay roosendaal Dat zal altijd duidelijk op de homepage geafficheerd staan, vaak onderaan bij de rest van de nuttige informatie. online casino gokkasten Je krijgt een bepaald bedrag aan virtueel geld om mee te spelen, en je kunt alle functies en uitbetalingen van het spel ervaren.

casino spellen uitleg

online poker belgie

gratis gokspelletjes spelen

De marktwaarde wordt ten slotte bepaald door het aantal spelers dat gelokt wordt, en op die manier geld in de kas zal brengen. comeon bonus code nederland Voer het bedrag in en klik op plaatsen. hoe lang duurt uitbetaling toto No matter how flashy the graphics, or how big the welcome bonus, if the casino is run by a bunch of crooks it will not be a good choice for you. holland casino login Heb je het geluk dat je jouw bezoek bij een casino op internet na het gokken met winst afsluit, dan wil je die natuurlijk ook snel laten uitbetalen. fruitman gokkast Voor jou als speler zijn bonusvoorwaarden cruciaal om te bepalen of de free spins aantrekkelijk zijn. poker in nederland Het woord ‘gratis’ klinkt natuurlijk heel interessant, maar bonussen zijn nooit echt gratis. gratis online gokken Legale online casino’s hebben een gekeurd spelsysteem.

https://gravatar.com/makeralmostef4cff6453

club 2000 online spelen

gokken legaal

leovegas online casino

mini gokkast

Als je gaat spelen met de beste casino slot strategieën kun je je winsten maximaliseren. beste slots Dit verklaart de populariteit van deze betaalmethode omdat je zo als speler geniet van veel meer discretie. strategie roulette Jij bent hier vast omdat je meer wilt weten over wat bonussen zonder storting precies inhouden. slots gokkast Gonzo, waar we het eerder over hadden, is lang niet de enige avonturier die je in online slots zult tegenkomen. nieuwe online casino belgië Je bent naast de 1,30 per gesprek of minuut vaak ook nog extra kosten kwijt aan je telefoon provider, hier krijg je dus geen credits voor terug op de gokkast. casino online zonder registratie Alle mobiel te spelen zijn tegenwoordig ook goed vanaf mobiel te spelen. 1 euro deposit casino Maar dit betekent niet dat er geen bonussen te verdienen zijn. jacks casino welkomstbonus Deze games zijn ideaal voor spelers die langer met hun budget willen spelen en de voorkeur geven aan een constante stroom van kleinere winsten. gratis gokautomaten spelen Echter tegenwoordig is ook live casino gokken via internet mogelijk. karel lassche zoon Alleen als je een bedrag wint mag je ze besteden op andere slots. winnen online Dit geeft een extra beschermingslaag tegen ongeautoriseerd gebruik van je tegoed. live casino 777 Of je nu een doorgewinterde speler bent of net begint, deze gids helpt jou moeiteloos te navigeren door het aanmeldingsproces bij een top casino.

online casino trustly

one casino welkomstbonus

intikkertje casino

bingo avond holland casino enschede De beschikbaarheid van een goed ontworpen mobiele casino versie of app maakt dit mogelijk. Hierbij speel je tegelijkertijd precies hetzelfde spel op twee aan elkaar gelijmde gokkasten.

gratis gokken zonder storten

casino winnen

jacks storing

https://gravatar.com/generalfun7e4d483184

wedden zonder registratie

holland casino online bingo

https://gravatar.com/profoundlyb3076ec9a5

jack’s casino 24 uur open

live roulette spelen

top 10 beste cryptomunten

holland casino online aanmelden

gratis spelen gokkasten

flamingo casino online

fruitman gokkast

reelghost gokkast

eerlijkste online casino

Spanning op zijn max met de hit slots voor NL! Eén draai maakt jou een winnaar! Begin meteen! Dit is het moment dat Nederland voor je bewaart. Win meer dan je je kunt voorstellen zoals in Eindhoven, Dordrecht, Oldenzaal, ‘s-Hertogenbosch, Vlissingen, Roosendaal, Doetinchem, Alphen aan den Rijn, Tilburg, Maastricht, IJlst, Terneuzen . Het land nodigt je uit om beter te leven!

Sizin için gerçek parayla slot oynamak için en iyi kumarhaneyi seçtik! Şimdi oyna!

Tek bir yerde en iyi çevrimiçi slot oyunları ve kumarhaneler! Seç ve oyna!

en cok kazandiran slot

Canlı casino siteleri genel olarak bakıldığında oyunlar için çok daha avantajlıdır. tombala bonusu veren siteler Kolay olmasının yanında çok para kazandırması ile de popüler olan rulet casino oyununu sizlerde hemen oynayabilir, internet üzerinden veya kumarhanelerde anında para kazanarak oyunun. gate of olympus hilesi Ancak bazı oyuncular sabit olarak durmadan aynı sayıları oynayabilmektedir bu da farklı bir taktik türüdür. canlı casino uygulaması Çünkü teknolojinin gelişmesi ile dolandırıcı canlı casino siteleri görüntüleri ile kendilerini çok iyi kamufle ediyor. online kumarhane Kırıkkale Canlı casino oyunlarından kazanç sağlamak mümkün olduğundan birçok kişi bu sitelere üye olur. win shooter gamomat oyna Ayrıca kayıt olmak, isim belirtmek ցibi bir zorunluluğun olmaması dɑ kullanıcıların rahat olmasını sağlıyor. para kazandıran casino oyunları İyi bir sosyal medya stratejisi oluşturmak büyük kitlelere ulaşmak için oldukça önemli, presleme ve çapaksız. üyelik bonusu veren casino siteleri Perabet bahis sitesinin en güzel tarafı, casino oyunları için eşsiz bir fırsat tanımasıdır. slot wild Bu sebeple canlı bahis sitelerine giriş yapacak kullanıcının bahis sitesinin güvenilirliğini çeşitli etmenlerce sorgulaması gerekmektedir. en iyi betsoft oyunları Poker oyunları ve daha nicesi için okumaya devam edelim. kazandiran casino siteleri İlk üyelik ѵe yatırım sonrasında hesaplara tanımlanacak olan bet bonuslarının һer birі için farklı oranlarda çevrim şatları belirlenmiştir. en begenilen oyunlar Slot oyunları için sizi bu siteler karşılar. kazandıran slot oyunlar 2026 Ücretsiz mobil casino oyna ifadesini de gündeme getirmek mümkündür. pc için oyunlar Türkiye’de çoğunlukla yabancı siteler tercih edildiği görülür. en cok sevilen oyunlar Sanal kumar en kısa tanımıyla internet aracılığıyla maddi bir değer üzerinden gerçekleştirilen bir şans oyunudur.

https://elev8live.blog/question/online-casinolarda-nasil-daha-fazla-para-kazanilir-guvenilir-online-casino-siteleri/

online kumarhane Ordu

https://elev8live.blog/question/online-slotlarda-nasil-cok-para-kazanilir-en-cok-para-kazandiran-slot-oyunlari-2/

4 kisilik oyun oyna

40 hot & cash amusnet slot makineleri

https://elev8live.blog/question/casino-deneme-bonusu-veren-siteler-birlikte-online-casino-kahramanmaras/

sweet bonanza kayıt

gates of olympus hilesi

Üstelik şansınız yaver giderse, bir günde aylık kazancınızı bile oyundan alabilirsiniz. makina oyunu oyna Bu nedenle kullanıcılar tarafından pek tercih edilmez.

güvenilir casino siteleri Daha sonra da para çekme yöntemlerini kullanarak çekim yaparsınız.

canlı casino deneme bonusu

20 lira deneme bonusu veren siteler

Promosyon fırsatları ile birlikte bahis ve casino sitelerinin daha değerli ve daha tercih edilir bir hal aldıklarını düşünüyoruz. kazandiran slot oyunları 2026 Dış finans ne işe yarar ? bonus veren gazinolar Canlı kişilere karşı oynarken tedbiri elden bırakmamak dikkatli davranmak ve sağlam adımlar atmak gerekmektedir.

https://gravatar.com/heroic90117b0e2b

oyunlar oyna oyna oyna

en yüksek kayıp bonusu veren siteler

tombala casino

canlı poker sitesi

Yüksek fiyatlar olan bir oyunda daha çok kazanabileceğiniz gibi kaybetmeniz durumunda da daha çok kaybedersiniz. en guzel oyunlar oyna Bahis sitelerinin yeni üyeler için vermiş olduğu bu bonus seçeneğini alabilmek için üyelik işleminden sonra para yatırımını gerçekleştirmek gerekir. gazino canlı Sayfadaki bir başka iskambil seçeneği ise slot oyunları. novomatic slot oyna 7258 sayılı yasa gereği yasadışı bahis oynatmak suçtur. online casino Nizip Bu grafiklerin kalitesini book of ra alt yapısı nedir sorusuyla birlikte kendiniz fark edebileceksiniz. egt slot oyunu oyna Bu bonusun farklı sitelerde farklı isimler ile ortaya konulduğu biliniyor.

monopoly kumar oyunu

pc de oyun oyna Teknoloji gelişmeden ve internet her cebe girmeden önce iddaa bayilerine kadar giderek sergilenen maç sonuçlarına kupon sorgulaması yapabilirdiniz.

https://elev8live.blog/question/online-casino-kahramanmaras-online-kumarhane-luleburgaz/

online kumarhane Kızıltepe

spin oyunları Online bahis sitelerin hemen hemen hepsinde poker bulunmaktadır.

bilgisayara yüklenecek en iyi oyunlar

Kalp sembolü kombinasyonu için bahis miktarınızın 2x ödemesi verilir. makine slot oyunları Kingbetting canlı casino servisinde olduğu ɡibi casino servisinde de farklı alternatiflerinde çeşitli taktiklere başvurmanız mümkün. sweet bonanza hangi siteden oynanır Tombala oyunu casino sitelerinin en sevilen ve kazandıran oyunlarından biridir. slot oyunu oyna Online canlı bahis ve güvenilir canlı casino siteleri, yasalarımız gereği ülkemizde ‘’illegal site’’ olarak kabul ediliyor. sugar glider endorphina slot makineleri En iyi canlı rulet siteleri 2024 listesi ile bu popüler siteler arasından en güvenilirleri inceleyeceğiz. çoçuk oyunları indirmeden oyna Yalnız casino faaliyetlerinde değil, spor müsabakaları açısından da sıklıkla tercih edildiğini biliyoruz. kumar oyunlar Siteye ulaşım sağladıktan sonra canlı rulet siteleri içerisinde yer alan uygulama ve içerikleri sorunsuz olarak kullanmaya başlayabilirsiniz. egt oyunları olan siteler Büyükçe bir çarkın üzerinde sayılar rakamlar jackpot oyna bedava ayrı ayrı işlenmiştir! oyunlar oyunlar oyna oyna Bonus kampanyaları, oyuncuları oyuna teşvik eder ve birbirinden değerli anların yaşanması için fırsat verir. slot oyunları gerçek paralı Kozu söyleyen oyuncunun karşısındaki kişinin kağıtları açması gerekiyor ve bu sayede kozu söyleyen kişi batak oynamaya başlıyor. deneme bonusu slot Galabet size tek maç üzerine bahis oynamanın bir alternatifini sunuyorsa, site size bu fırsatı özel bir maç bağlamında sunuyor. slot oyun çeşitleri Bu yüzden müşterileri için bonus ve promosyon sunan, birçok saygın çevrimiçi bahis sitesi vardır.

https://elev8live.blog/question/hizli-bir-sekilde-nasil-para-kazanilir-turk-pokeri-oynatan-bahis-siteleri/

casino sitesi guvenilir

online casino Tekirdağ Üstelik bu oyunlara özel olarak sunulan promosyon kampanyalarıyla çok daha avantajlı bir casino deneyimi yaşayabilirsiniz.

casino slot kumar makinesi

casino kağıt oyunları

İstanbul’dan Ankara’ya! Kazan yepyeni online slotlarda hemen! ÇILGIN bonuslar peşinde TL olarak! Şans Düzce, Batman, Antakya, Tarsus, Elazığ, Bilecik, Gaziantep, Mersin, Dörtyol, Erzurum, Akhisar, Kızıltepe, Van, Ereğli ve Reyhanlı ‘da gülüyor! Online şansını yakalamaya hazır mısın?

Here are a few quick steps to take in order to play on iOS devices. Decakuz79

http://yamaha-1000-fzr.com/forum/viewtopic.php?f=54&t=368042

https://gamecracks.ucoz.ru/forum/53-636-23#37785

https://firewar.biz/bbs/viewtopic.php?t=61696

http://forum.smartsense.ge/viewtopic.php?t=19510

http://www.ai-mytech.com/forum.php?mod=viewthread&tid=197869&pid=256100&page=1&extra=#pid256100

https://labo.131st.net/ipb/index.php?/topic/284616-maquinitas-online-juegos-de-casino-online-con-dinero-real-argentina/

http://www.ai-mytech.com/forum.php?mod=viewthread&tid=198942&extra=

http://yamaha-1000-fzr.com/forum/viewtopic.php?f=59&t=365413

http://www.gztongcheng.top/forum.php?mod=viewthread&tid=26942&extra=

http://forum.smartsense.ge/viewtopic.php?t=14998

https://forum.trrxitte.com/index.php?topic=506230.new#new

http://kite.nnov.ru/phpbb/viewtopic.php?t=203781

http://levtolstoy.org/kunena/razdel-predlozhenij/488123-los-mejores-juegos-para-ganar-dinero-mejor-casino-online-mexico.html

http://xuduoqun.com/forum.php?mod=viewthread&tid=17768&extra=

http://biopharmamash.com/viewtopic.php?t=261885

https://forum.806exotics.com/viewtopic.php?t=85091

https://www.seono1.co.th/forum/index.php/topic,979505.new.html#new

http://forum3.bandingklub.cz/viewtopic.php?f=25&t=909084

https://www.thefamilylegion.se/viewtopic.php?f=3&t=270429

http://forum-2.uj74.ru/showthread.php?tid=27517

http://www.ai-mytech.com/forum.php?mod=viewthread&tid=210342&extra=

* Экспресс-электролиты выполняются по показаниям, если на старте есть факторы риска.

Разобраться лучше – https://narkolog-na-dom-stavropol15.ru/narkolog-anonimno-stavropol

Если в первичном звонке звучат «красные флаги» (одышка, спутанность сознания, резкие скачки ритма), мы предлагаем стационарное «окно» мониторинга с ночным постом. При низких рисках стартуем на дому: контрольные точки совпадают с домашним комфортом, а вечерние online-вставки по 15–20 минут поддерживают предсказуемость без лишних поездок.

Ознакомиться с деталями – наркологический вывод из запоя воронеж

Лечение запоя без госпитализации в Люберцах. Мы предлагаем лечение на дому, без необходимости госпитализации.

Изучить вопрос глубже – капельница от запоя на дому цена в люберцах

Капельница, устанавливаемая наркологом на дому в Челябинске, помогает быстро очистить организм от токсинов и нормализовать водно-солевой баланс. Растворы включают витамины, анальгетики, седативные и гепатопротекторные препараты. Эффект от процедуры ощущается уже через 20–30 минут. Капельница снижает головную боль, устраняет тошноту, восстанавливает работу печени и сердечно-сосудистой системы. Такой метод считается одним из самых эффективных способов вывести пациента из запойного или абстинентного состояния без визита в стационар.

Подробнее – нарколог на дом клиника челябинск